Every year, I spend months painstakingly tracking every insurance carrier rate filing (nearly 400 for 2025!) for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

I really only need three pieces of information for each carrier:

This is gonna be one of the stranger references I've made on this site, but bear with me.

Back in 1996 there was an HBO movie called "The Late Shift" which told the story of the Late Night TV show battle between David Letterman and Jay Leno over who would succeed Johnny Carson as host of The Tonight Show. As stupid as this may sound today, this was actually a Really Big Deal in the '90's...one of those absurd pop culture stories which dominated the headlines and the tabloids for several years.

The movie itself was decent, with some interesting casting including Kathy Bates and Treat Williams, but nothing special. The main problem is that the audience is expected to root and feel sympathy for a couple of dudes who were already rich & famous and who would both continue to be rich & famous no matter how the story played out. The stakes weren't exactly the fate of the world, is what I'm saying.

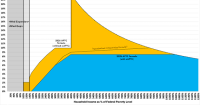

9/29/25: Welcome Paul Krugman subscribers! I greatly appreciate the shoutout by him but should add the following clarification:

Regarding the chart below which he reposted comparing the original ACA subsidy scale to the current version: You probably think that if the enhanced subsidies expire it will revert back to the original version, which would be bad enough. In fact, however, the Trump Regime has also made THAT version even worse, like so:

Ever since the MAGA Murder Bill (officially H.R. 1, the so-called "One Big Beautiful Bill Act") was passed by Republicans in the U.S. Senate & House and signed into law by Donald Trump a few days ago, I've seen a growing conventional wisdom taking hold on social media: People keep claiming that either all, "nearly all" or at least "most of" the budget cuts & other gutting of various programs and departments won't actually kick in until after the November 2026 midterms.

Now, don't get me wrong--most of those making these claims are well-intentioned; they're saying this cynically, to underscore how disingenuous Congressional Republicans are by back-loading the pain until the midterms are safely in their rearview mirrors. And, to be fair, much of the damage won't being until well after next November.

Over at The New Republic, Greg Sargent has taken this thinking one step further, noting that by delaying so much of the ugliness of the new law until 2027 or beyond...

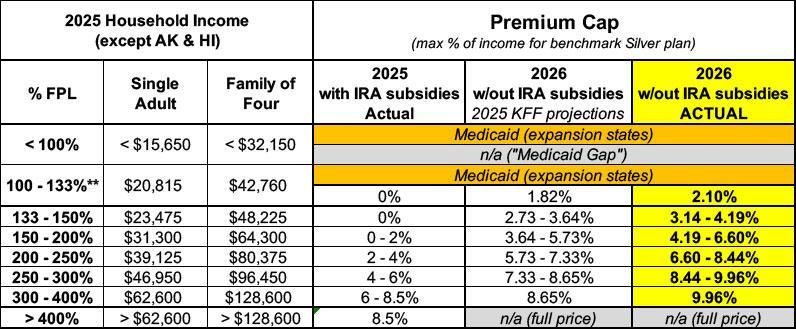

As anyone not under a rock for the past few months knows by now, the improved federal Affordable Care Act tax credits which were put into place by President Biden and Congressional Democrats starting in 2021 are currently scheduled to expire at the end of December, just 2 1/2 months from now.

On top of this, the Trump Regime has also made administrative regulatory changes to how the ACA is structured resulting in the remaining tax credit formula becoming even less generous yet, while also eliminating eligibility for either financial assistance or even ACA enrollment whatsoever to many other Americans.

(Unfortunately, no rate justification summary is available, and the full actuarial memo is heavily redacted. Policy enrollees are estimated based on marketwide estimated enrollment; see below.)

Banner/Aetna CVS:

(Dropping out of the individual market for 2026.)

I am writing to notify the Department that Banner Health and Aetna Health Plan Inc. (“Banner | Aetna”) will exit the individual health insurance market effective December 31, 2025. This notification is sent pursuant to Department guidance and Arizona statute 20-1380(D)(1). We made this decision after careful consideration and after evaluating the evolution of business at Banner | Aetna. The details of our individual market exit include the following:

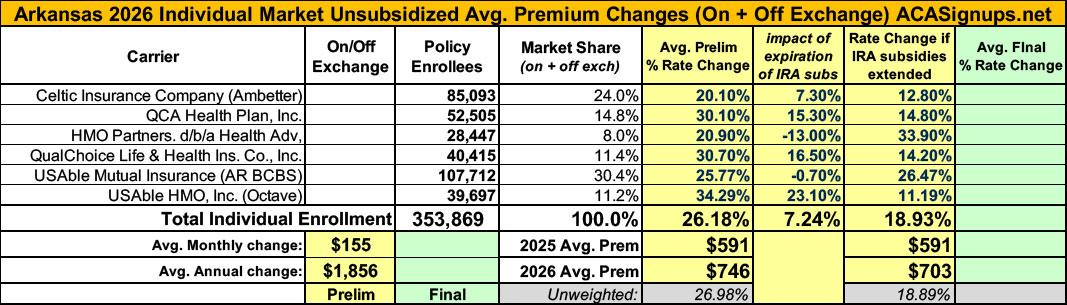

I still have the preliminary 2026 rate filings to analyze for about 10 more states, but I'm taking a break to go back and revisit ARKANSAS.

Back on July 18th, I posted my original analysis of ACA-compliant individual & small group market filings for Arkansas insurance carriers. At the time, I found that the weighted average increases being requested for individual market policies averaged a disturbingly high 26.2%. Here's what the breakout looked like:

Arkansas has around 166,000 residents enrolled in ACA exchange plans, 92% of whom are currently subsidized. I estimate they also have perhaps another ~11,000 unsubsidized off-exchange enrollees.

For many years, the District of Columbia has had among the most generous Medicaid income eligibility thresholds in the country, with children and pregnant women in households earning up to 324% of the Federal Poverty Level (FPL) being eligible as well as parents earning up to 216% FPL and childless adults earning up to 210% FPL*. As a result, nearly 37% of DC's total population is enrolled in Medicaid.

Oregonians continue to have at least five health insurance companies to choose from in every Oregon county as companies file 2026 health insurance rate requests for individual and small group markets

In-depth rate review process just beginning, opportunities for public review and input remain through June 20

June 2, 2025

Oregon health insurers have submitted proposed 2026 rates for individual and small group plans, launching a months-long review process that includes public input and meetings.

Five insurers will again offer plans statewide (Moda, Bridgespan, PacificSource, Providence, and Regence), and Kaiser is offering insurance in 11 counties, giving six options to choose from in various areas around the state.