Back in early June, the New York Dept. of Financial Services posted the requested 2018 rate hikes for the individual and small group markets. In most states, the CSR reimbursement issue is a much bigger factor than whether or not the Trump Administration enforces the individual mandate, but in New York it's the exact opposite: According to the NY DFS, loss of CSR payments would only tack on 1.3 points to the total, while "a full repeal of the federal individual mandate would increase rates by an additional 32.6%".

The reason for the fairly nominal CSR factor is that the vast majority of NY's CSR-eligible population (those earning 138-200% FPL) is instead enrolled in the state's Basic Health Program. As a result, only 26% of New York's exchange enrollees receive CSR assistance, and the 200-250% FPL recipients only receive a fairly skimpy amount of CSR help anyway. At the opposite end of the spectrum, the 32-point mandate factor is far higher than most carriers are indicating (more like 4-5 points), but there's a big difference between the administration "not enforcing" the penalty and outright repealing it, which NY DFS is talking about.

In any event, this means that NY's requested average increases boiled down to: 15.0% if CSRs are paid/mandate enforced, 16.6% if CSRs aren't paid/mandate is enforced, or a whopping 50.5% if CSRs aren't paid and the mandate was repealed.

As I noted earlier today, there’s a gazillion ways the Trump Administration could sabotage (and in some cases, is already sabotaging) the 2018 Open Enrollment period this fall, doing everything in their power to dampen, obstruct and otherwise minimize the number of people who actually enroll in a healthcare policy via the federal ACA exchanges.

However, as I've noted before (and as the CBO confirmed last week), due to the confusing, inside out way in which the APTC and CSR subsidy formulas happen to work, there's also the potential for one of the most pressing sabotage schemes by Trump and the GOP to backfire completely, leading to the potential for a significant increase in ACA exchange enrollment.

I've noted before that even if the Trump Administration does ensure CSR reimbursement payments and does enforce the individual mandate in 2018, there are literally dozens of other ways that Trump and HHS Secretary Tom Price could sabotage the 2018 Open Enrollment Period. Here's just a few, several of which they've already been caught doing:

Minimal or non-existent advertising/outreach/promotional efforts

Understaffing of call centers/support staff, leading to absurdly long hold times

Deliberately underthrottled server bandwidth, slowing HC.gov down or even taking it offline, especially during peak hours

"Accidentally" misentered enrollment instructions or policy specifications

Confusing or missing confirmation/status notification messages either on the site, via email or both

