Anyone who's followed me either here at ACASignups.net or over at Twitter over the past eight months knows that no one has been sounding the alarm louder or more frequently than me about both the real and potential sabotage of the ACA being carried out (or at least attempted) by the GOP in general and Donald Trump/Tom Price specifically. Hell, back in July, I even warned of a half-dozen things to look out for, several of which have since already been proven true:

This brings me to the main point of this entry: This is likely just the beginning. I'm not going to say that any or all of the following will happen--it's possible that Trump/Price/Verma will show some level of restraint--but I wouldn't be at all surprised to see any or all of these happen during this fall's Open Enrollment Period (which runs from Nov. 1st - Dec. 15th, by the way):

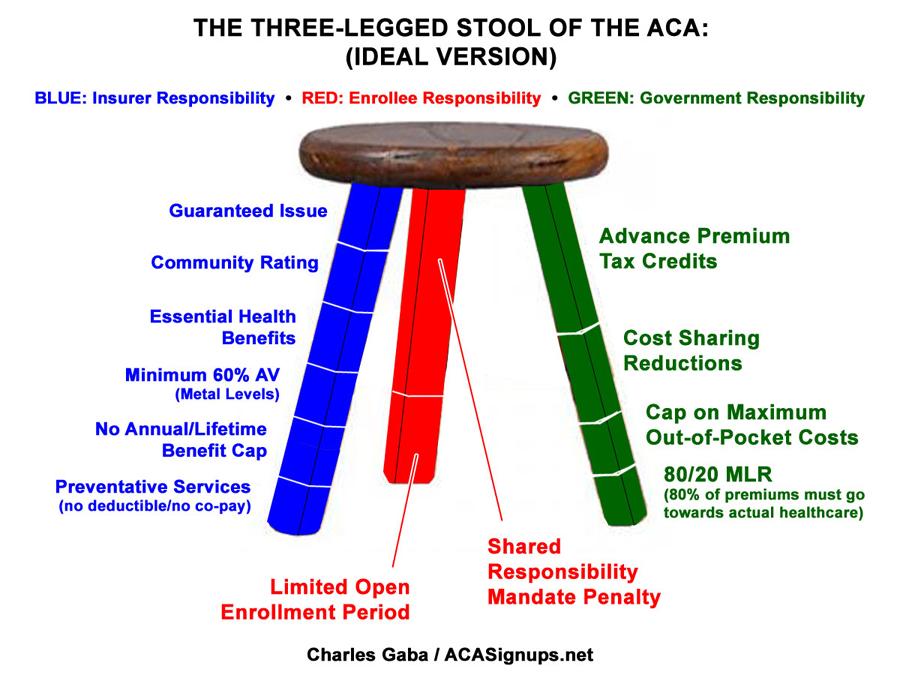

It's time to once again dust off the Three-Legged Stool visual aid to help explain just what the Graham-Cassidy bill would do to the individual insurance market. It's important to note that none of this has anything to do with Medicaid (expansion or traditional), the group market, Medicare and so forth; just the individual market.

Once again, here's what the "3-Legged Stool" was supposed to look like under the Affordable Care Act:

Here's what it actually looks like today, with some rather obvious gaps in the red (enrollee responsibility) and green (government responsibility) legs:

As the final deadline for final 2018 individual market rates to be locked in and the contracts signed, more states are coming into focus, and the pattern continues to be remarkably consistent.

In Mississippi, I originally pegged the requested rate hikes across the two individual market carriers (technically three, but "Freedom Life" is a phantom carrier with only 2 alleged enrollees) at 16.1% if CSR payments are made and 39.6% if they aren't. It turns out I was off by a bit, however, because I didn't realize that BCBS of Mississippi was only selling policies off-exchange next year. That means the CSR issue won't impact them either way, since none of their enrollees would receive the assistance anyway.

Alaska (along with Hawaii) will continue to receive Obamacare’s premium tax credits while they are repealed for all other states. It appears this exemption will not affect Alaska receiving its state allotment under the new block grant in addition to the premium tax credits.

Delays implementation of the Medicaid per capita caps for Alaska and Hawaii for years in which the policy would reduce their funding below what they would have received in 2020 plus CPI-M [Consumer Price Index for Medical Care].

Provides for an increased federal Medicaid matching rate (FMAP) for both Alaska and Hawaii."

Well, now.

