MY OFFICIAL 2019 RATE HIKE PROJECT EXPLAINER

Tue, 06/05/2018 - 1:56pm

The past two days have brought a flurry of 2019 premium rate change filings, with Washington, New York, Maine, DC and Pennsylvania putting their preliminary cards on the table. These join 5 other states which had already posted their early numbers, so I now have 10 compiled.

Now that I have a solid amount of state data to work with, I figured I should write up a tutorial to explain my methodology. This has become especially important the past two years since there's some new factors to consider.

OK: Calculating the average requested rate changes within each state is fairly easy (assuming I can dig up the necessary data). As I do every year, within each state's carrier filings I do the following:

- 1. Find the average, overall requested average rate increase for each carrier's 2019 ACA-compliant individual market policies

- 2. Find (or estimate if not available) the number of people currently enrolled in that carrier's ACA-compliant plans (both on & off-exchange)

- 3. Calculate the carrier's market share relative to the statewide ACA-compliant individual market

- 4. Multiply the carrier market share by their avg. requested rate change, to get the carrier's portion of the statewide average change, and then...

- 5. Add up all of those portions to get the overall, average rate increase.

For example, let's suppose a state has only 2 carriers in the individual market, with a combined enrollment of 100,000 people. One has 80,000 enrollees (80% market share), the other has 20,000 (20% share). Let's say the first carrier is raising premiums an average of 30%, while the second is raising them 15%.

That would give the following:

- Carrier A: 0.80 x 0.30 = 0.24

- Carrier B: 0.20 x 0.15 = 0.03

- Weighted Average increase: 0.27 = 27.0%

Simple, right? Up until last year, that's pretty much how I kept it. I'd run the numbers this way for every state during the requested change phase, then go back and re-run the numbers using the final, approved rate changes. Along the way, carriers would drop out, jump in, drop or add certain policies (some would discontinue PPOs but add more HMOs, etc), and so on, so the final, approved rates and averages often bore little resemblence to the original requested ones.

Of course, it's not always that simple. Sometimes the carriers don't list their current number of enrollees. Sometimes they only provide their projected enrollment number for next year. Sometimes they provide the total number of member months (in the example above, Carrier B might only say that they expect 240,000 member months in 2018, which I'd divide by 12 to get 20,000 enrollees). Sometimes they're dropping out of part of a state but not all of it. Sometimes they're dropping one line of policies but not others. In all of these cases I have to use my best efforts to get a reasonable guesstimate.

I didn't do this project in 2014 or 2015. In 2016 and 2017, I didn't really get into the reasons for the average rate increases, because I was still new at it and because they were pretty obvious:

- Some of it was lingering effects of various types of earlier sabotage (the Risk Corridor Massacre, for instance) which happened before started the project

- A smaller chunk was due to regular inflation, the ACA carrier tax, exchange usage fees

- A much larger chunk was due to the "Blue Leg" ACA regulations: Guaranteed Issue, Community Rating, Essential Health Benefits, no more Annual/Lifetime Caps and so on.

Last year, however, I had to up my game. The Trump Administration's decision to cut off Cost Sharing Reduction (CSR) reimbursement payments was a very specific and deliberate decision on Trump's part intended (by his own word) to cause the ACA exchanges to "blow up". So were other administrative decisions such as slashing the marketing budget for HealthCare.Gov by 90%, slashing the navigator/outreach budget by 40%, attempting to get the IRS not to enforce the ACA's Individual Mandate, cutting the Open Enrollment Period in half and so on.

In light of these deliberate attempts to undermine and sabotage the ACA, and given that the carriers in many states were already submitting two sets of 2018 rate filings anyway (one with CSR payments, one without), I decided to do my best to separate out what portion of the rate increases was due to the normal factors and what portion was due to deliberate, blatant, utterly unnecessary sabotage efforts by Trump and Congressional Republicans. As it happened, I ended up having a pretty good track record.

OK, so what about 2019? Well, again, calculating the actual requested rate changes is fairly easy. The tough part is figuring out how much of that rate change is due specifically to the new batch of sabotage efforts by Trump and the GOP. So far, there's three of them, joined at the hip:

- Repeal of the ACA Individual Mandate Penalty, combined with...

- Expansion of non-ACA compliant "Short-Term, Limited Duration" plans (i.e., making them neither short term nor of limited duration); and...

- Expansion of non-ACA compliant "Association Health Plans"

The good news is that just as they did last year with the CSR cut-off, many carriers this year are specifically stating not only that repeal of the mandate/expansion of #ShortAssPlans are causing a big chunk of their rate increases, but some of them are putting a hard number on how much is due to those factors.

In states where all (or at least a significant portion) of the carriers do so, I'm using their numbers to estimate the ACA Sabotage impact.

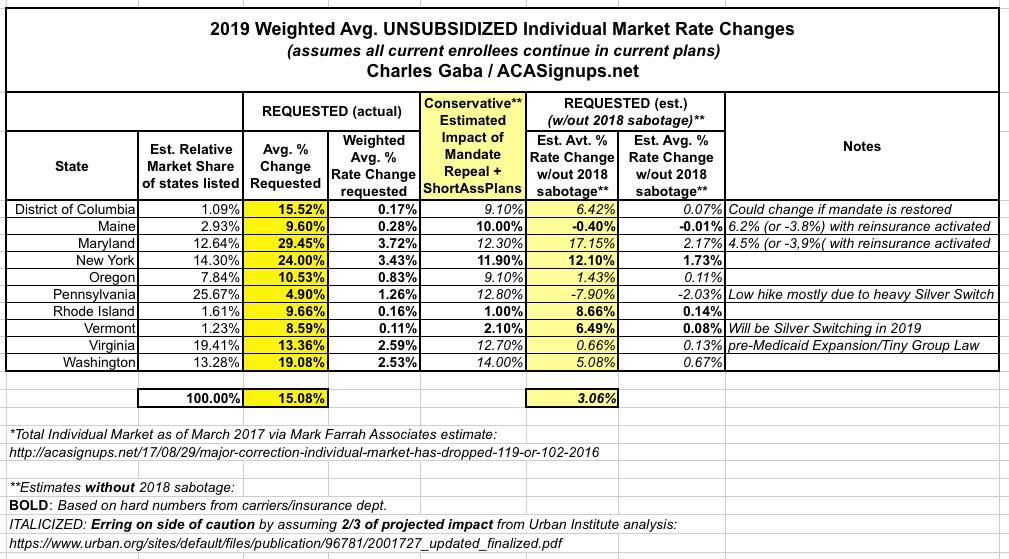

Even better, in some states, the state insurance department is doing this for me. For instance, New York made it very clear: 24.0% average increase, of which 11.9% is due specifically to the mandate being repealed (NY doesn't allow short-term plans at all).

