The Department of Insurance receives preliminary health plan information for the following year from insurance carriers by June 1 and reviews the proposed plan documents and rates for compliance with Idaho and federal regulations. The Department of Insurance does not have the authority to set or establish insurance rates, but it does have the authority to deem rate increases submitted by insurance companies as reasonable or unreasonable. After the review and negotiation process, the carriers submit their final rate increase information. The public is invited to provide comments on the rate changes. Please send any comments to Idaho Department of Insurance.

Way back in May (a lifetime ago), Vermont was among the first states to publicly post their preliminary 2021 rate filings for their combined individual & small group market. At the time, the carriers were requesting an average 6.8% rate increase, and noted that they had no clue how much to tack on to cover themselves for the COVID-19 factor...or to even reduce rates because of it.

This week, the Vermont insurance regulatory board issued their final decisions about both BCBS of Vermont and MVP Health Plan, and cut down on each of their requested increases by several points (h/t Louise Norris for the links):

Hmmm...back in June, the New York Dept. of Financial Services published the preliminary 2021 rate filing requests for the individual & small group markets. As I noted at the time:

Hmmmm....some of these seem suspiciously high, at least as compared to the handful of other states which have released their preliminary requests so far, but we'll have to see...

It was just a few weeks ago that the Montana Insurance Department posted the preliminary 2021 rate filings for the individual & small group markets. At the time, the individual market carriers were requesting a 3.2% average rate increase, while the small group carriers wanted a 2.4% bump.

Unfortunately, the actual actuarial filing memos ("Part II Justification") weren't available as of this writing, so I couldn't tell whether there's any COVID-19 impact specifically mentioned or not. Montana is one of the states with the fewest casese of COVID per capita, so I wasn't expecting much, but it would be nice to know.

Today I checked again and it looks like they've not only posted the Actuarial Memos (which don't mention COVID-19 at all, as I expected), but it also looks like Montana is the first state to publish their final/approved 2021 rate changes as well. They also modified the estimated enrollment numbers somewhat. Here's what it looks like now:

The good news is that both of last years' individual market carriers (Blue Cross Blue Shield and Bright Healthcare) do have listings for 2021 in the SERFF database.

The bad news is that those listings don't include actual rate filings, just some other forms.

The good news is that rate filings for every state appear to be available at RateReview.HealthCare.Gov this week.

The bad news is that the filings at RR.HC.gov appear to be incomplete so far; BCBS is listed but Bright isn't (and since I do have other forms for Bright being listed in 2021, I'm pretty sure it's not because they're pulling out of the Alabama market).

The good news is they include the number of people enrolled by each carrier in both markets, making it easy to calculate a weighted average, and th ey even include the SERFF tracking number for each.