Bird doesn't have the actual legislative text, but they threw Hawaii in there as well (not to win their votes...Dems Brian Schatz and Mazie Hirono are solid NOs no matter what). That means that the wording is probably along the lines of:

The Congressional Budget Office stated that they won't be able to provide a full score of the projected 10-year impact of the Graham-Cassidy bill for "at least several weeks". Instead, they expect to provide a partial score, focusing purely on the budget-related stuff necessary to "count" towards Senate reconciliation voting rules "early next week".

What won't be included are some pretty damned important details, like:

Impact on the federal deficit

Impact on insurance premiums, and of course...

Impact on the number of people with health insurance coverage

Unfortunately, Mitch McConnell and Senate Republicans are insisting on squeezing the vote on Graham-Cassidy through within the next 10 days, before the fiscal year ends on Sept. 30th, since that's the only way they have a chance at passing it using 50 votes (after the 30th, they would require 60 votes, which of course they have no chance at getting).

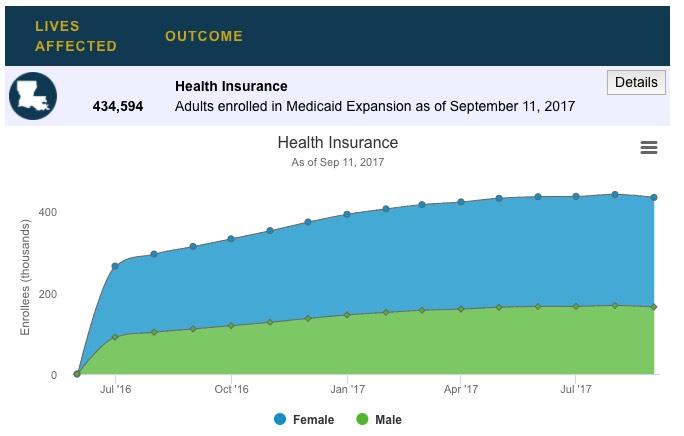

I've embedded screen shots below, but there's various interactive stuff you can do at the site itself; LA did a very nice job, I'd love it if every state put up a similar "dashboard" style website.

In short:

434,594 Louisianans enrolled in Medicaid via ACA expansion

126,229 have received preventative care

22,058 women have received breast cancer screenings

225 women have been diagnosed with breast cancer as a result of ACA Medicaid expansion

13,994 adults have received a colon cancer screening

4,337 have averted colon cancer by having polyps removed

199 have been diagnosed with colon cancer thanks to ACA Medicaid expansion

3,774 have been diagnosed with diabetes

9,575 have been diagnosed with hypertension

32,912 are receiving outpatient mental health services

6,025 are receiving inpatient mental health services

5,559 are receiving outpatient substance abuse services

6,026 are receiving residential substance abuse services

As NBC News reporter Hallie Jackson notes, there are too many quotable lines to count in this Vox piece, in which Jeff Stein tracked down 9 Republican Senators to ask them what the hell the purpose of the Graham-Cassidy bill actually is. The responses pretty much say it all.

Jeff Stein: Senator, I wanted to ask you for a policy-based explanation for why you’re moving forward with the Graham-Cassidy proposal. What problems will this solve in the health care system?

Pat Roberts: That — that is the last stage out of Dodge City...I’m from Dodge City. So it’s the last stage out to do anything. Restoring decision-making back to the states is always a good idea, but this is not the best possible bill — this is the best bill possible under the circumstances.

If we do nothing, I think it has a tremendous impact on the 2018 elections. And whether or not Republicans still maintain control and we have the gavel.

Jeff Stein: But why does this bill make things better for Americans? How does it help?

The fact that the Graham-Cassidy bill, like all of the prior Republican "replacement" healthcare bills, screws over people on both Medicaid and the individual market starting in 2020 is hardly news. A few provisions of the ACA are stripped out and/or bastardized immediately (and some, like the individual mandate penalty, are even repealed retroactively), but for the most part the pain doesn't start for another 2 years, well after the midterms are over.

However, JP Massar called something to my attention this morning:

Regular readers know that one of the issues I've spent the better part of the past year yammering on about endlessly is the importance of Congress formally appropriating Cost Sharing Reduction reimbursement payments to the insurance carriers on the individual market exchanges.

Thanks to the ongoing/pending ruling in the federal House vs. Burwell Price lawsuit, Donald Trump has the ability to pull the plug on CSR payments pretty much whenever he wants to (and he's threatened to cut them off every month since around March or April so far). CSR payments hang like a Sword of Damocles over the heads of every exchange-based insurance carrier each month, with them never knowing whether they'll get reimbursed or not.