Health Insurer Aetna Inc on Wednesday said it plans to continue its Obamacare health insurance business next year in the 15 states where it now participates, and may expand to a few additional states.

"We have submitted rates in all 15 states where we are participating and have no plans at this point to withdraw from any of them," said company spokesman Walt Cherniak. But he noted that a final determination would hinge on binding agreements being signed with the states in September.

Aetna sells the individual coverage on exchanges created by the Affordable Care Act, also called Obamacare. By also filing proposed rates in several other states, Aetna said it had preserved its options to participate in them as well next year. It declined to identify the potential new markets.

The 15 states where it currently participates are Arizona, Delaware, Florida, Georgia, Illinois, Iowa, Kentucky, Missouri, Nebraska, North Carolina, Ohio, Pennsylvania, South Carolina, Texas and Virginia.

Now that the official ASPE Q1 2016 Effectuated Enrollment report is out, I can compare various state exchange reports against that to see how they're doing. In Washington State, 158,245 people were reported as being enrolled in active, effectuated exchange policies as of 3/31/16.

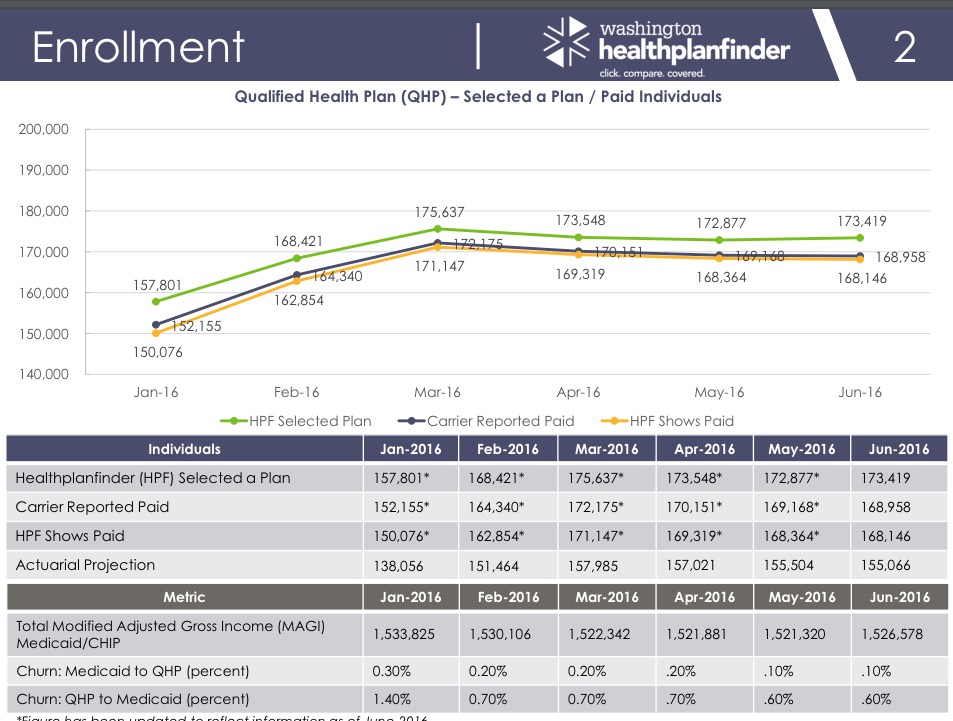

The WA HealthplanFinder has issued their July dashboard report, and their off-season retention numbers look pretty good: 168,958 people had paid their monthly premiums as of June...a 6.8% increase over the March figure. Even if this is off slightly due to methodology differences, it's still a good thing to see exchange enrollment up from earlier in the year, since overall enrollment is down at least 12.6% since the end of open enrollment due to non-payments, legal issues and so on.

The Massachusetts Health Connector has posted their latest monthly enrollment report (through the end of July), and the news is good. As I note every month:

Unlike most states, the Massachusetts Health Connector has not only seen no net attrition since the end of Open Enrollment, but has actually seen a net increase in enrollment...mainly due to their unique "ConnectorCare" policies, which are fully Qualified Health Plans (QHPs) but have additional financial assistance for those who qualify and which are available year-round instead of being limited to the open enrollment period.

The amount of the increase depends on which "official" number you start with; the MA exchange claimed 196,554 people as of 1/31/16...while the ASPE report gives it as 213,883 as of the next day....yet their March report claims 208,000 effectuated enrollees as of February.

As I keep noting, the DC exchange insists on presenting their enrollment numbers as cumulative since October2013.

As a result, I have to subtract the prior numbers from the current ones to find out the net increase in QHP selections, Medicaid enrollments and SHOP enrollments.

As I've been noting for a few months now, Connect for Health Colorado's monthly enrollment reports are chock full of data and confusing as hell at the same time.

As a result, I've started simply presenting them without much commentary. Here's the July report:

I don't write about Idaho much, which is a bit surprising when you think about it because it's kind of a unique state when it comes to the ACA exchanges. Most states never set up their own exchange platform. A dozen or so set them up and are still using them. Two states (Massachusetts and Maryland) scrapped their original, failed platforms and completely overhauled them.