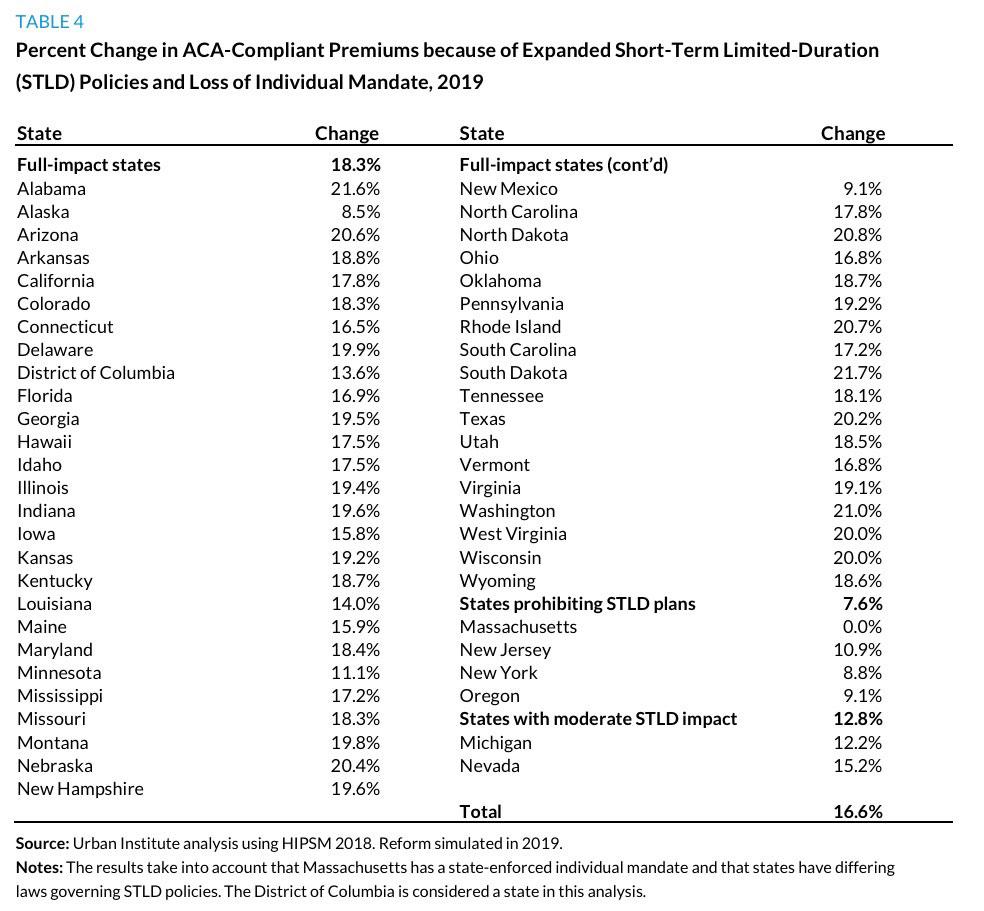

Unfortunately, in many states, neither the insurance department nor the carriers provide any hard guidance on this (in some cases one small carrier out of 5-6 might do so, not enough to extrapolate from). In those cases, I've turned to the most comprehensive analysis of the issue I know of: The Urban Institute's study on The Potential Impact of Short-Term Limited-Duration Policies on Insurance Coverage, Premiums, and Federal Spending from back in March. Here's their bottom line:

Obviously these are projections only; the actual average changes vary widely. For instance, in Rhode Island, Urban projected a whopping 20.7% sabotage factor...but the carriers themselves are only pinning about 1% on it. On the other hand, in New York, Urban projected just an 8.8% sabotage factor for mandate repeal + short-term plans combined...but it's actually somewhat higher: 11.9%.

With that in mind, for states where I don't have hard data from either the carriers or the state insurance department, I'm going to use the Urban Institute's estimates...but I'm going to knock 1/3 off their projections in the interest of erring on the side of caution.

For instance, in Pennsylvania, Urban projected a 19.2% sabotage increase. Since I don't have access to the actual rate filings and the PA Insurance Dept. didn't go into specifics about how much of their 2019 average rate change is due to mandate/shortassplans, I'm taking 2/3 of Urban's projection: 12.8%.

Pennsylvania carriers are asking for a 4.9% average rate increase next year, so I'm assuming that in the absence of both mandate repeal and #ShortAssPlans, they'd actually be asking for an average 7.9% rate decrease.

With all that in mind, here's what things look like as of today across the 10 states (well, 9 + DC) which have released their 2019 ACA Individual Market Rate Changes so far:

As of today, it looks like an average of around 15.1%, with around 12 points of that being due to mandate repeal / #ShortAssPlans, and the rest being actual, underlying cost increases and so forth. Obviously these numbers will jump around as more states release their data, and then they'll jump around again once the approved rate changes come in...not to mention other resubmission factors like Medicaid expansion in Maine and Virginia; reinsurance programs in Maine and Maryland, and so on.

Stay tuned...

Advertisement