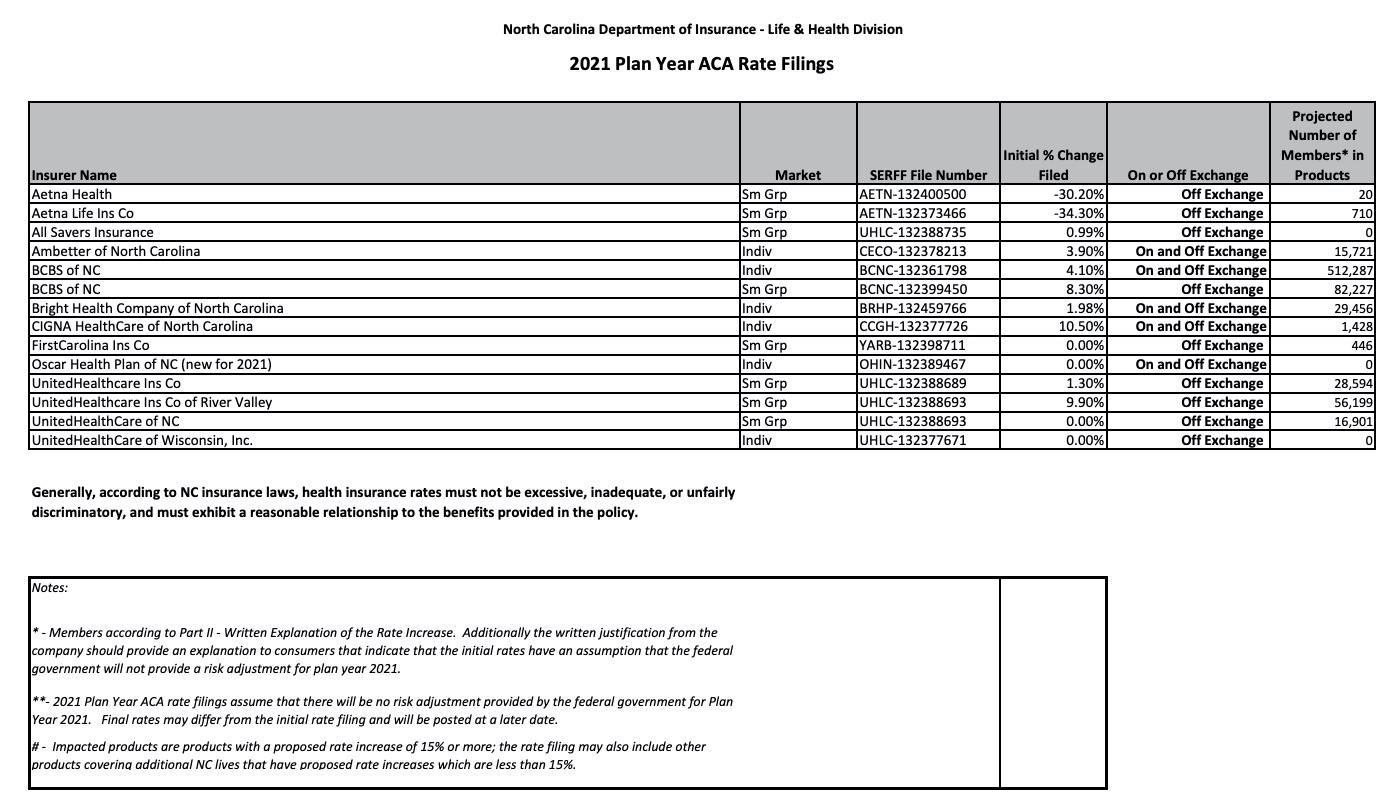

The bad news is they don't include links to the actuarial memos, and even plugging the tracking numbers into the SERFF database only brings up the memos for three of the six carriers on the individual market...and of those, two of the three have been redacted (Oscar and Cigna), while the third (UnitedHealthcare) is brand-new to the North Carolina market anyway and therefore has no COVID-19 impact on their rate changes to speak of.

Are you turning 26 soon and still on your parent’s health insurance policy? Did you know that you will need to take action or you may no longer have health insurance? Don’t worry, you have options!

If you have a job that offers insurance, you can enroll in that coverage as turning 26—known as aging out—is considered a qualifying life event and will enable you to enroll in job-based coverage outside of your job’s open enrollment period.

Get covered through your school

If you are a college student, you may be able to enroll in a student health insurance plan through your school. Find out more

As I noted last year, the Nevada Insurance Dept. website is both helpful and frustrating when it comes to tracking down the type of data that I need. On the one hand they make it very easy to view the individual & small group market rate filing summaries: Carrier names, markets, sumission dates, status, effective dates and most importantly, the proposed and approved average rate changes are all easily found.

On the other hand, they don't actually link to the filing memos or URRT forms, which means I can't find the actual effectuated enrollment numbers for each carrier, the impact of COVID-19 on each carrier's request or other noteworthy info about the filings. Oddly, they do include the SERFF tracking numbers...except that plugging those into the SERFF database still doesn't bring anything up, which kind of defeats the point.

Fortunately, the NV DOI does provide the weighted average of the entire market and COVID-19 impact elsewhere. I've also been able to piece together the total market enrollment (both on & off-exchange) using some other public data.

With recent reports illustrating the growing number of uninsured Americans across the country, MNsure is reminding Minnesotans that there are options. For those who have lost their health insurance, seen a change in income, or experienced a qualifying life event, enrollment opportunities may be available.

"The last couple of months has brought tremendous uncertainty to many families across the state," said MNsure CEO Nate Clark. "It's important that Minnesotans know there are enrollment opportunities available if they lose their health insurance. MNsure is here to help."

Since the start of the COVID-19 pandemic, more than 100,000 Minnesotans have come through MNsure to find health insurance coverage.

For new customers, you may be eligible to enroll if:

I've acquired the preliminary 2021 rate filings for Georgia's individual and small group market carriers. There were two filings submitted for many of the carriers because of a (since delayed) ACA Section 1332 waivier submission; the carriers submitted one in case the waiver was approved and a second if it wasn't. Since the process has been delayed, however, the no-waiver filing is the one which is relevant.

As you can see in the tables at the bottom of this entry, the overall weighted rate change requested by individual market carriers in Georgia is a 1.3% reduction, which would have been more like a 2.3% drop if not for the COVID-19 factor, according to the carriers. The small group market carriers are requesting an 11.1% average increase, which is unusually high these days. I haven't reviewed all the memos for the sm. group market to see what they're pinning on COVID-19, however.

Here's what the indy market carriers have to say about the COVID-19 factor in their 2021 filings: