Going forward, it looks like I'm going to have to do some educated guesses for a lot of carrier enrollment numbers for the states which haven't made their full 2023 rate filing data publicly available either on their own insurance dept. sites or even via the SERFF database.

The federal Rate Review site includes the average rate increases for each individual carrier, but most of the enrollment data is still redacted.

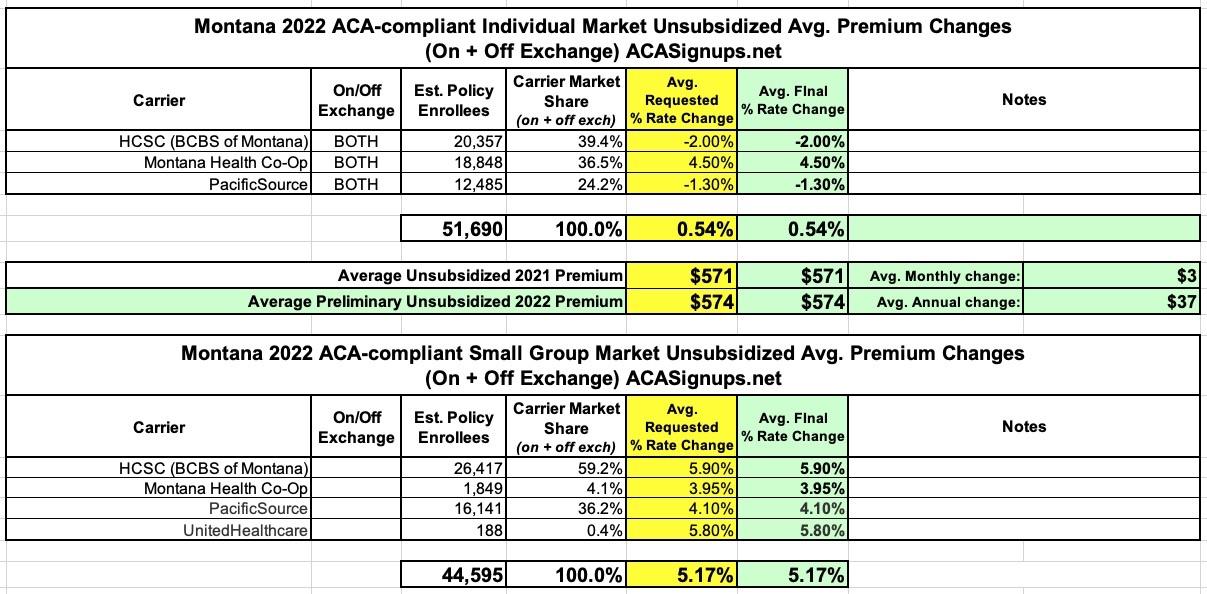

In Montana, there are only 3 carriers offering individual market coverage next year. I have hard enrollment numbers for one of them; for the other two, I'm assuming equal enrollment for each based on a rough assumption of ~52,000 total indy market enrollees statewide.

Assuming this is fairly close, that would put the weighted average rate increases at roughly 8.8%. If not...well, the unweighted average would be 9.3%.

For the small group market, I don't even have a decent total market size to base an estimate off of, so I have to go with the unweighted average of 4.9%.

Seriously, if every state displayed their annual rate filing data in as simple and clear-cut a fashion as Montana does, I'd be a much happier man. Admittedly, several others do, but the trickiest issue is usually getting the estimated enrollment numbers.

In any event, not much to say about Montana's ACA markets in 2022: No new carriers are jumping in, no current ones are dropping out, and the rate changes are pretty straightforward: +0.5% on the individual market, +5.2% on the small group market.

UPDATE 10/22/21: Well, it looks like the Montana Insurance Dept. has signed off on all 7 rate filing requests without making any changes, so I guess these are the approved rate changes as well:

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In some states I've been able to get more recent enrollment data from state websites and other sources.

ACA expansion in Montana didn't launch until 2016. It gradually ramped up over the next year or two and peaked at around 260,000 in 2018 before gradually dropping off to around 240,000 in early 2020...right before the COVID pandemic hit.

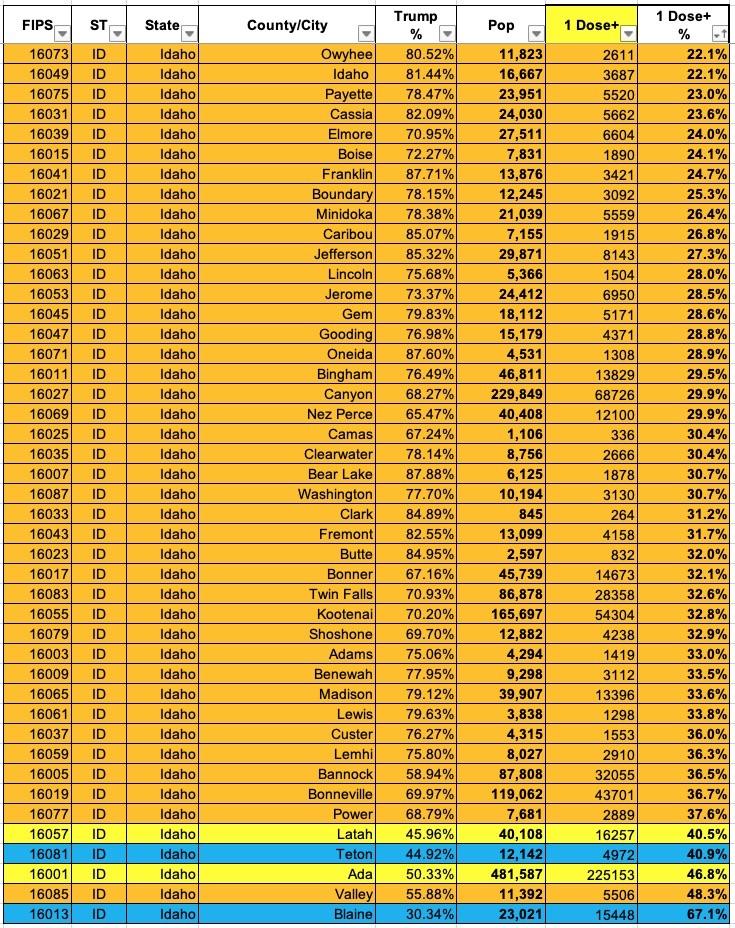

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

NOTE: This is an updated version of a post from a couple of months ago. Since then, there's been a MASSIVELY important development: The passage of the American Rescue Plan, which includes a dramatic upgrade in ACA subsidies for not only the millions of people already receiving them, but for millions more who didn't previously qualify for financial assistance.

Much has been written by myself and others (especially the Kaiser Family Foundation) about the fact that millions of uninsured Americans are eligible for ZERO PREMIUM Bronze ACA healthcare policies.

I say "Zero Premium" instead of "Free" because there's still deductibles and co-pays involved, although all ACA plans also include a long list of free preventative services from physicals and blood screenings to mammograms and immunizations with no deductible or co-pay involved.

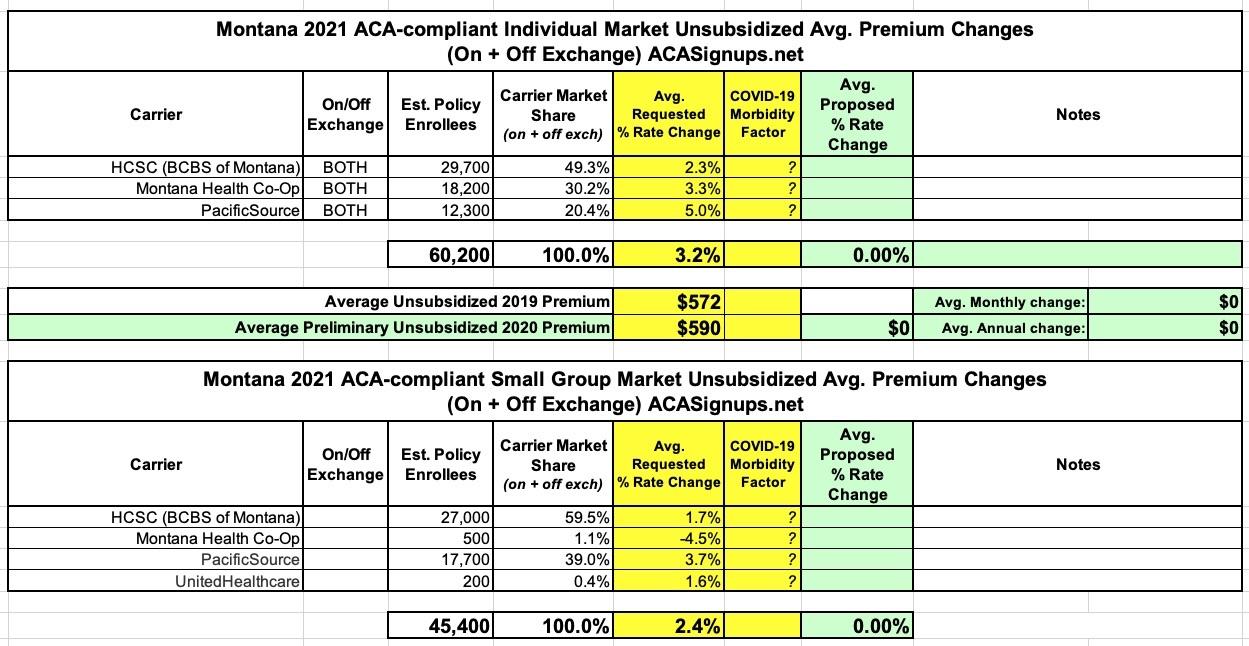

It was just a few weeks ago that the Montana Insurance Department posted the preliminary 2021 rate filings for the individual & small group markets. At the time, the individual market carriers were requesting a 3.2% average rate increase, while the small group carriers wanted a 2.4% bump.

Unfortunately, the actual actuarial filing memos ("Part II Justification") weren't available as of this writing, so I couldn't tell whether there's any COVID-19 impact specifically mentioned or not. Montana is one of the states with the fewest casese of COVID per capita, so I wasn't expecting much, but it would be nice to know.

Today I checked again and it looks like they've not only posted the Actuarial Memos (which don't mention COVID-19 at all, as I expected), but it also looks like Montana is the first state to publish their final/approved 2021 rate changes as well. They also modified the estimated enrollment numbers somewhat. Here's what it looks like now:

Last year, thanks to the Section 1332 Reinsurance waiver allowed for by the ACA, Montana health insurance carriers reduced their premiums for 2020 by 13.1% on average on the individual market, while raising them by 7% on the small group market (which the reinsurance program doesn't impact).

I've only written about Montana State Auditor (which includes acting as the Insurance Commissioner, as far as I can tell) Matt Rosendale a couple of times before. The first was in October/November 2017, when he pulled a cynical, disingenuous dick move by deliberately framing a non-profit insurance carrier into losing money for purely political reasons:

Montana commissioner chides insurance companies for raising rates, despite earlier offers to help

BOZEMAN — Montana's insurance commissioner chided two companies for raising rates on health insurance policies offered under the Affordable Care Act after federal subsidies ended, despite earlier telling them they could modify their rates if circumstances changed, the Bozeman Daily Chronicle reported.

...Matt Rosendale said he was "extremely disheartened" that PacificSource and the Co-op increased their premiums, adding that he had been assured by the companies that with or without the cost-sharing reduction payments they would be able to honor the rates they first submitted.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

REINSURANCE LOWERS HEALTH INSURANCE RATES FOR 2020

New Program Championed by Rosendale Leads to Double-Digit Rate Decreases in the Individual Market

HELENA, Mont. – State Auditor Matt Rosendale announced today that every health insurance plan sold on the individual market in Montana will have lower rates next year, largely due a new program that he’s championed for the past two years.

{kind=link}