So far, only 4 states have released their preliminary 2019 ACA-compliant individual market premium rate filings: Maryland, Virginia, Vermont and Oregon.

However, it's a bit overly cumbersome for my purposes: It stretches out over 6 full pages, and includes columns for Standalone Dental Plans as well as a bunch of info regarding the Small Group Market. I did used to try tracking Small Group rates as well, but that got to be too difficult to keep up with, and I haven't really done much analysis of standalone dental plans at all. Let's face it: About 90% of the drama, controversy and confusion regarding ACA premiums is all about the individual market.

Eleven health insurers file for 2019 individual market: No bare counties

May 25, 2018

OLYMPIA, Wash. – Eleven health insurers filed 88 health plans for Washington state’s individual market yesterday, and all 39 counties will be covered in 2019.

The proposed rate changes are not public until 10 days after the OIC has determined the filings are complete. Release of the proposed rate changes is targeted for June 4.

“We can all breathe a sigh of relief knowing consumers in every county who need coverage will have access to a health plan in 2019,” said Insurance Commissioner Mike Kreidler. “Obviously, how much premiums may change and any increases to out-of-pocket costs are still key concerns, but I’m grateful that we can assure people that coverage is available, regardless of where they live.”

One of the things Ford had always found hardest to understand about humans was their habit of continually stating and repeating the very very obvious, as in ‘It’s a nice day’, 'You’re very tall’, or 'You seem to have fallen down a thirty-foot well, are you alright?’

--Douglas Adams, The Hitchhiker's Guide to the Galaxy

A top insurance industry official said Wednesday that he expects “substantial” ObamaCare premium increases for 2019.

Kris Haltmeyer, a vice president at the Blue Cross Blue Shield Association, told reporters that the premium increases were in part due to the repeal of ObamaCare’s individual mandate in the Republican tax reform bill in December. He also cited lawmakers’ failure to pass a bill aimed at lowering premiums, which fell apart earlier this year amid a partisan dispute over abortion restrictions.

It's become a tradition that every spring/summer/fall, I pore over the official SERFF database for every state, furiously searching for the ACA-compliant rate filings for the upcoming year.

The thing is, the SERFF database, in addition to being somewhat confusing and clunky to work with, includes a lot more than just "here's how much we want to raise our rates next year". Even after narrowing it down to just major medical health insurance policies, there are often still dozens of different forms and spreadsheets in the database, covering pretty much any change to any insurance policy for any carrier. If a carrier drops out of a market, there are forms. If they stop offering PPOs, there are forms. If they merge with or buy out another company, there are obviously forms. Even for the rate filings themselves, there are often a dozen or more different PDFs and/or spreadsheets included as supporting documentation.

OK, this doesn't technically count as an official 2019 Rate Hike analysis since none of it comes from actual carrier rate filings, but Covered California, the largest state-based ACA exchange, just released their proposed 2018-2019 annual budget, and it includes detailed projections regarding expected premium increases and enrollment impact over the next few years due specifically to the GOP's repeal of the ACA's Individual Mandate. Oddly, while they mention short-term plan expansion as another potential threat to enrollment/premiums, they do so passingly, and they don't mention association plans at all:

Since 2014, nearly 5 million people have enrolled in Medi-Cal due to the Affordable Care Act expansion, and more than 3.5 million have been insured for some period of time through Covered California. Together, the gains cut the rate of the uninsured in California from 17 percent in 2013 to a historic low of 6.8 percent as of June 2017.

Oregon just became the 4th state to submit their preliminary 2019 ACA individual market rate filings, and while the expected increase is smaller than expected on average (in part due to Oregon's strict control of short-term plans), repeal of the individual mandate by Congressional Republicans and Donald Trump are still responsible for the vast majority of the rate increase.

