Tennessee: Preliminary 2019 #ACA rate change: 5.7% decrease...but guess what it would be without ACA sabotage?

Fri, 07/13/2018 - 12:36am

Holy guacamole. I've noted repeatedly that unlike last fall, when average rate increases of 20-30% or more were commonplace for ACA individual market policies (due mainly to Trump cutting off CSR reimbursement payments), the preliminary rate requests for 2019 are actually averageing quite a bit lower than originally expected; of the 20 or so states I've crunched the numbers for so far, the weighted average for unsubsidized premium hikes is hovering around the 10% mark.

At first glance, it may sound like Democrats have been overplaying their hand when it comes to the "individual mandate repeal/short-term plan expansion is causing massive hikes!" attack. However, the rate increases from deliberate sabotage are happening...they're just being partly cancelled out by other factors, including:

- Many carriers overshot the mark this year, raising their 2018 premiums more than was necessary to absorb last year's sabotage efforts, so they have to lower premiums somewhat next year so as not to violate, ironically, the ACA's 80/20 MLR rule. In this sense, the ACA is working exactly as it's supposed to.

- The ACA's Health Insurer Tax (which I believe amounts to around 2% of the premium cost) was once again "holidayed" (it was charged in 2014 & 2015, waived i 2016 & 2017, is being charged in 2018 but isn't being charged in 2019).

With this in mind, I greatly appreciate this post from a blog called "Bird Dog", which is apparently dedicated to all things Tennessee-related, and which includes some additional factors...not all of which are a good thing:

Insurers angling to sell on the Tennessee individual health insurance market in 2019 filed their premium requests with the state July 11 — and some premiums will fall even as insurers plan for fewer healthy people to enroll.

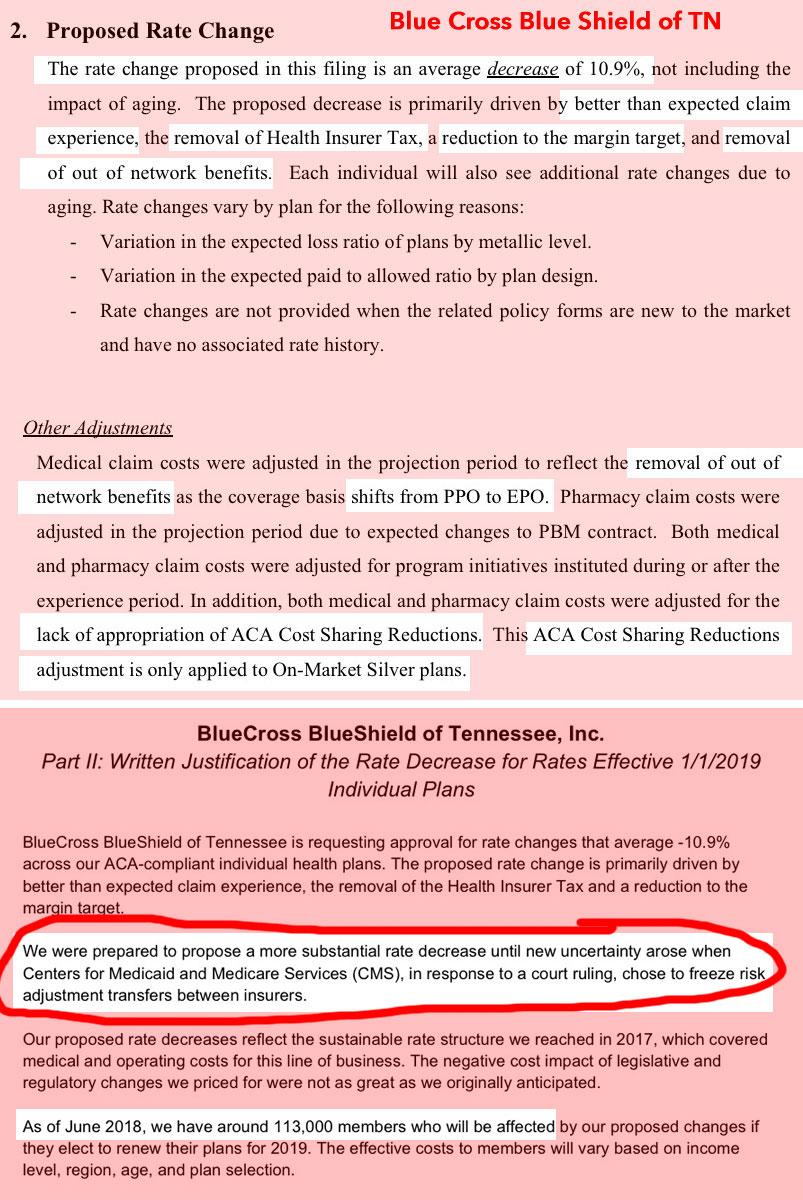

...But, BCBST — one of the insurers in the U.S. with the most payments on the line, according to Axios — filed its request on the deadline: It requested an average 10.9 percent decrease although it had planned for an 18 percent decrease until the HHS announcement.

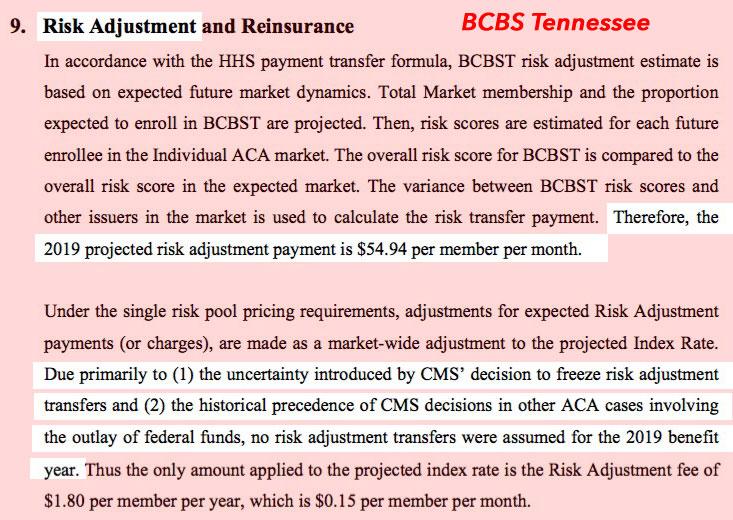

The insurer has been expecting $75.8 million in estimated payments from HHS in relation to the individual and small group plans it offered on the federal exchange for 2017 and 2018, said Danielson.

“Our rate reduction would have been larger, but we had to account for added uncertainty in our rates due to indefinite suspension (the U.S. Centers for Medicare and Medicaid Services) placed on risk adjustment transfers between insurers,” said , said Mary Danielson, a BCBST spokeswoman. “Again, we were planning a larger reduction – around 18 percent – but needed to factor in the prospect of greater costs for 2019.”

Yes, that's right: Blue Cross Blue Shield of Tennessee, which enrolls over 50% of TN's entire ACA-compliant individual market, was planning on dropping average premiums by a whopping 18% until Trump's CMS Dept. decided to freeze Risk Adjustment transfers for no legitimate reason whatsoever.

18 - 10.9 = 7.1 percentage points. Tennessee's unsubsidized premiums average $803/month this year, so that means they're tacking on around $58/month or $680/year per enrollee just to account for the frozen RA payments.

UPDATE: Strike that...the filing actually provides the exact dollar amount:

OK, it's slightly lower: $54.94 per month, or $649 per enrollee for the full year.

Does this sound excessive? Well, BCBSTN has 113,000 enrollees. 113K x $649 = $73.3 million...almost exactly what they're owed in RA payments.

This may change if CMS changes their mind and decides to make the 2017 RA payments after all, but if they don't, 113,000 Tennessee residents will have to pay an extra $680 next year for no reason.

BUT WAIT, THERE'S MORE!

Remember, the RA thing is on top of the other big sabotage factors this year: Repeal of the ACA's individual mandate and the expansion of #ShortAssPlans. Those are, as usual, specifically called out by most of the TN carriers as well. None of them break the impact out specifically, so I'm once again using my standard estimate: 2/3 of what the Urban Institute projected these factors to be. In the case of Tennessee, Urban estimated around 18.1 percentage points would be tacked on, so I'm assuming this to be around 12 points to err on the side of caution.

The #ShortAssPlans factor is even mentioned by new entrants to the ACA market. There's three this year (BCBS, Cigna and Oscar), but two more (Bright and Centene/Ambetter) are jumping in...but pricing accordingly:

Insurers are expecting HHS regulations regarding short-term and association plans to strip out some of the shoppers who are younger, healthier, and therefore lower cost, according to filings.

“The change in regulations is anticipated to cause some young and healthy, lower cost members to migrate from the ACA individual market. Therefore, a larger proportion of higher cost people will remain in the overall risk pool of the ACA individual market, generating increased adverse selection and morbidity,” new entrant Bright Health wrote in its TDCI filing.

With all that in mind, here's what things look like at the moment for the 2019 Tennessee ACA individual market:

I had to estimate Oscar's market share based on TN's total indy market size, but it should be around 31,000 people. Neither Bright nor Centene/Ambetter have any impact on average premium changes since they don't have any enrollees at the moment to begin with.

Therefore, Tennessee enrollees are looking at roughly a 5.7% average premium drop next year, which is good news...except that, assuming the Urban Institute's estimates are even close to being accurate, if the mandate hadn't been repealed, #ShortAssPlans weren't being expanded and Risk Adjustment payments weren't at risk of not being paid, the average premium rates would drop by around 21% instead (neither Cigna nor Oscar are owed any money, so there's no RA freeze impact to them).

In fact, assuming that 12 point estimate is true for BCBSTN specifically, this also suggests that they'd be dropping 2019 rates by up to a stunning 30% if you removed all of this year's sabotage factors. As always, I'll modify/update my estimates if/when individual carriers issue clarifications on this point. It sounds like they seriously overshot this year.

Oh, one more thing regarding the CSR load: As you can see in the filing screen shots below, there's also several statements which confirm that Tennessee will be shifting from "standard" Silver Loading to the full "Silver Switcharoo" next year, which is a good thing:

Advertisement