A couple of weeks ago I went on a bit of a rant about some terribly irresponsible reporting about how much the American Rescue Plan is spending on subsidizing private health insurance and how many people that money is expected to provide insurance premium assistance for.

The bottom line is that a whole lot of people got both the numerator and denominator wrong: Instead of being ~$53 billion to cover ~1.3 million people (which would be an insane $40,000 per person for just six months), it's actually more like ~$61 billion to help cover ~18.6 million people (roughly $3,300 per person per year on average).

When the $1.9 trillion American Rescue Plan (ARP) achieved final passage on March 10th, it did so almost exclusively along party lines. I say "almost" because there was a single Democratic House member who voted against it: Representative Jared Golden (ME-02).

I fully understand the tightrope that some swing district Dems have to walk. To his credit, Rep. Golden voted to impeach Donald Trump not once, but twice (though he only voted in favor of one of the 2 articles of impeachment against him the first time around). I certainly don't expect every single Democrat to vote the party line on every single bill.

In the end, the bill passed anyway, if only by a handful of votes; my guess is that he even received Speaker Pelosi's unofficial blessing to vote against it, as long as she knew for sure it would pass regardless.

NOTE: SEE SUMMARY TABLE IN UPDATE ALL THE WAY AT THE END.

I'm doing my best to stop myself from putting my head through a wall this weekend.

You may have seen this viral tweet making the rounds over the past day or so:

The Democrats just spent $52 billion to subsidize COBRA for 1.3 million people until September. That’s $40k per person for less than 6 months of health insurance. Most countries spend about $5-6k per person per year for universal healthcare.

This was posted at 12:22pm on Friday, March 12th, 2021. It's still live as of 11:00am on Sunday the 14th, has over 32,700 Likes and has been retweeted over 7,300 times as of this writing, but in case it's deleted by the time you read this, here's a screen shot:

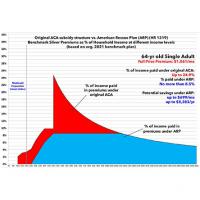

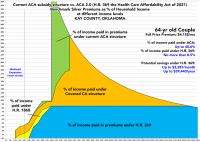

In early February, I posted a deep dive into HR 369, the Health Care Affordability Act, and how it would reduce net ACA premiums by permanently eliminating the income "subsidy eligibility cliff" (#KillTheCliff) and making the underlying subsidy formula more generous for all enrollees (#UpTheSubs).

I'm re-posting an updated, modified version of this analysis for two reasons:

First, because HR 1319, the American Rescue Plan, is about to actually pass and be signed into law, with a slightly different formula from HR 369 embedded within it (if only for two years).

Second, because my earlier analysis also threw in two other subsidy enhancement tables which confused the issue (California's state-based subsidies, and the predecessor to HR 369, both of which are/were less generous)

In this version I'm using the actual Advanced Premium Tax Credit (APTC) table under the American Rescue Plan, and I'm cutting out all references to the other two tables to avoid confusion.

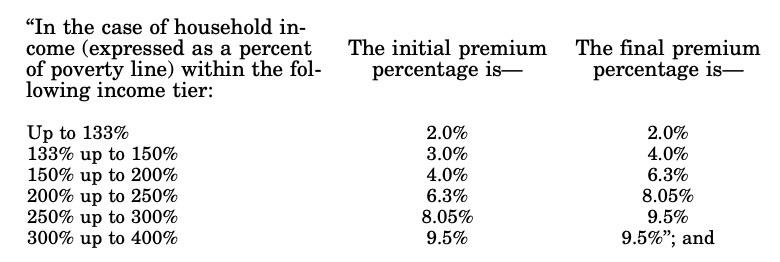

If you look at the actual legislative text of the final version of the Patient Protection & Affordable Care Act (PPACA, or simply ACA), the table describing the applicable maximum percentage of income that exchange-based enrollees have to pay for their premiums looks like the table below:

(Notably missing is the lower-bound 100% FPL subsidy eligibility cut-off; there's a separate section of the law which notes the 100% threshold but makes an exception for certain lawfully-present immigrants who earn less than 100% FPL but who aren't eligible for Medicaid for various reasons and are given an exception).

I'm a couple of weeks behind on this (the full #AmRescuePlan, #HR1319, already passed the House late last Friday night), but Medicaid expansion is one of the core issues I cover here, so it didn't feel right not to give this a write-up.

Before the Affordable Care Act was passed, only certain populations were eligible for Medicaid. Low-income children, pregnant women, parents of minor children and those with certain disabilities and so forth were eligible up to a certain household income threshold ranging from as a ceiling of as little as 13% of the Federal Poverty Line (parents in Alabama) to as much as 375% FPL (pregnant women and newborn infants in, interestingly, Iowa).

When President Biden announced that HealthCare.Gov would be re-launching an extended Special Enrollment Period in light of the ongoing COVID-19 pandemic, I wasn't surprised at all; in fact, I would have been shocked if he hadn't ordered the HHS Dept. to do so. I was surprised by how long the new COVID Enrollment Period would be: A full 3 months (I had been expecting either 30, 45 or perhaps 60 days at the outside).

Roughly two to three million people lost employer sponsored health insurance between March and September, and even families who have maintained coverage may struggle to pay premiums and afford care. Further, going into this crisis, 30 million people were without coverage, limiting their access to the health care system in the middle of a pandemic. To ensure access to health coverage, President-elect Biden is calling on Congress to subsidize continuation health coverage (COBRA) through the end of September. He is also asking Congress to expand and increase the value of the Premium Tax Credit to lower or eliminate health insurance premiums and ensure enrollees - including those who never had coverage through their jobs - will not pay more than 8.5 percent of their income for coverage.

Together, these policies would reduce premiums for more than ten million people and reduce the ranks of the uninsured by millions more.

Note: This is the second or third time that I'm cribbing a bit from my friend & colleague Andrew Sprung over at Xpostfactoid. If you like my healthcare policy analysis/writing style and follow me on Twitter, you should follow him at @xpostfactoid as well.

Over at Xpostfactoid, Andrew Sprung beat me to the punch by several days with an excellent two-part look at the "ACA 2.0 Hunger Games" scenario.

During the Democratic primary season, I posted a simple graph which boiled down the four major types of healthcare policy overhaul favored by the various Democratic Presidential candidates...which also largely cover the gamut of systems preferred by various Democratic members of the House and Senate.