New Hampshire: Preliminary 2019 #ACA rates: 13.5% DROP...but would have dropped by up to *26%* without #ACASabotage

Sun, 08/05/2018 - 10:57am

New Hampshire is perhaps the most striking example of both insurance carriers significantly overshooting the mark for 2018 premiums while also proving my point that just because premiums are dropping next year, #ACASabotage is still causing unsubsidized enrollees to pay a lot more than they'd have to otherwise.

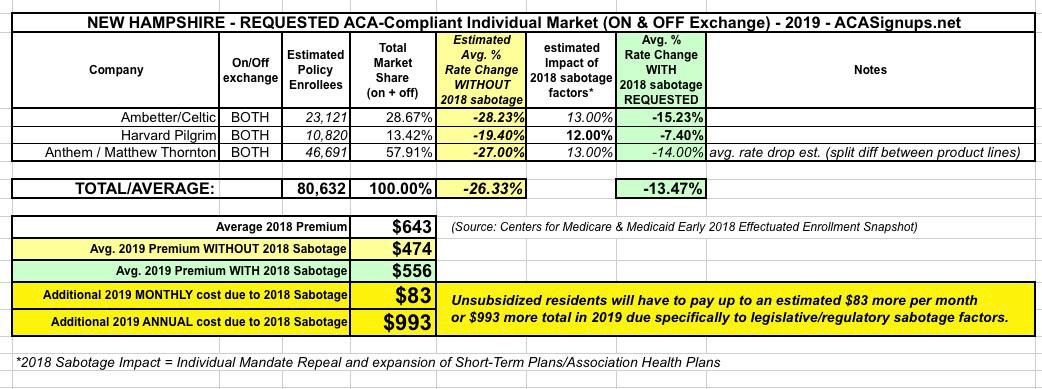

All three of the carriers offering ACA policies on New Hampshire's individual market are reducing their 2019 premiums, by anywhere from 7.4% for Harvard Pilgrim to a whopping 15.2% in the case of Ambetter/Celtic.

THe enrollee market share numbers come from the monthly report from the New Hampshire insurance department (I'd love it if every state required one of these...it includes both on and off-exchange enrollees). The "PAP" column refers to NH residents enrolled in their "private option" Medicaid expansion program...but those are still part of the same risk pool as the other enrollees, so they still have to be factored into the market share formula.

The average premium decrease is an eyebrow-raising 13.5%. This is the greatest reduction in ACA premiums I've see so far this year, made all the more unusual by that fact that New Hampshire doesn't have a new reinsurance program or Medicaid expansion factor to take into account. Basically, all three carriers simply overestimated how much their costs would go up this year.

Here's the key thing, however: Some people may be skeptical about the "sabotage" factor--after all, rates are dropping, right?

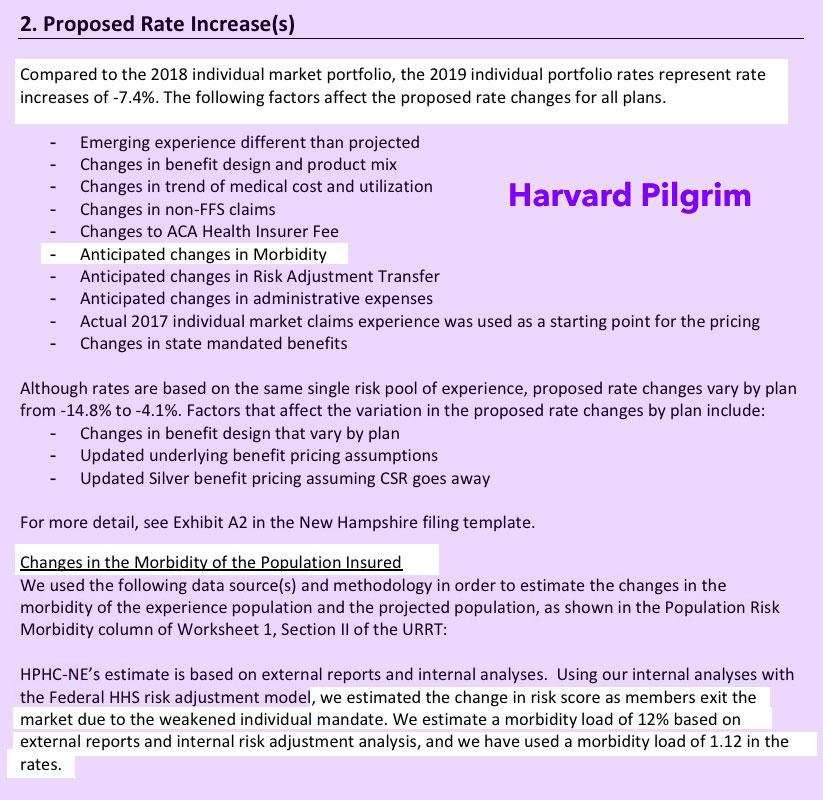

Yes...but take a look at Harvard Pilgrim's rate filing, where they clearly lay it out:

- 2019 rates are dropping by 7.4%.

- 2019 rates are increasing by 12% due to morbidity changes...which are based specifically on the adverse selection impact of the individual mandate being repealed.

In other words, they would have dropped rates by around 28%, but then had to raise them back up again by 12 points due to mandate repeal, for a final drop of around 15.2%.

The other two carriers don't break out the mandate repeal or #ShortAssPlans impact (in fact, they're both redacted), but the 12% for Harvard Pilgrim is very close to the 13% ballpark estimate I'm using (based on 2/3 of the Urban Institute's estimates), so I'd say that's a pretty good rule of thumb.

Average premiums are $643/month this year for unsubsidized enrollees. That means 2019 premiums would have dropped by nearly $1,000 more per enrollee next year if the mandate hadn't been repealed and non-ACA compliant short-term plans hadn't been expanded.

Advertisement