Just as I'm wrapping up calculating the weighted average rate hikes requested in all 50 states, New York just became the second state (after Oregon) to release their approved rates:

As of 2014, South Carolina's total individual market was roughly 201,000 people, including grandfathered & transitional enrollees. 205,000 people were enrolled in exchange policies as of the end of March 2016; when you add off-exchange enrollees, it's likely closer to 250K, of which I'd imagine 225K or so are ACA-compliant. The enrollment numbers below therefore should reflect roughly 70% of the ACA-compliant market.

To calculate the Blue Cross Blue Shield average percentage, I had to do a bit of guesswork as to the proportion of their 116,000 enrollees between the 3 different types of plans (BlueEssentials, Multistate and Catastrophic). BlueEssentials is the highest of the three (14.74%), but also likely holds the vast majority (I'd guess 95% or more); usually very few people select Catastrophic plans, and I don't think many go for Multistate either. Therefore, I'm eyeballing the overall average at around 14.4%.

Golf Carts vs. Ford Fiestas: No, "healthcare policy" premiums did NOT go up 49% due to the ACA

Yesterday I posted an entry which noted a story published by Avik Roy over at Forbes about an extensive study by the Manhattan Institute which compared the average insurance policy premiums last year vs. the average premiums this year, after the first ACA open enrollment period. Roy's piece breathlessly claims "Obamacare Increased 2014 Individual-Market Premiums By Average Of 49%"

I wrote a response piece which also included the HHS report about ACA subsidies covering an average of 76% of the premium cost for the Federal marketplace, but I didn't really have time to do a full analysis of the Forbes piece. However, I did note 4 major points which lept out at me right off the bat:

Patients burst into tears at this city’s glistening new charity hospital when they learned they could get Medicaid health insurance.

In Baton Rouge, state officials had to bring in extra workers to process the flood of applications for coverage.

And at the call center for one of Louisiana’s private Medicaid plans, operators recorded their busiest day on record.

The outpouring began in June, when Louisiana became the 31st state to offer expanded Medicaid coverage through the Affordable Care Act, effectively guaranteeing health insurance to its residents for the first time.

Now, as Republican presidential nominee Donald Trump promises to repeal the healthcare law, Louisiana is emerging as a powerful illustration of the huge pent-up demand for health insurance, particularly in red states where elected officials have fought the 2010 law.

Supreme Court grants emergency order to block transgender male student in Virginia from using boys' restroom

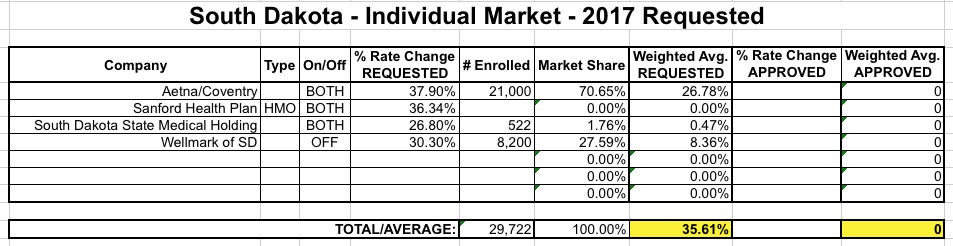

Last month I noted that while South Dakota hadn't posted their ACA-compliant 2017 rate filings yet, they had posted their grandfathered/transitional filings, and decided to take a look at those. While GF/TR plans are down to a pretty nominal number in most states (and about half the states don't have any transitionals at all at this point), SD still has a huge portion of their individual market enrolled in them (over 1/3, from what I can tell).

Only 4 carriers appear to be participating in the ACA-compliant individual market in South Dakota next year: Aetna, Sanfrod, SD State Medical and Welmark. I only have the enrollment numbers for 3 of the 4, but the requested rate hike for the fourth one (Sanford) is pretty close to the average of the other three anyway, so it shouldn't really impact the overall average by much:

As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

Wisconsin's total individual market was around 260,000 people in 2014 and is likely up to around 300,000 today (not including grandfathered/transitional enrollees), with about 224,000 enrolled on ACA exchange policies as of March 2016, plus an unknown number off-exchange. That means that the table below is likely missing around 1/3 of the total ACA-compliant market.

As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

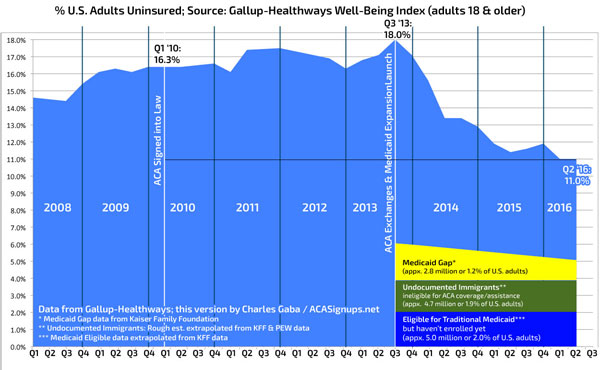

I've written a number of times about the irritating tendency of media outlets (and even the original data source itself) posting graphs & charts which are presented in highly misleading ways...even if the data itself supports the larger headline. The usual target of my ire is Gallup itself, which keeps presenting their quarterly Uninsured Rate graphs like so:

By cutting off the first 10 percentage points, this makes the uninsured rate drop since the ACA was implemented seem far more impressive than it already is. I support the ACA, but still prefer the situation be presented as accurately as possible. As a result, I keep reformatting Gallup's data like so (I also add some additional data points for further context):

I'm bringing this up again today because Greg Dworkin took note of the opposite problem yesterday (h/t to Richard Mayhew for calling his tweet to my attention):

As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

As I noted Monday morning, I believe that August 1st was the deadline for every state to submit their 2017 rate filings, meaning that the 14 states missing from my Requested Rate Hike Project are finally available to be plugged into the spreadsheet. I'll also be going back through the other states I've been tracking since as early as April to see which ones require updates due to carriers dropping out, joining in or resubmitting their rate requests.

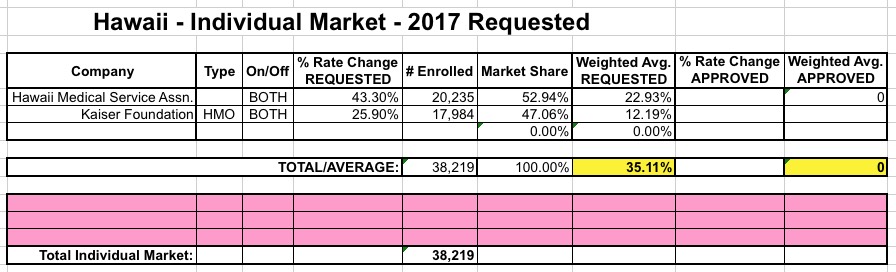

There are only two insurance carriers participating in Hawaii's individual market next year: The Hawaii Medical Service Association (HMSA) and the Kaiser Foundation Health Plan.