(sigh) I'm into the home stretch with only a handful of states left to go. Unfortunately, South Carolina is yet another state where the actual enrollment numbers are either missing or redacted, making it impossible to run a properly weighted average...but again, the range between the three carriers offering individual market policies is so narrow that it doesn't make much difference anyway (between -3.72% and +0.17%).

The unweighted average is a 1.9% reduction in unsubsidized premiums statewide.

On the small group market, however, average 2020 premiums are jumping by double digits: 11.1%.

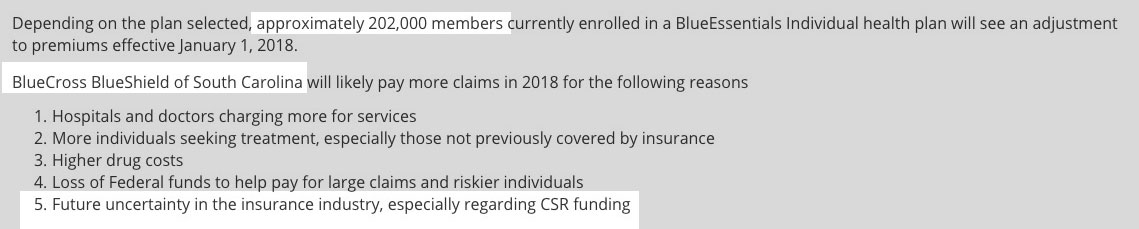

Back in August, Blue Cross Blue Shield of South Carolina, the only carrier offering policies on SC's individual insurance market, asked for a 9.2% average premium rate increase for 2019 statewide. This consisted of 9.3% for their most popular plans (which cover over 200,000 South Carolinans) and 6.9% for 6,800 BlueChoice plan enrollees (BlueChoice is only available off-exchange).

2019 PRELIMINARY HEALTH INSURANCE PLANS RATE CHANGES FOR INDIVIDUAL MARKET COVERAGE

The SCDOI has approved the rates and forms for health insurance issuers that are planning to offer ACAcompliant products in the individual market in 2019.

The only confusing thing about South Carolina's 2019 rate filings is that I'm not sure whether the "BlueChoice Health Plan" should be rolled in with the main Blue Cross Blue Shield of SC population. Carriers often have multiple listings in the same state for different policy lines, but they're generally listed under the same official corporate name. In this case, "BlueChoice" (which is clearly still part of BCBS) has a completely seaparate listing.

The BCBS filing clearly states the number of enrollees as around 203,000 people. The BlueChoice listing doesn't give a membership number, but appears to be roughly 6,800 people based on the full premium dollars they received in all of 2017 ($53.5 million divided by 12 months, divided by the statewide average of $654/month this year). This doesn't really make much difference, however, since BCBS still holds nearly 99% of the market anyway.

Assuming an 11.5% #ACASabotage factor (mandate repeal + shortassplans), this translates into unsubsidized enrollees having to pay an extra $900 than they'd otherwise have to (a 9.2% rate increase instead of a 2.3% rate drop).

Now that it appears that the full list of states and counties eligible for hurricane (or windstorm, in the case of Maine) Special Enrollment Periods (SEP) has settled down, Huffington Post reporter Jonathan Cohn asked an interesting question:

How if at all do you allow for the extensions in FL, TX, etc.? Or, to put another way, how many post-Dec 15 signups through https://t.co/bhGNSognZK do you expect?

The closest parallel to this particular situation I can think of was the #ACATaxTime SEP back in spring 2015. In that case, it was the first year that the ACA's (defunct as of this morning) Individual Mandate was being enforced, and a lot of people either never got the message about being required to #GetCovered or at least pretended that they didn't.

A couple of weeks ago, a joint letter was sent to all four Congressional leaders from AHIP (America's Health Insurance Plans), the BlueCross BlueShield Association, the American Academy of Family Physicians, the AMA, the American Hospital Association and the Federation of American Hospitalsm warning them, in no uncertain terms, of what the consequences of repealing the individual mandate would be:

We join together to urge Congress to maintain the individual mandate. There will be serious consequences if Congress simply repeals the mandate while leaving the insurance reforms in place: millions more will be uninsured or face higher premiums, challenging their ability to access the care they need. Let’s work together on solutions that deliver the access, care, and coverage that the American people deserve.

As the final deadline for final 2018 individual market rates to be locked in and the contracts signed, more states are coming into focus, and the pattern continues to be remarkably consistent.

In Mississippi, I originally pegged the requested rate hikes across the two individual market carriers (technically three, but "Freedom Life" is a phantom carrier with only 2 alleged enrollees) at 16.1% if CSR payments are made and 39.6% if they aren't. It turns out I was off by a bit, however, because I didn't realize that BCBS of Mississippi was only selling policies off-exchange next year. That means the CSR issue won't impact them either way, since none of their enrollees would receive the assistance anyway.

