The Connecticut Insurance Department is reviewing 14 health insurance rate filings for the 2019 individual and small group markets. The filings were made by 10 health insurers for plans that currently cover about 293,000 people.

Two carriers – Anthem and ConnectiCare Benefits Inc. (CBI) – have filed rates for both individual and small group plans that will be marketed through Access Health CT, the state-sponsored health insurance exchange.

The 2019 proposed rate increases for both the individual and small group market are, on average lower, than last year:

“Our rate reduction would have been larger, but we had to account for added uncertainty in our rates due to indefinite suspension (the U.S. Centers for Medicare and Medicaid Services) placed on risk adjustment transfers between insurers,” said , said Mary Danielson, a BCBST spokeswoman. “Again, we were planning a larger reduction – around 18 percent – but needed to factor in the prospect of greater costs for 2019.”

The cost of plans through Nevada’s health insurance exchange are anticipated to only increase by an average of 1.9 percent next year in what the state’s insurance commissioner said is the lowest proposed rate increase from insurance companies since the Affordable Care Act went into effect in 2014.

The announcement, made by the Division of Insurance late Tuesday morning, comes amid ongoing uncertainty about the impact that Congress’s repeal of the Affordable Care Act’s individual mandate and federal rule changes for two types of non-ACA-compliant health plans will have on the individual market as a whole. Insurance Commissioner Barbara Richardson cautioned that the proposed rates are subject to change based on any action by the federal government and said the division is working “diligently” to review the proposed rates from insurance companies.

That 1.9% figure is slightly misleading, though, because...

This year, thanks to their reinsurance program, ACA individual market premiums dropped by around 23.6% on average, from a whopping $1,040/month to "only" $795/month per enrollee.

No Load: They could gamble that the CSR problem would be resolved and the payments would be made after all (i.e., they would price normally).

Broad Load: They could spread the CSR cost out evenly across all of their 2018 ACA policies, on exchange & off.

Silver Load: They could load the CSR costs onto all Silver plans only (both on & off exchange).

Silver Switcharoo: They could load CSR costs onto all on-exchange Silver plans only, while also creating "mirror" Silver plans off-exchange without any CSR load.

Mixed Load: Each insurance carrier could choose whichever of the other 4 strategies they wanted to and let the chips fall where they may. Not sure if this really counts as a "strategy", since it's more or less "all of the above".

DENVER (July 13, 2018) – The Colorado Division of Insurance, part of the Department of Regulatory Agencies (DORA), today released preliminary information for proposed health plans and premiums for 2019 for individuals and small groups. Colorado consumers can file formal comments on these plans through August 3.

2018 Companies Return for 2019 The same seven companies that offered on-exchange, individual plans are returning for 2019 - Anthem (as HMO Colorado), Bright Health, Cigna Health and Life, Denver Health Medical Plans, Friday Health Plans, Kaiser Foundation Health Plan of Colorado and Rocky Mountain HMO. And like in past years, this means that all counties in Colorado will have at least one on-exchange company selling individual health plans.

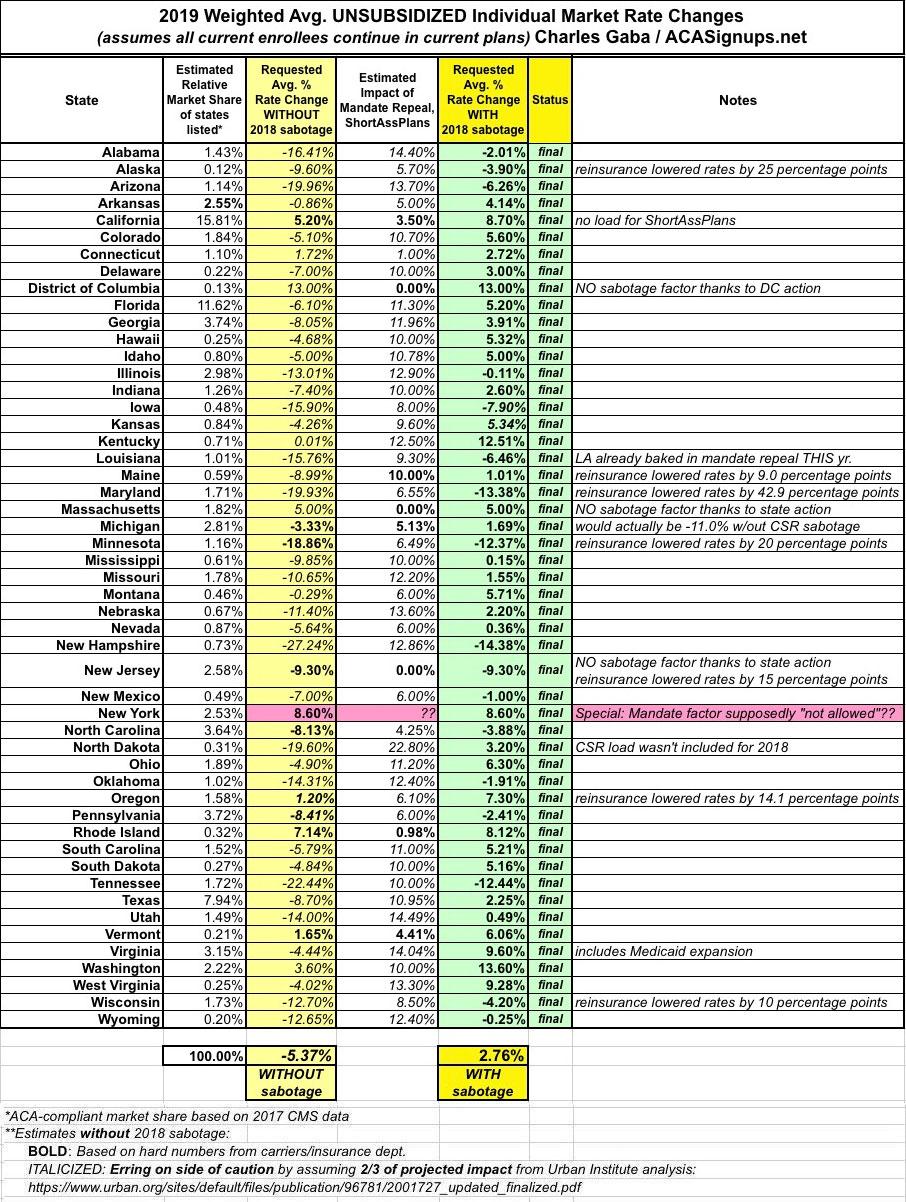

Holy guacamole. I've noted repeatedly that unlike last fall, when average rate increases of 20-30% or more were commonplace for ACA individual market policies (due mainly to Trump cutting off CSR reimbursement payments), the preliminary rate requests for 2019 are actually averageing quite a bit lower than originally expected; of the 20 or so states I've crunched the numbers for so far, the weighted average for unsubsidized premium hikes is hovering around the 10% mark.

At first glance, it may sound like Democrats have been overplaying their hand when it comes to the "individual mandate repeal/short-term plan expansion is causing massive hikes!" attack. However, the rate increases from deliberate sabotage are happening...they're just being partly cancelled out by other factors, including:

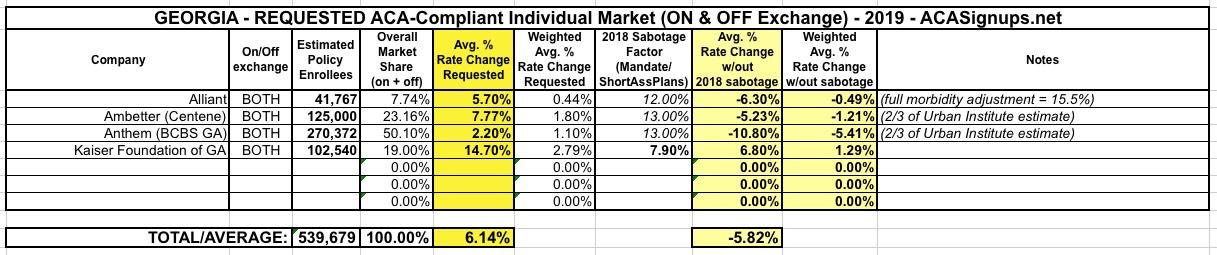

Whew! Georgia only has 4 carriers participating in the individual market, but tracking down some of the data was a royal pain in the butt, especially Ambetter/Centene, which not only buried the numbers I needed inside a whopping 1,900-page PDF file, but the actual average requested rate increase wasn't even included; for that I had to check a different file. Yeesh.

The good news is that carriers in Georgia are only requesting around a 6.1% average rate increase for ACA-compliant individual market policies next year.

The bad news is that if it weren't for the ACA's individual mandate being repealed and the Trump Administration's expansion of #ShortAssPlans, 2019 premiums would likely be dropping by around 5.8% instead.

*(OK, these are technically only "semi-approved" rates...there could still be some additional tweaks later on after public comment, etc.)

Oregon was the fourth state which I ran a preliminary 2019 rate increase analysis on back in May. At the time, I concluded that insurance carriers were requesting a weighted average increase of 10.5% for ACA-compliant individual market policies next year. I knew that Oregon's state-based Reinsurance program was helping keep that average down to some degree, but I didn't know exactly how much of a factor it was.

I also knew that efforts to sabotage the ACA by Donald Trump and Congressional Republicans would play a major role in increasing 2019 rates: Repeal of the individual mandate is a big factor, along with the unnecessary 1-point increase in the state exchange fee being imposed on Oregon and the other four states which run their own exchange but "piggyback" on HealthCare.Gov's technology platform.