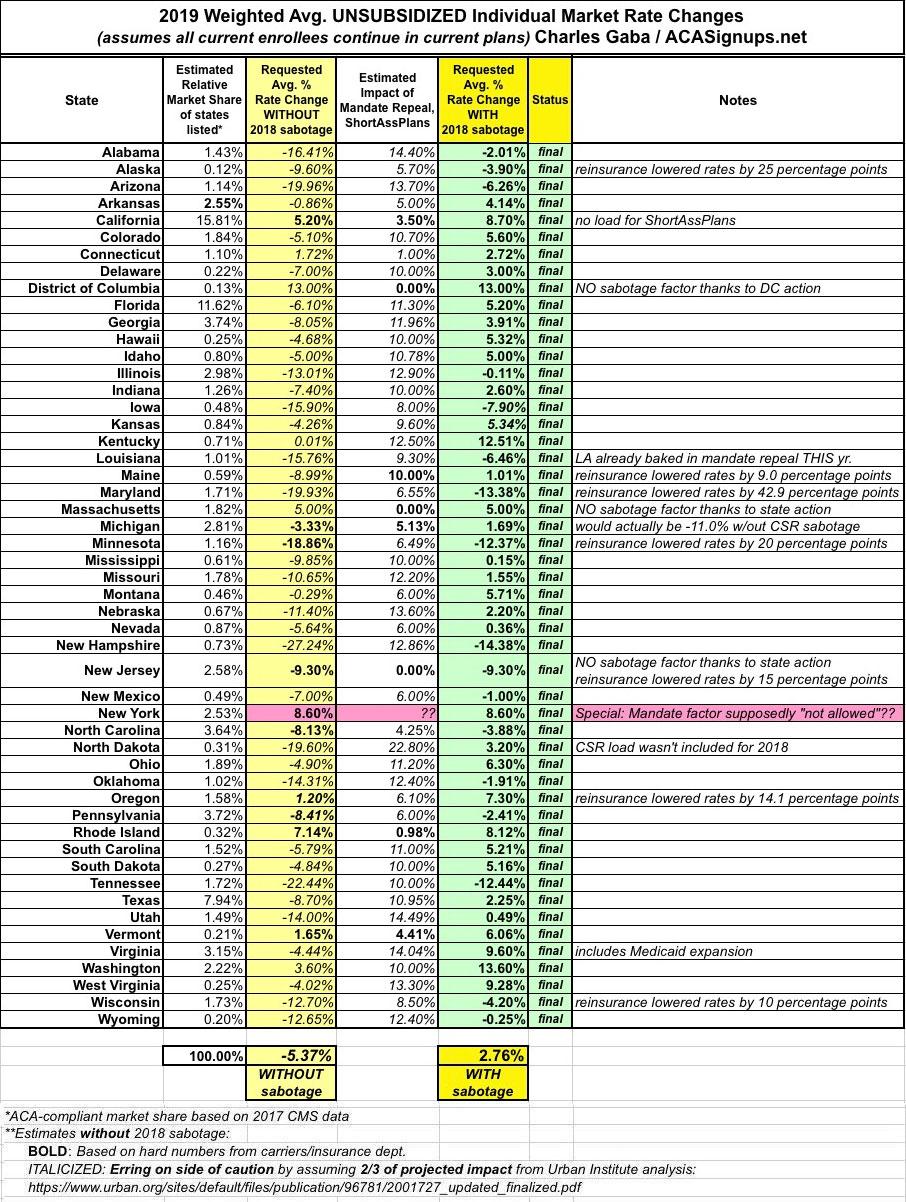

NOTE: I originally missed two carriers (McLaren and Molina); thanks to Louise Norris for calling attention to my error. The entire post, along with the table, has been updated to reflect the updated numbers including all 11 carriers.

Also note that while the headline originally reflected what the average rate change would be without the CSR load sabotage factor introduced in 2017, I've decided to be consistent with other states and only include 2018 sabotage impact.

My home state of Michigan just posted their preliminary requested rate changes for the 2019 Open Enrollment Period, and unlike most of the other states which have released their early requests so far, Michigan is a pleasant surprise: An overall average requested premium increase of just 1.7%!

Also noteworthy: According to the filings, eight of the carriers are specifically projecting exactly a 5% mandate repeal factor, which is remarkably consistent (usually the projections are all over the place). HAP is slightly lower (4.4%) while Molina is higher (7.2%). Priority Health didn't mention this at all, but it's safe to assume it'd be roughly 5% for them as well.

Tax Credits Through MNsure Can Help Lower Proposed Premiums for 2019

June 14, 2018

DULUTH, Minn.—Preliminary health insurance rates proposed by Minnesota health insurance companies will be available on the Minnesota Department of Commerce website on Friday, June 15.

Private insurance companies set premium prices, and the Minnesota Department of Commerce regulates those companies. Final, approved 2019 premium rates will be available by October 2, and the 2019 open enrollment period begins on November 1. Minnesotans shopping for health insurance through the individual market may be able to reduce premium costs in three ways:

1. See if you are eligible for tax credits only available through MNsure

Rate filings were due in New Mexico by June 10, 2018, for insurers that wish to offer individual market plans in 2019. Insurers that offer on-exchange coverage have been instructed by the New Mexico Office of the Superintendent of Insurance (NMOSI) to add the cost of cost-sharing reductions (CSR) only to on-exchange silver plans and the identical versions of those plans offered off-exchange (different silver plans offered only off-exchange will not have the cost of CSR added to their premiums).

The past two days have brought a flurry of 2019 premium rate change filings, with Washington, New York, Maine, DC and Pennsylvania putting their preliminary cards on the table. These join 5 other states which had already posted their early numbers, so I now have 10 compiled.

Now that I have a solid amount of state data to work with, I figured I should write up a tutorial to explain my methodology. This has become especially important the past two years since there's some new factors to consider.

Health Insurance Plan Rates Stabilize, Offer More Choice for Consumers Despite Federal Government Sabotage

Harrisburg, PA – Insurance Commissioner Jessica Altman today announced that health insurance rates in Pennsylvania have moderated significantly, counter to the national trend, after Wolf Administration efforts to combat the effects of sabotage on health insurance markets by the federal government and specifically the Trump Administration to dismantle the Affordable Care Act (ACA). Importantly, the filings indicate that rate increases in Pennsylvania will be significantly more modest in 2019 than other states and many consumers will see more choices in their local markets as a result of Pennsylvania's efforts to increase competition.

One important twist: A few months back I remember reading that Maine, like several other states, was considering establishing some type of reinsurance program along the lines of successful programs in Alaska, Minnesota and Oregon. I also remember reading that the Maine version was unusual--it would actually involve reestablishing an old, discontinued state program which was still on the books but had been mothballed for years. However, I never got around to doing a write-up about it.

Hot on the heels of Washington State releasing their preliminary 2019 individual market rate hike request comes a similar press release out of the New York Department of Financial Services...and neither the carriers nor the state regulators are making any bones about the reason for next year's rate increases:

PROPOSED 2019 HEALTH INSURANCE PREMIUM RATES FOR INDIVIDUAL AND SMALL GROUP MARKETS

Health insurers in New York have submitted their requested rates for 2019, as set forth in the charts below. These are the rates proposed by health insurers, and have not been approved by DFS.

OLYMPIA, Wash. – Eleven health insurers filed 74 health plans for Washington state’s 2019 individual and family health insurance market, with an average proposed rate increase of 19.08 percent. There are no bare counties, although 14 counties will have only one insurer selling through Washington’s Exchange, Washington Healthplanfinder.

Several quick tidbits out of the District of Columbia from the DC Health Benefit Exchange Authority May board meeting:

Their preliminary 2019 premium rate filings were originally due by May 1st, but this was bumped out until June 1st. Not available publicly yet, however.

The board voted unanimously to restrict Short-Term, Limited Duration plans to no more than 3 months at a time and to make them non-renewable in order to prevent them from further damaging the ACA individual market. They basically went with the parameters laid out under the newly-signed Maryland law. This won't become official unless the DC Council approves it, however (which I strongly suspect will happen).

As shown below, things are pretty cut & dry in Rhode Island; they only have 2 carriers participating in the individual market (Blue Cross Blue Shield and Neighborhood Health Plan). BCBSRI is asking for a 10.7% average increase, while Neighborhood is requesting 8.7% overall.

The estimated market share ratios are based on this press release from HealthSourceRI, the state ACA exchange. That doesn't include the final numbers or the off-exchange enrollment, but it should be pretty close, as there are only 2 carriers and their requested increases are so close to begin with it wouldn't make much difference. The weighted average is 9.3%.