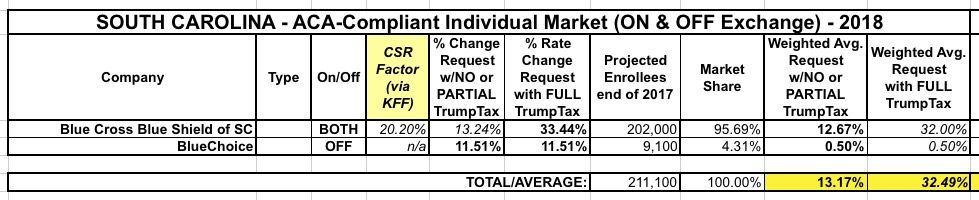

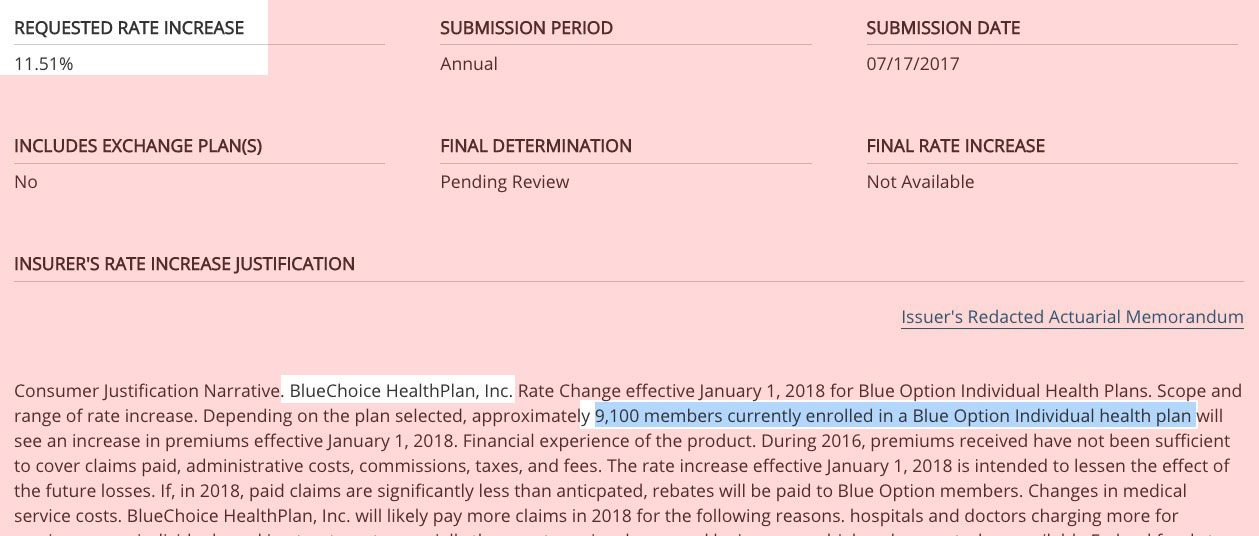

I admit to being a bit confused about the distinction between BCBSSC and BlueChoice HealthPlan, which is also a BCBS carrier...I'm guessing one is for HMOs, the other for PPOs or something. In any event, BlueChoice plans appear to only be available off-exchange, and are thus not subject to the CSR issue. BCBSSC is, however, and the Kaiser Family Foundation estimates that their Silver plans would have to go up 23% if CSR payments are cut off. 87%% of SC exchange enrollees are on Silver plans, so that should be roughly 20.2% across all policies.

If CSR payments are made, South Carolina is looking at around a 13.2% average rate hikes; if they aren't, it's an uglier 32.5%.

Over the past few months, my Congressional District Breakdown tables estimating how many people would likely lose healthcare coverage if the ACA were to be "cleanly" repealed (with no replacement) have gotten a lot of attention. This was followed by the Center for American Progress (CAP) running their own estimates of how many would likely lose coverage if, instead of a "clean" repeal of the ACA as a whole, the ACA were to be partially left in place, with the GOP's AHCA (Trumpcare) bill, which dramatically changes the ACA, being signed into law instead.

As I noted when I crunched the numbers for Texas, it's actually easier to figure out how many people would lose coverage if the ACA is repealed in non-expansion states because you can't rip away healthcare coverage from someone who you never provided it to in the first place.

As noted before, I'm really trying to move onto the actual enrollment part of the 2017 open enrollment period, but I can't resist doing some more final cleanup of my Rate Hike project:

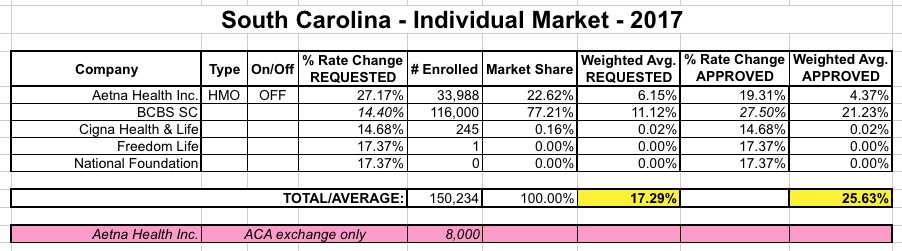

SOUTH CAROLINA: This is one of the 5 states which I still didn't have approved rate changes for. Today the RateReview.HC.gov site finally added in the final numbers for SC, so here's what it looks like:

Aetna was a bit tricky--the total enrollee number is actually 41,988. They dropped out of the ACA exchange but are sticking around the off-exchange market, so I had to figure out how many of those 42K are on vs. off-exchange. The answer is in this article which notes:

More than 220,000 South Carolinians rely on the federal health care law for insurance. This year, only 8,000 of them are covered by Aetna plans.