But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

At long last, I've completed my analysis of the preliminary 2020 rate filings for ACA-compliant individual market policies across all 50 states (+DC)! in most cases I've also included the small group market, although with far less documentation for those.

Texas, understandably enough, has the third largest individual market in the country after California and Florida, at somewhere around 1.27 million enrollees (they had around 990,000 on-exchange enrollees; I'm pretty sure around 75% of the market is on-exchange these days).

There's ten carriers offering ACA policies on the individual market in Texas, and fifteen participating in the small group market. Unfortunately, most of the rate filings are redacted or missing data altogether (again), so I was only able to cobble together hard enrollment data for half the Indy market carriers, comprising just 15% of the statewide market. I've run an unweighted average for the other five carriers, and blended that with the first five for a semi-weighted average rate hike of just 0.8% overall.

I know this is an imperfect way of doing it, but it's the best I can do at the moment. I hope to have more complete data once the approved filings are made available.

As I noted a few days ago, now that the 2019 ACA Open Enrollment Period is actually underway and the approved individual market premium rate changes have been posted publicly for every state, I'm finally able to go back and wrap up my 2019 Rate Hike Project for the nine states which I was still missing final numbers for.

As I further noted, the approved rates in most of those states didn't change much compared to the preliminary/requested rate changes I had already analyzed earlier this year:

Maryland files suit to protect health reform from Texas.

... the Maryland attorney general today filed a separate lawsuit in a Maryland district court. Among other things, he’s seeking an injunction requiring the continued enforcement of the law. Depending on how quickly the Maryland case moves, it’s possible we could see dueling injunctions—one ordering the Trump administration to stop enforcing the law, the other ordering it to keep enforcing.

That’s an unholy mess just waiting to happen. Now, it may not come to that. My best guess is that the Texas lawsuit will fizzle: any injunction will likely be stayed pending appeal, either by the Fifth Circuit or the Supreme Court, and the case is going nowhere on the merits. The Maryland lawsuit will likely prove unnecessary.

I don't have much to add to this other than to note how much this case underscores just how much power and importance state attorneys general have.

Normally at this point in the year I only do full rate hike write-ups for states when their approved rate changes are made public by insurance regulators. I'm making an exception for Texas, however, because my preliminary analysis of the statewide average premium changes back in June was missing a huge portion of the market--I only had around half the ACA individual market accounted for, and I repeatedly warned that the missing enrollment and rate change data could easily skew the statewide average higher or lower.

Well, it's early September now, and not only do I have access to pretty much all of the missing data now, some of the rate filings have changed significantly as well. At the time, I estimated Texas carriers as requesting average rate increases of just 1.5% overall, with them dropping around 10.6% if not for the ACA's individual mandate being repealed and Trump's expansion of #ShortAssPlans.

Unfortunately, while the SERFF database shows 2019 listings for most of the 11 carriers which offer ACA policies in Texas this year, it only actually has the filings posted for 3 of them so far: CHRISTUS, Sendero and FirstCare Health Plans (aka SHA, LLC). Even then, those three carriers hold a pretty small share of the market, totalling just 65,000 enrollees. That means I only have actual 2019 rate data for about 5% of the ACA market available so far.

Now that it appears that the full list of states and counties eligible for hurricane (or windstorm, in the case of Maine) Special Enrollment Periods (SEP) has settled down, Huffington Post reporter Jonathan Cohn asked an interesting question:

How if at all do you allow for the extensions in FL, TX, etc.? Or, to put another way, how many post-Dec 15 signups through https://t.co/bhGNSognZK do you expect?

The closest parallel to this particular situation I can think of was the #ACATaxTime SEP back in spring 2015. In that case, it was the first year that the ACA's (defunct as of this morning) Individual Mandate was being enforced, and a lot of people either never got the message about being required to #GetCovered or at least pretended that they didn't.

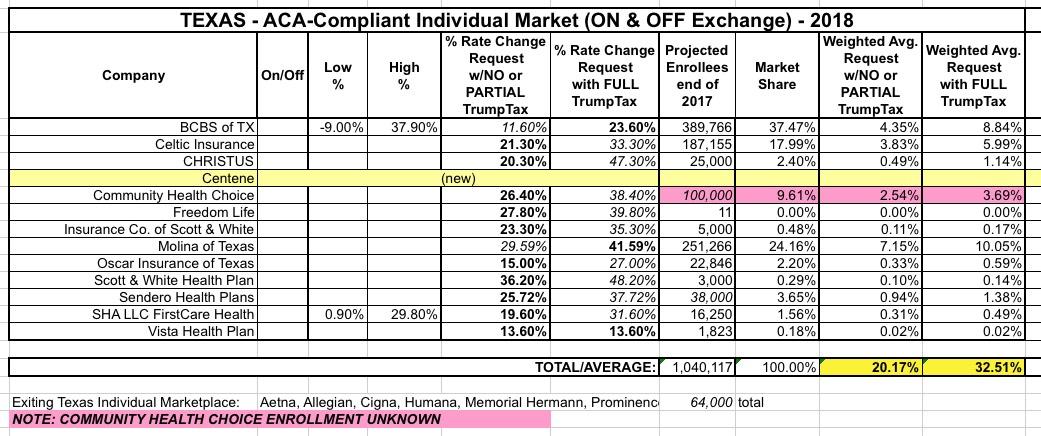

I've saved Texas for last because, frankly, I haven't been able to make heads or tails out of their actual average rate increases for next year (and unlike smaller states which might not move the needle on the national average anyway, Texas has one of the largest populations in the country, so a substantial error here can also impact the national numbers significantly).

Back in early August, I pieced together a rough average of the requested rate increases for the Lone Star State of around 20% if CSR payments are made or 32.5% if they aren't:

CMS Announces Special Enrollment Periods for Americans Impacted by Recent Hurricanes Agency provides special open enrollment periods for 2017 Medicare and Exchange coverage

As a result of Hurricanes Harvey, Irma, and Maria, the Centers for Medicare & Medicaid Services (CMS) will make available special enrollment periods for all Medicare beneficiaries and certain individuals seeking health plans offered through the Federal Health Insurance Exchange. This important step gives these individuals and families who have been impacted by the hurricanes the opportunity to change their Medicare health and prescription drug plans and gain access to health coverage on the Exchange immediately if eligible for a special enrollment period.

Health and Human Services Secretary Tom Price, MD, declared a public health emergency in Texas on Saturday as Hurricane Harvey was pounding the state's coast.

Harvey made landfall late Friday night with winds topping 130 mph. Forecasts called for the storm to hover over the state for 5 days or more, possibly drenching some areas with as much as 50 inches of rain. Hundreds of thousands were without power and the National Weather Service said parts of Texas could be "uninhabitable for weeks or months."

"Many Medicare beneficiaries have been evacuated to neighboring communities where receiving hospitals and nursing homes may have no health care records, information on current health status or even verification of the person's status as a Medicare beneficiary. Due to the emergency declaration and other actions taken by HHS, CMS is able to waive certain documentation requirements to help ensure facilities can deliver care," an HHS statement read.