My 2021 Rate Change project isn't complete yet for two reasons: First, I only have the final/approved 2021 rate filings for 18 states as of today (vs. preliminary rates for all 50 states + DC). Second, a higher-than-usual number of carriers have made it impossible (or at least highly difficult) to dig up their effectuated enrollment data for 2020.

Without that number, I have no way of running weighted averages for that state's individual market; those are listed in grey below. In a few cases (like Florida), the state insurance dept. actually provided the weighted average but I still had to guess at the total enrollment number (also in grey).

This is a bigger problem than you might think. Let's say a state has 3 carriers requesting a 5% rate reduction, a 2% increase and a 15% increase. The unweighted average would be +4%....but if it turns out that the first carrier holds 90% of the market share this year, the weighted average would be more like -4%. You see the problem here.

At long last, I've finally wrapped up my 50-state (+DC) 2021 Rate Change project...or at least the preliminary rate filings; I have the final/approved rate changes for 18 states as of this writing.

I'm finishing things off with New Jersey, and unlike the past half-dozen or so states, I am able to run a properly weighted average for both the individual and small group markets in the Garden State even though, like many other states, the actuarial memos are either unavailable or heavily redacted.

In any event, based on the Q2 2020 report (which includes enrollment data updated through the end of June), 2021 enrollees in New Jersey's individual market are looking at average premium increases of around 4.1%, while small group plans are going up by roughly 2.6% on average.

Massachusetts, which is arguably the original birthplace of the ACA depending on your point of view (the general "3-legged stool" structure originated here, but the ACA itself also has a lot of other provisions which are quite different), has ten different carriers participating in the individual market. MA (along with Vermont) has merged their Individual and Small Group risk pools for premium setting purposes, so I'm not bothering breaking out the small group market in this case.

Getting a weighted average is tricky. On the one hand, only one or two of the rate filings included actual enrollment data. On the other hand, the Massachusetts Health Connector puts out monthly enrollment reports which do break out the on-exchange numbers by carrier. This allowed me to run a rough breakout of on-exchange MA enrollment. I don't know whether the off-exchange portion has a similar ratio, but I have to assume it does for the moment.

Louisiana joins the disturbingly-long list of states where the 2021 individual & small group market rate filings are either completely missing or heavily redacted, thus making it impossible for me to break out the market share by carrier and thus running a weighted average rate change.

I really hope this trend is reversed in the future, whether via HHS transparency regulations or through legislation.

In any event, the unweighted average rate increase for the Louisiana indy market is around 6.9%, and for the small group market it's roughly 5.2%.

Once again, I'm afraid the actuarial memos for Kansas' 2021 individual and small group market carriers are either absent or redacted, so I have to run unweighted average rate changes, which are likely off significantly (for instance, the individual market is +7.8% unweighted, but if it turns out that, say, Oscar Insurance has 95% of the market share, the weighted average would be more like a 7% decrease).

Unfortuantely, without knowing the actual enrollment data for each carrier, this is the best I can do for now. The small group market's unweighted average increase is 8.2%.

(sigh) Once again, I only have actual enrollment data for a one of the five carriers offering individual market policies in Illinois next year, and for two of the eleven selling small group plans. That means I can't run a weighted average rate change for either market, just unweighted ones.

That being said, the unweighted average change on the individual market is a 1.8% premium reduction, while the small group market is increasing by 5.2%.

Unfortunately, Alaska's 2021 rate filings aren't available via the state insurance department website or the SERFF database, and the actuarial memos posted to the federal Rate Review database are heavily redacted, so I can't run a weighted average rate change for either the individual or small group market.

The unweighted average changes, however, are a 2.0% reduction on the indy market and a 1.9% reduction for small group plans.

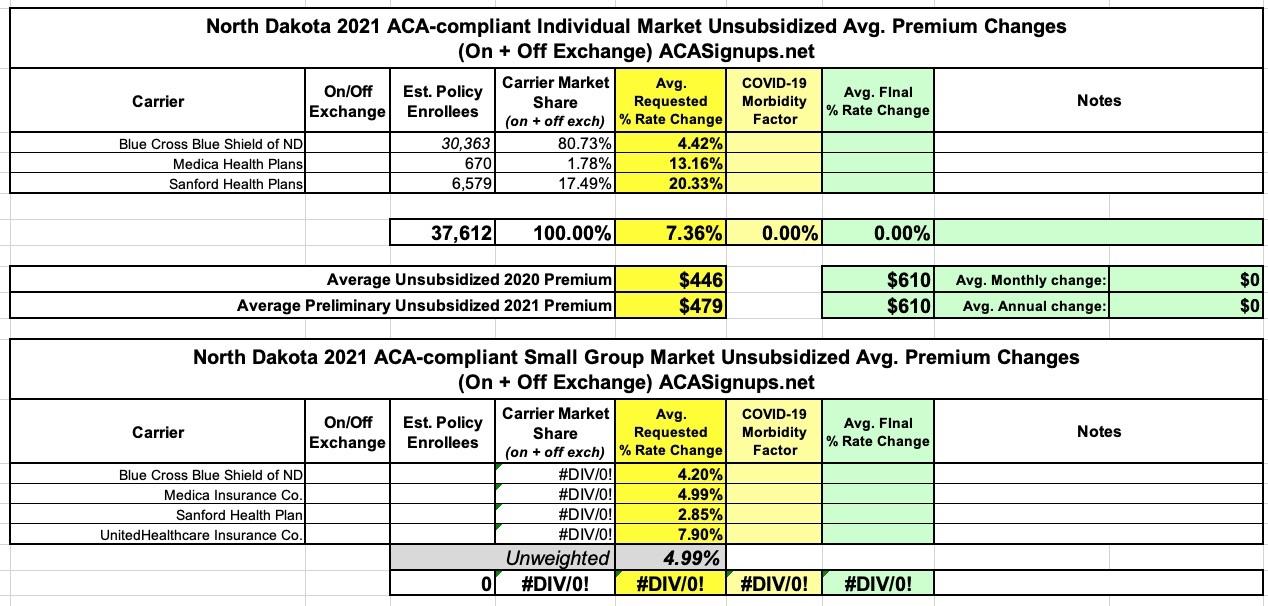

Here's North Dakota's 2021 individual & small group market rate change filings. Note that all of the small group filings are heavily redacted and the memos aren't available in the SERFF database for any of them, so I can't run a weighted average and had to go with the unweighted 5.0% increase.

For the individual market, Blue Cross Blue Shield's memo isn't available, so I had to plug in an estimate based on the average 2019 enrollment; I'm assuming it's fairly close to that this year as well. Weighted average on the indy market is a 7.4% increase.

The South Carolina Insurance Dept. released their final/approved 2021 Individual and Small Group Market premium rate changes.

I actually never got around to analyzing the preliminary rate filings for SC, so I don't actually know whether any of these are changes from the original filings, but whatever. In the end, the Palmetto State's individual market premiums will be dropping by about 1.5%, while their small group rates will be increasing by 4.7% on average.

It's also worth noting that UnitedHealthcare of SC is joining the South Carolina small group market for the first time next year (not to be confused with "UnitedHealthcare Insurance Co." and "UnitedHealthcare Insurance Co. of the River Valley...no confusion there I'm sure...)

South Dakota's 2021 individual & small group market rate filings are up, and there's not much to say about any of them: Individual premiums are going up around 2.6%, small group market policies around 2.8% overall statewide.