Yesterday the Pennsylvania Insurance Dept. posted the preliminary 2021 rate filings for the individual and small group markets. On the surface, it appears that Pennsylvania has an absurdly competitive market, with 17 carriers listed on the indy market and 21 small group carriers...but when you look closer, many of these are simply branches of the same main company.

For instance, fully five of the individual market carriers are variants of "Highmark"...which is actually Pennsylvania's rebranding of Blue Cross Blue Shield. Two are branches of Geisinger and another two are both UPMC. The same is true in the small group market.

And don't even get me started about "Capital Advantage Assurance Company" and "Capital Advantage Insurance Company". Sheesh.

In any event, the overall rate filings average out to rougly a 2.6% premium decrease on the individual market and a 2.3% increase for small group plans, when weighted by carrier market share.

The Kentucky Insurance Dept. has posted KY's preliminary 2021 rate filings for the individual and small group markets, and the requested average rate increases for both are unusually high compared to the other states which have submitted their filings so far. In another unusual development, most of the carriers on each market are being pretty specific about the impact (or lack thereof) on their 2021 rate filings from the COVID-19 pandemic (I only have UnitedHealthcare posted once but they account for three of the seven small group carriers listed.

California’s Efforts to Build on the Affordable Care Act Lead to a Record-Low Rate Change for the Second Consecutive Year

The preliminary rate change for California’s individual market will be 0.6 percent in 2021, which marks a record low for the second consecutive year and follows California’s reforms to build on and strengthen the Affordable Care Act.

Covered California’s increased enrollment, driven by state policies and significant investments in marketing and outreach, has resulted in California having one of the healthiest individual market consumer pools and lower costs for consumers.

The impact of COVID-19 on health plans’ costs has been less than anticipated as many people deferred or avoided health care services in 2020, and while those costs are rebounding, it now appears the pandemic will have little effect on the total costs of care in California’s individual market for 2020 and 2021.

All 11 health insurance companies will return to the market for 2021, and two carriers will expand their coverage areas, giving virtually all Californians a choice of two carriers and 88 percent the ability to choose from three carriers or more.

Insurance companies offering individual and small group health insurance plans are required to file proposed rates with the Arkansas Insurance Department for review and approval before plans can be sold to consumers.

The Department reviews rates to ensure that the plans are priced appropriately. Under Arkansas Law (Ark. Code Ann. § 23-79-110), the Commissioner shall disapprove a rate filing if he/she finds that the rate is not actuarially sound, is excessive, is inadequate, or is unfairly discriminatory.

The Department relies on outside actuarial analysis by a member of the American Academy of Actuaries to help determine whether a rate filing is sound.

Below, you can review information on the proposed rate filings for Plan Year 2020 individual and small group products that comply with the reforms of the Affordable Care Act.

Users will only be able to view the public details of the filing, as certain portions are deemed confidential by law (Ark. Code Ann. § 23-61-103).

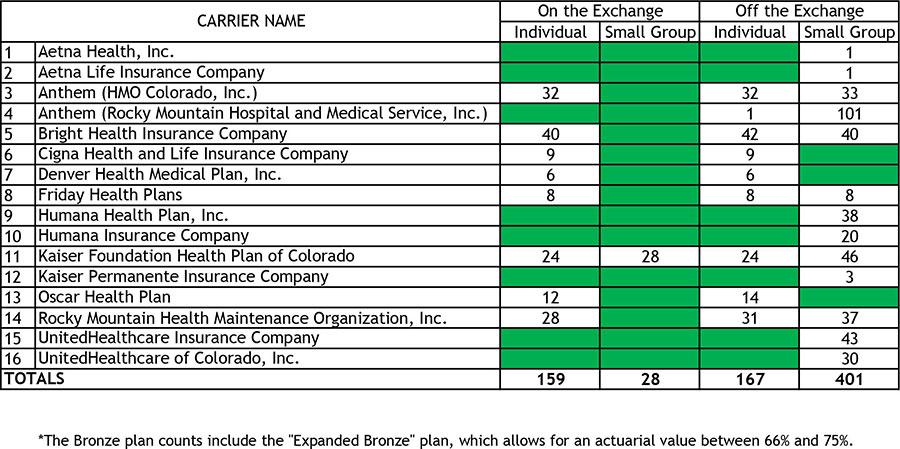

Overall, it looks like Colorado carriers are asking for a weighted average rate increase of 2.2% on the individual market and 5.7% on the small group market. There's some important tables breaking out exactly which carriers are offering their policies in which counties, and they've even broken out the average rate hikes by rating area, which is unusual to see but takes on special significance in Colorado due to thier unusual Section 1332 reinsurance waiver program, which is more robust in some parts of the state than others (I believe most reinsurance programs are pretty much an across-the-board sort of thing, though I could be wrong about that).

2021 Requested Commercial Health Insurance Rates Have Been Submitted to OHIC for Review

CRANSTON, R.I. (July 21st, 2020) – The Office of Health Insurance Commissioner (OHIC) today released the individual, small, and large group market premium rates requested by Rhode Island’s insurers. The requests were filed as part of OHIC’s 2020 rate review and approval process (for rates effective in 2021). Tables 1 – 3, below, summarize the insurers’ requests for 2021, and provide the requested and approved rate changes for the previous two years. Two insurers, Blue Cross Blue Shield of Rhode Island (BCBSRI) and Neighborhood Health Plan of Rhode Island (NHPRI) filed plans to be sold on the individual market for persons who do not receive insurance through their employer. In addition to BCBSRI and NHPRI, UnitedHealthcare and Tufts Health Plan filed small group market plans. Five insurers (BCBSRI, UnitedHealthcare, Tufts Health Plan, Aetna, and Cigna) filed large group rates.

ST. PAUL, Minn.—Searching for MNsure on the internet can yield misleading results. If you search for MNsure, you may see ads and websites that appear to be the official MNsure website but are not. Some of these sites collect your contact information and either bombard you with phone calls or try to sell you sub-standard health insurance. Here’s how to be sure you’re working with MNsure and purchasing comprehensive health care coverage:

Those eligible for the urgent need program must:

Check the website URL: make sure you’re clicking on MNsure.org when using a search engine or simply type MNsure.org into your address bar.

The Connecticut Insurance Department has posted the initial proposed health insurance rate filings for the 2021 individual and small group markets. There are 14 filings made by 10 health insurers for plans that currently cover about 214,600 people.

Important: As noted below, the 214,600 figure is Connecticut's individual & small group market combined.

Two carriers – Anthem and ConnectiCare Benefits Inc. (CBI) – have filed rates for both individual and small group plans that will be marketed through Access Health CT, the state-sponsored health insurance exchange.

The 2021 rate proposals for the individual and small group market are on average slightly lower than last year:

Unfortunately, it looks like only some of the 2021 ACA individual market premium rate filings have been uploaded to the SERFF database as of today, so I'm unable to calculate anything even close to an accurate weighted average. There are, however, several noteworthy items on the TX market:

Over a year ago, the Washington State legislature passed (and Gov. Inslee signed) a bill to create, for the first time, a state-based Public Option healthcare plan for the individual market. As I noted at the time, there's a few important caveats which illustrate again just how difficult it is to make major overhauls to the healthcare system, even at the state level: