Federal Government Announces 2020 Premium Rates

Website details proposed decreases for health plans to be sold in NH

CONCORD, NH – The federal government has published information on proposed rates for New Hampshire’s health insurance exchange (HealthCare.gov) in 2020.

The New Hampshire Insurance Department looks at premiums each year from a market-wide perspective, comparing the median premium for an on-exchange silver-level plan covering a 40-year-old non-tobacco-user. For 2019, the median premium at this level was $440; the median premium at this level for 2020 would be $429, based on the carriers’ proposed rates. If these rates are ultimately approved, this would represent a 2.5% decrease between next year’s and this year’s median premium in the individual market.

Sometimes I don't have anything particularly useful to add to a data point. New Hampshire is one of the very few states which don't operate their own ACA exchange which does keep track of (and, more importantly, report) ACA exchange enrollment on a regular basis, via a monthly report.

New Hampshire enrolled 44,581 people in individual market QHPs during open enrollment this year, so the 40,728 enrolled as of May shows an impressive 91% retention rate.

Their SHOP enrollment is around ~1,300 people working for ~230 small businesses.

Two states in two days...just 24 hours after the Washington State Insurance Commissioner pulled the plug on the "Aliera Healthcare" and "Trinity Healthshare" healthcare sharing ministries for fraud, the New Hampshire Insurance Dept. is issuing a similar warning (although they don't appear to be actually shutting the operation down just yet):

Consumer Alert on Potential Unlicensed Health Insurance Company

CONCORD, NH – As a result of a recent Georgia court order, the New Hampshire Insurance Department is advising consumers that Aliera, a company that markets itself as a health care sharing ministry, may be operating illegally in New Hampshire.

I realize this may seem a bit late in the game seeing how the 2019 ACA Open Enrollment Period has already started, but I do like to be as complete and thorough as possible, and there were still 9 states missing final/approved premium rate change analyses as of yesterday which I wanted to check off my 2019 Rate Hike Project list.

Fortunately, RateReview.HealthCare.Gov has finally updated their database to include the approved rate changes for every state, which made it easy to take care of most of these. In addition, in a few states the insurance department has also posted their own final/approved rate summary.

CONCORD, NH -- Open enrollment in the individual Health Insurance Marketplace will run from November 1 to December 15. In advance of open enrollment on and off the federally facilitated Marketplace, the New Hampshire Insurance Department offers information and resources for the approximately 54,000 state residents who will purchase health insurance in the individual market for 2019 coverage.

"We are encouraging New Hampshire residents who are buying a plan on Healthcare.gov to update their applications and actively compare plan options, “ said New Hampshire Insurance Commissioner John Elias. “Buying insurance is signing a contract. Once you lock in coverage, your rates and cost-sharing amounts will stay the same all year. But if you don’t sign up now, you will not have another chance to enroll until next year – unless you have a qualifying life event.”

With just 3 weeks to go before the 2019 Open Enrollment Period begins, the dust has mostly settled on my 2019 Rate Hike Project. Over half the states have provided their final, approved individual market premium changes, and while I haven't found the final rates for the other half yet, their preliminary rates are all on record, so I don't anticipate the needle moving too much at this point.

New Hampshire is among the states which I haven't found final rate changes for yet. The three carriers in the state have requested average price reductions of around 13.5% on average, which is well below the 3.2% increase which is the average nationally, but I still don't know what the state regulators are going to approve.

This makes the following press release rather surprising:

NH Insurance Department to Hold Oct. 30 Annual Public Hearing on Health Insurance Premiums

New Hampshire is perhaps the most striking example of both insurance carriers significantly overshooting the mark for 2018 premiums while also proving my point that just because premiums are dropping next year, #ACASabotage is still causing unsubsidized enrollees to pay a lot more than they'd have to otherwise.

All three of the carriers offering ACA policies on New Hampshire's individual market are reducing their 2019 premiums, by anywhere from 7.4% for Harvard Pilgrim to a whopping 15.2% in the case of Ambetter/Celtic.

THe enrollee market share numbers come from the monthly report from the New Hampshire insurance department (I'd love it if every state required one of these...it includes both on and off-exchange enrollees). The "PAP" column refers to NH residents enrolled in their "private option" Medicaid expansion program...but those are still part of the same risk pool as the other enrollees, so they still have to be factored into the market share formula.

As noted earlier today, I've now managed to plug 48 states (plus DC) into my 2018 Rate Hike Project spreadsheet. This leaves just two states missing: New Hampshire and Texas. I'm still waiting to clarify some things for each, so this analysis could still change, but I really want to wrap this up, so here's what I have for New Hampshire right now:

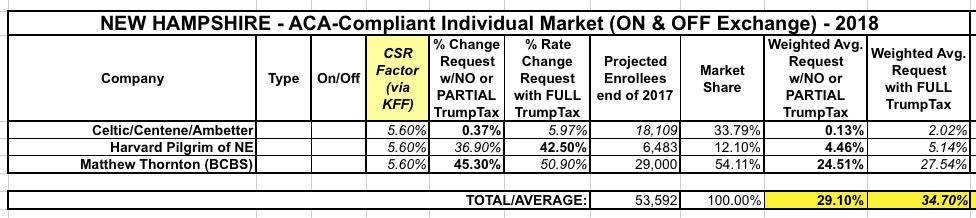

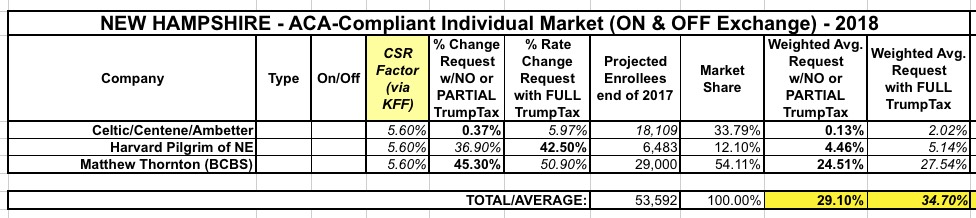

When I first ran the numbers for New Hampshire'srequested 2018 rate increases, it seemed pretty straightforward: 3 carriers on the individual market. 2 listed rate changes assuming CSRs would be paid; one assumed they wouldn't. This gave the following:

Did CMS execute a last-minute reversal on navigator program? That's what independent blogger Charles Gaba is reporting, posting what appear to be internal CMS documents that show the agency was poised to essentially renew last year's funding for this year's ACA open enrollment.

One document posted by Gaba indicates that Randy Pate — tapped by the Trump administration to run Medicare's Center for Consumer Information and Insurance Oversight — signed off on $60 million in program funding on Aug. 24. More. However, CMS ultimately funded the program at less than $37 million for the upcoming enrollment, a 41 percent cut from last year.

New Hampshire's a bit of a head-scratcher this year: Of the three carriers on the individual exchange next year (each of whcih has a significant chunk of the market), Centene is requesting virtually no rate increases whatsoever...while the other two are asking to raise their rates by over 40% apiece.

Even more odd: Harvard Pilgrim's 42.5% seems to assume the worst regarding CSRs/mandate enforcement...yet Matthew Thornton (BCBS) is asking for 45.3% while assuming CSRs will be paid.

Finally, Kaiser assumes around a 10% Silver rate increase in NH if CSRs aren't paid, which translates into about 5.6% spread across the entire membership. Result: 29.1% if CSRs are paid, 34.7% if they aren't.