Open Enrollment Period for Get Covered New Jersey Begins Nov. 1, With Record Levels of Financial Help Available to Make Health Insurance More Affordable

Majority of consumers receiving financial help can find a plan for $10 a month or less

More options available to consumers for 2022, Residents can preview available plans now at GetCovered.NJ.gov

TRENTON — The Murphy Administration announced today the Affordable Care Act Open Enrollment Period at Get Covered New Jersey (GetCovered.NJ.gov), will begin Monday, Nov. 1st, with more plan choices and record levels of financial help available to make health insurance more affordable. Residents can view available 2022 plans and compare costs now, before the enrollment window opens, using the Get Covered New Jersey Shop and Compare tool.

NJ Department of Banking and Insurance Announces More Health Insurance Offerings in 2022, Record Levels of Financial Help Available for Another Year at Get Covered New Jersey

9 in 10 enrolling on the marketplace qualify for financial help; majority of consumers receiving assistance can find a plan for $10 a month or less

TRENTON — The New Jersey Department of Banking and Insurance today announced that consumers shopping for 2022 health coverage this fall at Get Covered New Jersey, the state’s official health insurance marketplace, will continue to benefit from record levels of financial help available from the federal American Rescue Plan and the State of New Jersey. Consumers will also have more choice, with the entry into the market of a new health insurance company, Ambetter from WellCare of New Jersey, increasing the number of carriers offering plans on the marketplace.

NJ DOBI Announces Grant Opportunity for Navigators to Assist New Jerseyans With Health Insurance Enrollment

Open Enrollment Period at Get Covered New Jersey Begins November 1, 2021

TRENTON – The New Jersey Department of Banking and Insurance today announced it is now accepting applications for community organizations to serve as Navigators to assist residents with health insurance enrollment for the upcoming Open Enrollment Period and during 2022. The department is making available a total of $4 million in grant funding for Navigators, in an effort to ensure enrollment assistance is available in the community for residents seeking coverage through Get Covered New Jersey, the state’s official health insurance marketplace, during the Open Enrollment Period that starts November 1, 2021 and through the year.

TRENTON – New Jersey Department of Banking and Insurance Commissioner Marlene Caride issued the following statement on the U.S. Supreme Court decision today upholding the Affordable Care Act by a 7-2 vote:

“Today’s Supreme Court decision is a victory for millions of Americans and New Jerseyans who have access to quality, affordable health insurance as a result of the Affordable Care Act.

“Under Governor Murphy’s leadership, New Jersey has led the way in increasing access to health insurance based on the guiding principle that health care is a fundamental right. New Jersey launched its own state-based health insurance exchange, Get Covered New Jersey, and provided state-level subsidies to increase access and affordability of health coverage and care for our residents, and enrollment increased by nearly 10 percent during our first Open Enrollment Period. Nearly 40,000 residents have signed up for health insurance during the Special Enrollment Period opened by the state on February 1 in response to COVID-19.

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In some states I've been able to get more recent enrollment data from state websites and other sources.

Today I'm presenting New Jersey.

For enrollment data from January 2021 on, I'm relying on adjusted estimates based on raw data from the New Jersey Dept. of Human Services.

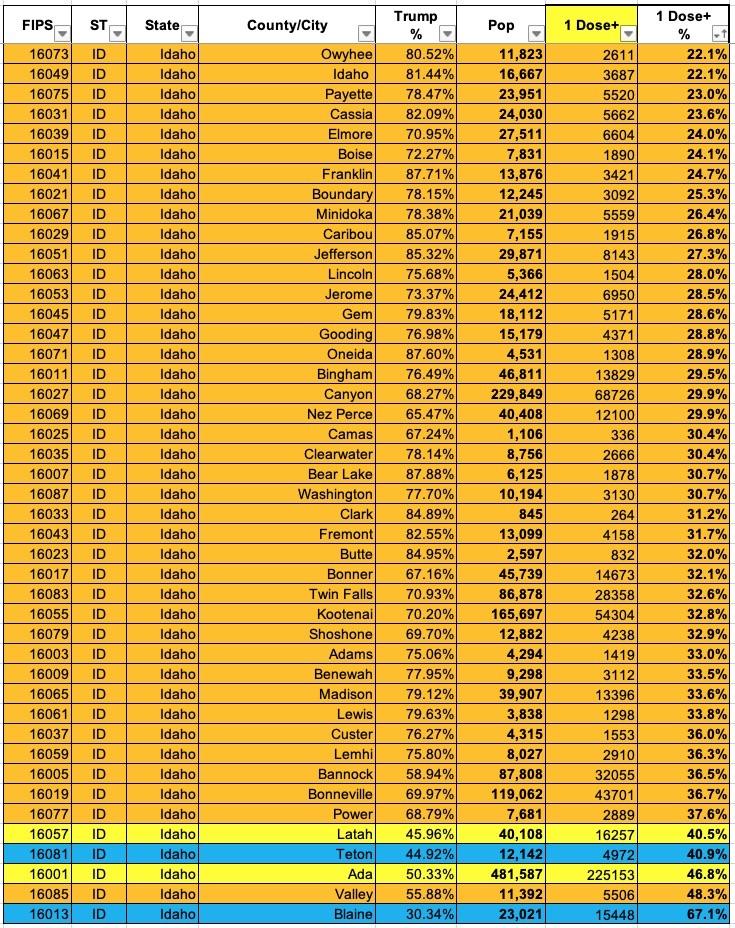

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

Note: The CDC lists ~323,000 New Jersey residents (8.1% of the total fully vaccinated) whose county of residence is unknown.

Huh. I'll have to double-check, but I believe New Jersey is the first state out of the 30 I've generated graphs for so far where the vaccination rate isn't higher in the more blue-leaning counties than the red-leaning ones. Of course, it's only an extremely slight tilt, and this is a blue state so even in the reddest county (Ocean), Trump still only received 63.5% of the vote, but it's still worth noting. NJ also has an unusually high percentage of vaccinated residents whose county of residence is unknown (over 8% of the total) which could be a factor as well.

New Jersey also happens to be the U.S. state with the highest cumulative COVID-19 death toll. I have no idea if that has anything to do with anything, but figured I should throw it out there.

Good news! More financial help is now available through Get Covered New Jersey

New Federal and State Savings

The federal government recently passed a COVID-19 relief bill, the American Rescue Plan Act of 2021, which was signed into law by President Biden on March 11, 2021. The new law will reduce health insurance premiums by providing more financial help to eligible consumers who purchase a plan through Get Covered New Jersey. The State of New Jersey is also providing more financial help to lower health insurance costs for residents enrolling at Get Covered New Jersey.

More people than ever will qualify for financial help. If you did not qualify for financial help before because your income was too high, you may qualify under the state and federal changes. If you already receive financial help, you will likely be eligible for additional premium reductions. These new changes make coverage more affordable at many income levels.

On January 29, 2021, the Department of Banking and Insurance (“Department”) issued Bulletin No. 21-03 advising carriers and other interested parties that an emergency COVID-19 Special Enrollment Period (“COVID-19 SEP”) would go into effect on February 1, 2021 and extend through May 15, 2021. The COVID-19 SEP ensured that New Jersey residents have access to quality affordable health insurance during a critical time in which the need to protect public health is paramount. Specifically, the COVID-19 SEP made sure that individual market coverage was available to uninsured individuals during the pandemic. It also aligned New Jersey with the Federal Special Enrollment Period which runs through May 15, 2021 and the Federal Public Health Emergency.

The American Rescue Plan & Additional Financial Relief

The federal government recently passed a COVID-19 relief bill, the American Rescue Plan Act of 2021, which was signed into law by President Biden on March 11, 2021. The new law will reduce health insurance premiums by providing more financial help to eligible consumers who purchase a plan through Get Covered New Jersey. Get Covered New Jersey is working to implement the changes and update its system to ensure that New Jerseyans receive this relief as soon as possible.

More people than ever will qualify for financial help. If you did not qualify for financial help before because your income was too high, you may qualify under the federal changes. If you already receive financial help, you will likely be eligible for additional premium reductions. These new changes make coverage more affordable at many income levels.

{kind=link}