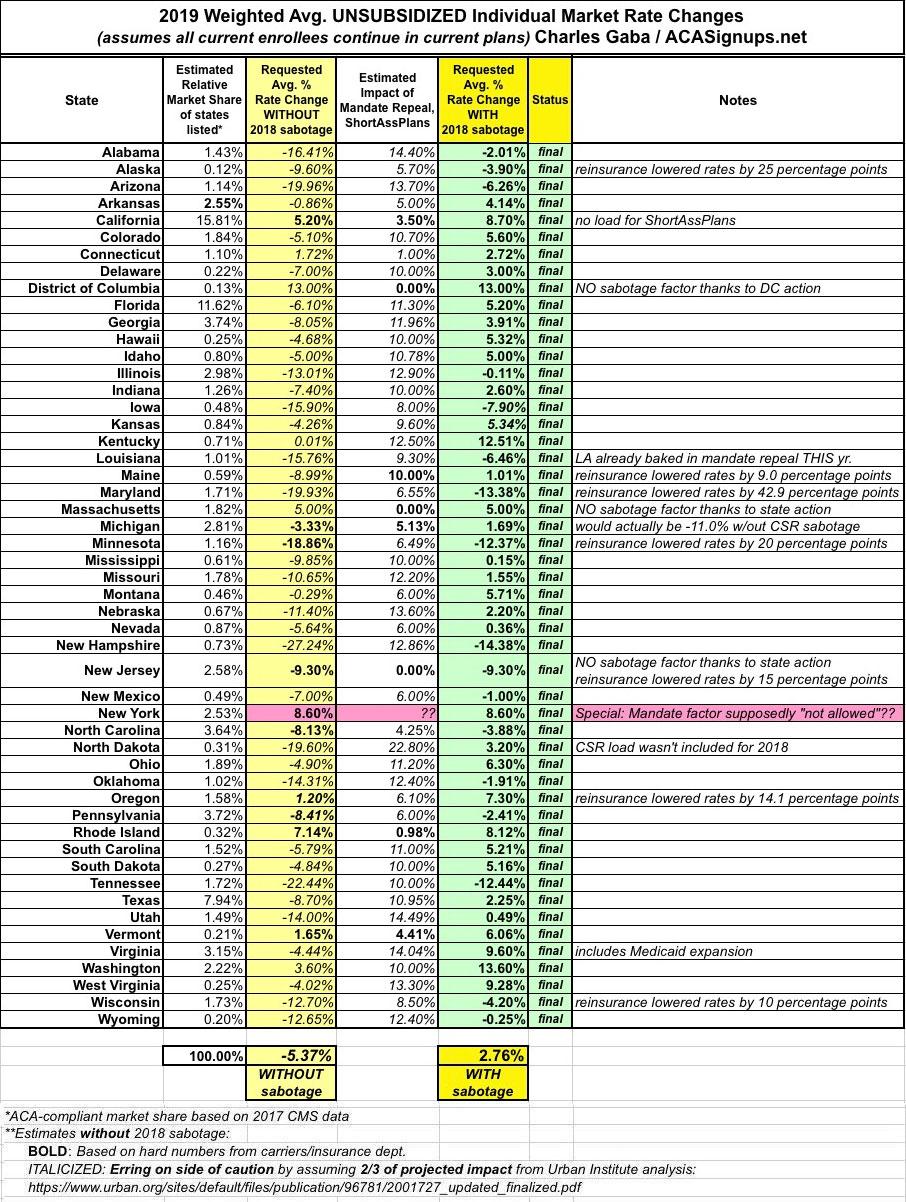

Normally, I don't start posting natoinal projections for my annual Rate Hike Project until I have at least filing data for at least a dozen or so states because the national weighted average jumps around so much early on. A "national average" of, say, 10% based on numbers from, say, Vermont, Wyoming and the District of Columbia (collective population: 1.9 million people) is gonna change radically once you add California or Florida to the mix if they're looking at a 20% hike, for example.

Having said that, seeing how advocacy organization Protect Our Care has decided to launch their own version of my Rate Hike Project, and seeing how I do have preliminary 2019 rate increase projections from at one large state (Virginia) and two mid-sized states (Maryland and Oregon), I've decided to go ahead and start posting the national projections early, with a major caveat that the national average will likely change dramatically until at least 2/3 of the states have been plugged in.

For three years now, I've been painstakingly tracking the annual average rate increases for ACA-compliant individual market policies across all 50 states (+DC) and nationally, including both the on & off-exchange markets in as much detail as possible, and at the risk of tooting my own horn too much, my track record on this has been pretty damned accurate:

Given how progressive Vermont is, you'd think that they'd be doing as much as possible to batten down the hatches in order to avoid or mitigate the latest wave of sabotage efforts from the Trump Administration and the GOP...and you'd mostly be correct.

Some of the work on that front has already been done. For one thing, Vermont (along with Massachusetts and the District of Columbia) merges their individual and small group market risk pools together, which helps smooth out premium increases and overall morbidity across a larger risk pool. For another, Vermont has fully embraced ACA provisions such as Medicaid expansion and operating their own full exchange, of course. Vermont, along with a few other states, also has pretty strict rules in place limiting both short-term and association healthcare plans, so that portion of Trump's sabotage attack is neatly cancelled out already.