Three states started out with their own platform but gave up when they failed, moving home to the mothership (HealthCare.Gov). One state, New Mexico, was supposed to move off of HC.gov after the first couple of years, but changed their mind and is still hosted by the federal platform. Oh, and there's also Kentucky, which is scheduled to scrap their perfectly-functioning tech platform for absolutely no good reason other than the petty whim of their new Governor, Matt Bevin.

And then there's Idaho.

Idaho is unique for a couple of reasons: Not only is it the only state to start off hosted by HC.gov and then move off of the federal tech platform onto it's own system, it's also the only state running it's own full exchange which hasn't expanded Medicaid as well.

UPDATE 10/27/16: See below for FINAL update (for real!)

UPDATE 10/19/16: As you can see, I've locked in the approved weighted average rate hikes for 40 states plus DC, leaving 10 states to go. I do plan on filling in the remaining approved rate hikes as the data for those 10 states comes in, but at this point it's quite clear that 25% is the magic number. The weighted average has been hovering between the 23-26% range since the first few approvals started being publicized in mid-August, and has stabilized in the 24-25% range for the past month. Over 77% of the total U.S. population is represented by these 40 states (+DC); unless there's some dramatic final rate changes in the remaining 10 states, that national 25% average isn't likely to budge by more than a rounding error.

As proof of this, I assumed that the requested rate hikes are approved exactly as is for all 10 states.

Result? The national, weighted average rate hikes went from 25.25%...to 25.36%.

OK, make that four states in which at least one major carrier has submitted an updated rate filing request since I originally estimated the statewide average.

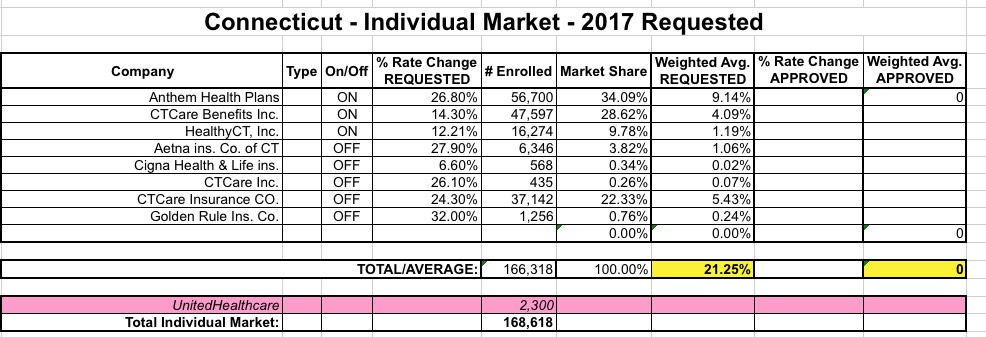

Shortly after that, however, HealthyCT became the latest ACA-created Co-Op to fail, meaning their 16,000 or so current enrollees will have to shop around for new coverage next year. I revised the numbers accordingly and the average request bumped up a bit to 22.2%...

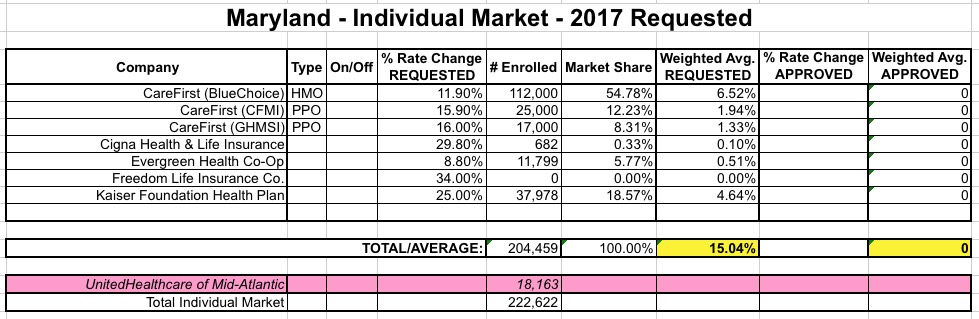

BALTIMORE – Commissioner Al Redmer, Jr. will be conducting a second public hearing on Monday, August 15th from 11 am – 1 pm at the Maryland Insurance Administration located at 200 St. Paul Place, 24th floor Hearing Room, Baltimore, MD 21202 to receive public input on a revised filing made by CareFirst. On July 26, CareFirst refiled its 2017 proposed rates for the individual market and requested a 27.8% rate increase for HMO plans and a 36.6% rate increase for PPO plans. CareFirst previously requested a 12.0% and 15.3% rate increase, respectively.

I noted back in February that Vermont Health Connect, VT's ACA exchange, has remained essentially silent since last fall, issuing only 2 press releases since Open Enrollment started last November (one of which was about a new plan comparison tool, the other of which was about some sort of Medicaid-related dealine). In other words, they haven't publicized their 2016 enrollment numbers whatsoever...the only reason I have data for VT at all is thanks to the official ASPE reports from the HHS Dept. This is a stunning 180º turnaround from 2015, when they were issuing detailed reports on a regular basis.