Of the 31 states which have expanded Medicaid under the Affordable Care Act, only a handful issue regular monthly or weekly enrollment reports.

I noted in February that enrollment in the ACA's Medicaid expansion program had increased by around 35,000 people across just 4 states (LA, MI, MN & PA).

It's early June now, so I checked in once more, and the numbers have continued to grow. I have the direct links for 5 states now (including New Hampshire)...

Of course, as I (and others on both sides of the political spectrum) have written about many, many times, not everyone who selects a QHP (either on or off the exchanges) actually pays their first premium, and therefore is never actually enrolled in an active, effectuated policy. This amounted to roughly 12-13% of all QHP selections in 2014, but has improved over the past 3 years as people got used to how the system works and technical improvements were made. I've been using a 10% non-payment rate as a general rule of thumb for some time now.

In New Hampshire, assuming 58,000 people enroll in private exchange policies by the end of January, I estimate around 31,000 of them would be forced off of their private policy upon an immediate-effect full ACA repeal, plus another 50,000 enrolled in the ACA Medicaid expansion program, for a total of 81,000 residents kicked to the curb.

As for the individual market, my standard methodology applies:

(sigh) OK, with three states still missing, you just knew I wouldn't rest until I was able to fill in the missing pieces of the puzzle. Sometime today, the HHS Dept. finally entered the approved rate hikes for individual makret carriers in two of those states: New Hampshire and Virginia. Louisiana is still AWOL for whatever reason.

It's important to note that sometimes the "Final Rate Increase" percentages listed at RateReview.HealthCare.Gov dont' actually end up matching the approved rate hikes found in the official SERFF databases or even at the state's Dept. of Insurance website. Normally I cross-check all three to make sure nothing weird is going on, but given that it's well past time to move on, I'm relying purely on the RateReview numbers for these states.

With that in mind, here's what it looks like in each:

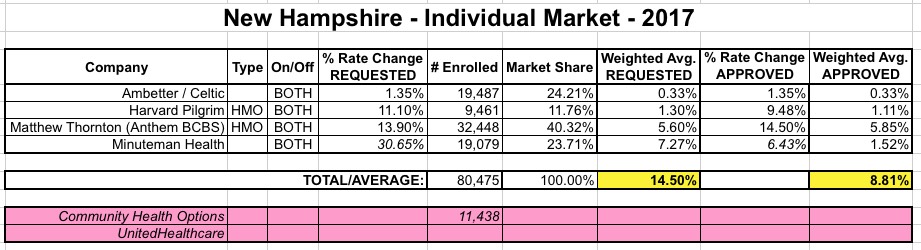

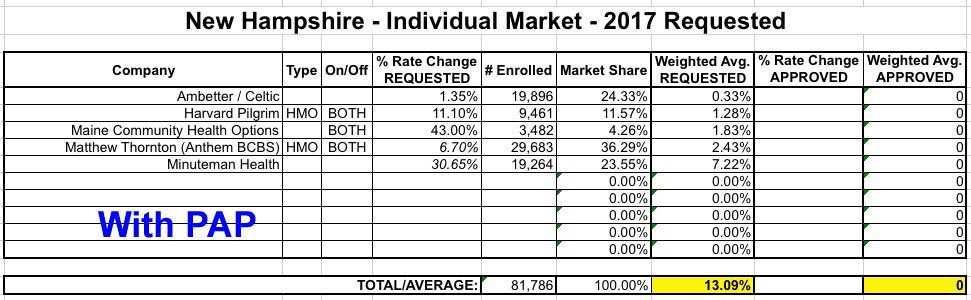

When I originally calculated the average requested rate hike for New Hampshire, I came up with a weighted estimate of around 13.1%. A month later, the average dropped a few points...but not for a good reason: One of the remaining ACA-created Co-Ops, Community Health Options, decided to pull out of New Hampshire (they started out as a Maine-only operation, expaneded into nearby NH for the 2nd and 3rd year, but are pulling back to Maine-only again). Since CHO would otherwise have been requesting a more than 40% increase, them dropping out actually lowered the average increase for everyone else. This obviously illustrates a major caveat with my "average rate increase" methodology: It only applies to those who are able to renew their existing plans. The moment a carrier pulls out of parts/all of a state, or drops PPOs (while keeping HMOs), etc, I have to remove a portion of the existing enrollees from the equation completely.

Community Health Options, a Lewiston-based health insurance cooperative, has gotten approval to withdraw from the New Hampshire insurance market in 2017.

The plan was approved this week by the Maine Bureau of Insurance, which has been monitoring CHO’s finances as it tries to recover from a $31 million loss in 2015. The nonprofit cooperative has set aside more than $45 million in reserves to try to avoid another big loss this year.

Of course, as I (and others on both sides of the political spectrum) have written about many, many times, not everyone who selects a QHP (either on or off the exchanges) actually pays their first premium, and therefore is never actually enrolled in an active, effectuated policy. This amounted to roughly 12-13% of all QHP selections in 2014, but got a bit better over the next two years as people got used to how the system works and technical improvements were made. In addition, another chunk of QHP selections were scrapped by the HHS Dept. or state exchanges at later points thorughout 2014 for a variety of reasons ranging from legal residency issues to other data matching problems. Again, this percentage has been gradually whittled down as improvements to the system have been made.

New Hampshire has only 5 carriers offering individual market policies, all 5 of which will still be participating in the NH market next year as well. Two of the five (Community Health Options and Minuteman Health) are among the 7 surviving ACA-created Co-Ops.

Even so, NH is proving to be a very tricky state to estimate, because only one of the 5 carrier rate filings includes their actual current rate-impacted enrollment data. As a result, I've had to take my best shot at estimating the market share of the other four. The only way I could think of to do this was to look up the latest NH DOI 2016 QHP Monthly Membership Report. New Hampshire, to their credit, is one of the only states without their own state-based ACA exchange which still actually posts regular reports about how many residents are enrolled in ACA exchange policies. Furthermore, they even break these numbers out by metal level and carrier, making the relative market share easy to calculate.

A few weeks ago I reported on some weirdness in New Hampshire's monthly exchange QHP enrollment data. They were showing an unusually high effectuated enrollment drop-off between March and April, especially odd considering that enrollment had supposedly increased from February to March.