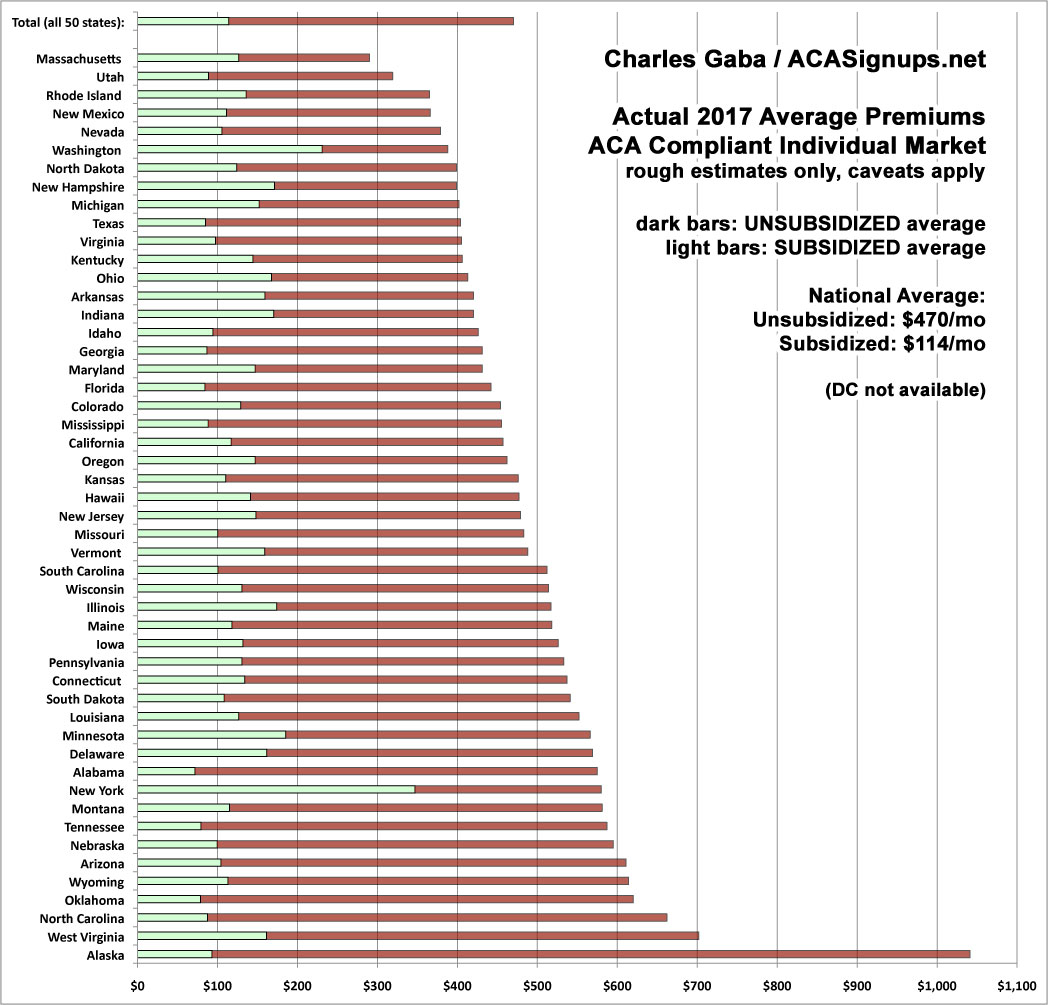

For all the fuss and bother about how much premiums are expected to go up on a percentage basis next year, using percentages can be misleading, since the lower the premium is to begin with, the more dramatic a percentage increase is going to seem relative to where it started.

With that in mind, I've decided to mush together two recent projects of mine: First, my debunking/correction of the May ASPE report which disingenuously claimed that individual market premiums had "increased by 105% since 2013 due to the ACA"; second, my 2018 Rate Hike Project.

As I noted when I debunked/corrected the ASPE report, not only did it turn out to be somewhat lower when all 50 states were included (84%, not 105%), but the ASPE report completely ignores both the financial assistance provided to roughly half the market and, just as importantly, blows off the apples to oranges mismatch between the numbers, because only a handful of states had guaranteed issue laws in 2013, and only one (NY) had a community rating law. Having said that, as long as you keep those caveats in mind, the (corrected) ASPE report does provide a good baseline for figuring out what the 2018 premiums are likely to be.

By merging the spreadsheets for these projects together, I've come up with a rough idea of what I expect to see in terms of unsubsidized, full-price premiums for individual ACA policies this November. I'm using a median instead of a weighted average this time around because I expect high variables in terms of the number of people who enroll in each state compared to 2017 (unfortunately, I still don't have 2018 data for several states, and I don't have the 2017 dollar average for DC to compare against).

I've ordered the states from lowest to highest based on the assumption that CSR reimbursements aren't made next year ("full sabotage effect"). The blue sections are my best estimates for each state assuming CSRs are paid; the yellow sections represent how much of the average premiums are due to "CSR padding" by the carriers.

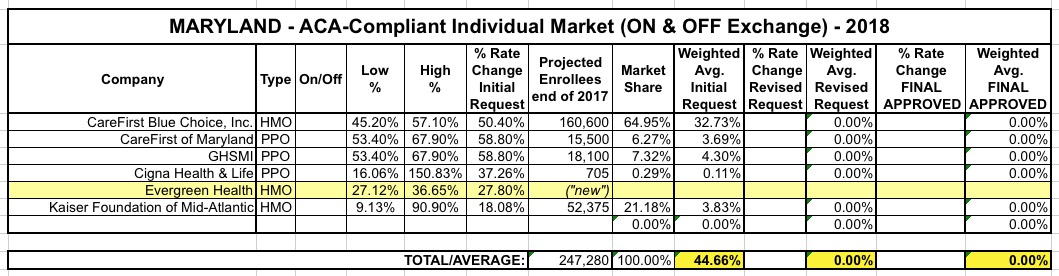

As noted in the Virginia and Maryland updates, I've started going through the earlier state rate filings and revising them to include:

Updated/revised carrier rate filings;

Additional market withdrawls and/or expansions;

Corrections to CSR factor impact, etc.

The original versions of each state writeup includes screen shots of the actual filing documents and explainers behind specific requests; I don't have time for that with most of the updates, so I'm bundling several states together. Here's Connecticut, Oregon and Vermont's revisions:

As noted the other day, now that I've compiled the initial 2018 rate filing requests for 46 states + DC (the remaining 4 states aren't public yet), it's time to go back to the earlier states I analyzed and see whether there's been any updates/corrections to my original estimates. I started running the numbers back in early May, and a lot has changed since then, with carriers dropping out of the exchanges, expanding to fill the gaps or simply refiling with revised pricing requests.

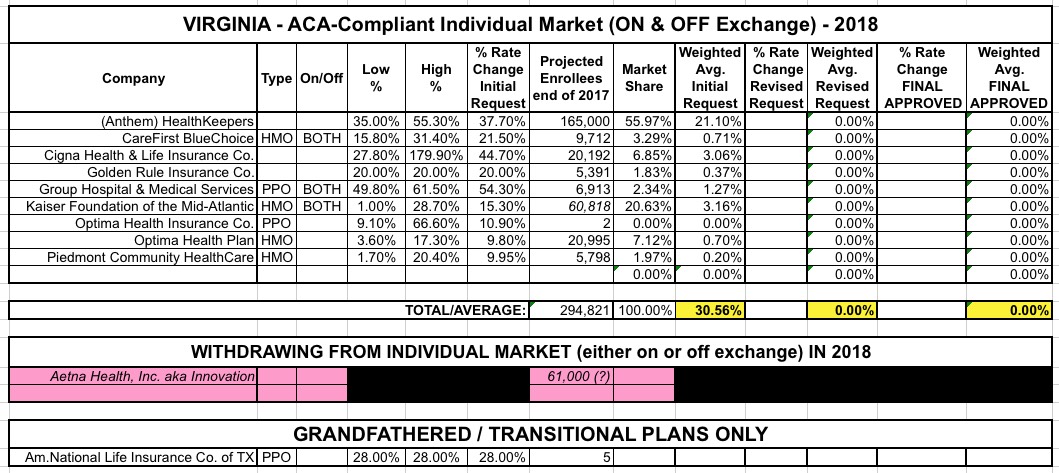

For the past two years, Virginia has been the first state in the nation to post their initial rate filings for the following year. I originally compiled their individual market 2018 change requests back in early May, and came up with the following at the time:

UnitedHealthcare had previously announced they were dropping out of Virginia, but I didn't have an enrollee number for them, and Aetna had also just announced their withdrawl from the state. I hadn't yet finalized my "CSR/Mandate Penalty" factor layout yet; at the time I assumed the 30.6% weighted average requested assumed full CSR/mandate sabotage and reduced that number by 17 points based on the Kaiser Family Foundation's "19% national average CSR rate hike" estimate analysis, which estimated the CSR impact at 17 points for Virginia.

I've completed this process for 46 states + DC. I've confirmed (well, really, Louise Norris confirmed for me) that the filing data for the four missing states--Kansas, Missouri, Nevada and Utah--won't be made available publicly for another couple of weeks, which is irritating...but those four states combined only make up about 5% of the total population anyway; unless their average rate increase requests are significantly higher (or lower) than the average of the rest of the states, they aren't gonna move the needle up or down by more than a tenth of a point or so.

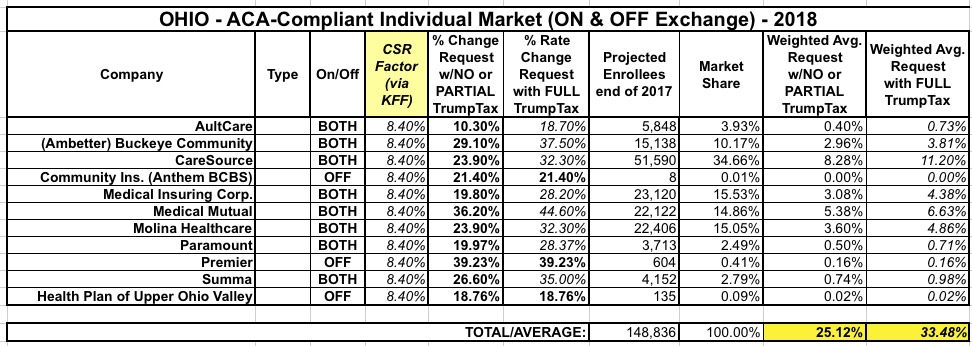

Like Wisconsin and Michigan, Ohio has a high number of carriers statewide...although the per-county competition is still lacking in some areas. Even so, their rate hike requests are still pretty high even with CSR payments being made...and dramatically higher if they aren't.

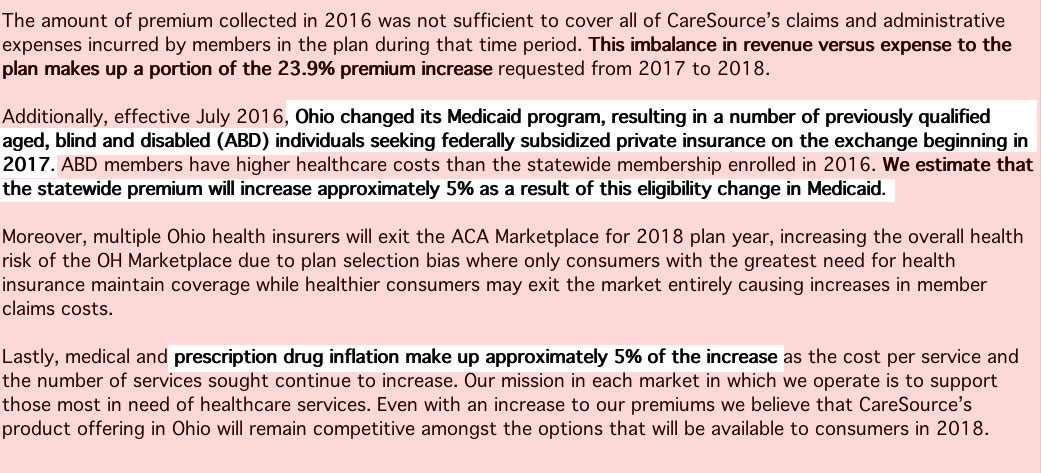

One interesting tidbit: Check out the CareSource filing letter (first one below the table). They don't mention CSRs or mandate enforcement...but they do specify that a full 5 points of their 23.9% increase request is tied to prescription drug inflation (see Shkreli, Martin)...and even more noteworthy, they say that another 5 points is due specifically to "a number of previously [Medicaid-] qualified individuals" being kicked over to the private exchange,

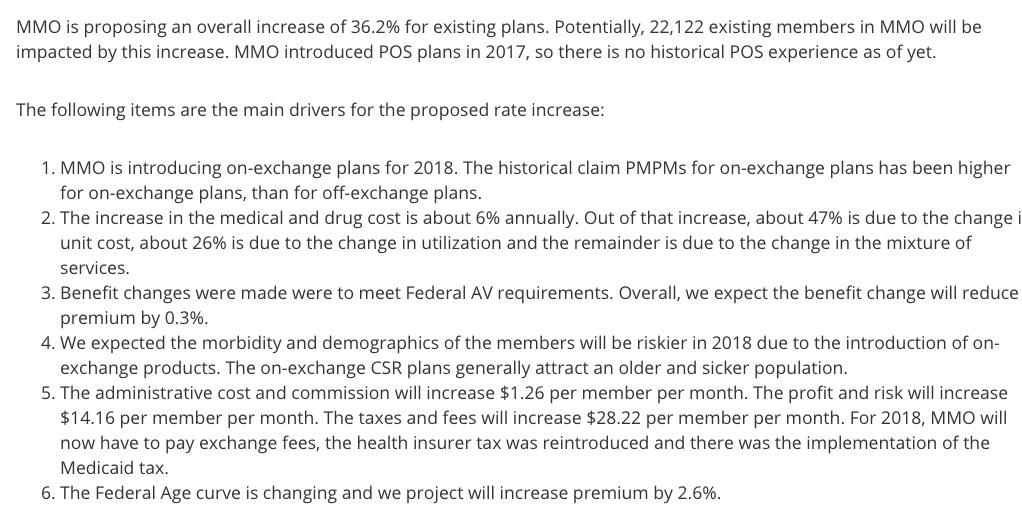

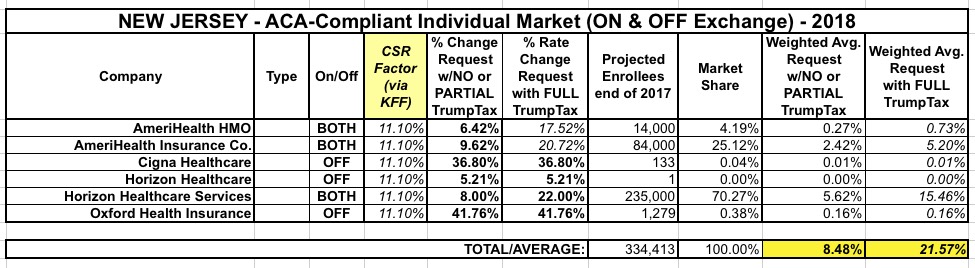

I had already posted a partial look at the New Jersey rate hike situation a couple of weeks ago with a video in which Topher Spiro of the Center for American Progress interviewed NJ Congressman Frank Pallone about the situation. Since his comments weren't official and only referred to Horizon Blue Cross, I didn't make it an official part of the Rate Hike spreadsheet, but now I've managed to plug in the remaining carriers and here's how it looks. As expected, with Horizon holding a commanding 70% market share, the statewide average is around 8.5% if CSR payments are made and the mandate is enforced versus 21.6% if CSR payments aren't made and the mandate isn't enforced.

Also, check out Horizon's cover letter explaining the rate hike...they're not screwing around with who to pin the blame on.

{kind=link}