Today, the Centers for Medicare & Medicaid Services (CMS) announced that Tennessee and South Carolina can begin offering Medicaid and Children’s Health Insurance Program (CHIP) coverage for 12 months postpartum to an estimated 22,000 and 16,000 pregnant and postpartum individuals, respectively, through a new state plan opportunity made available by the American Rescue Plan.

Tennessee and South Carolina join Louisiana, Michigan, Virginia, New Jersey, and Illinois in extending Medicaid and CHIP coverage from 60 days to 12 months postpartum. CMS is also working with another nine states and the District of Columbia to extend postpartum coverage for 12 months after pregnancy, including California, Indiana, Kentucky, Maine, Minnesota, Oregon, New Mexico, Pennsylvania, and West Virginia. As a result of these efforts, as many as 720,000 pregnant and postpartum individuals across the United States could be guaranteed Medicaid and CHIP coverage for 12 months after pregnancy.

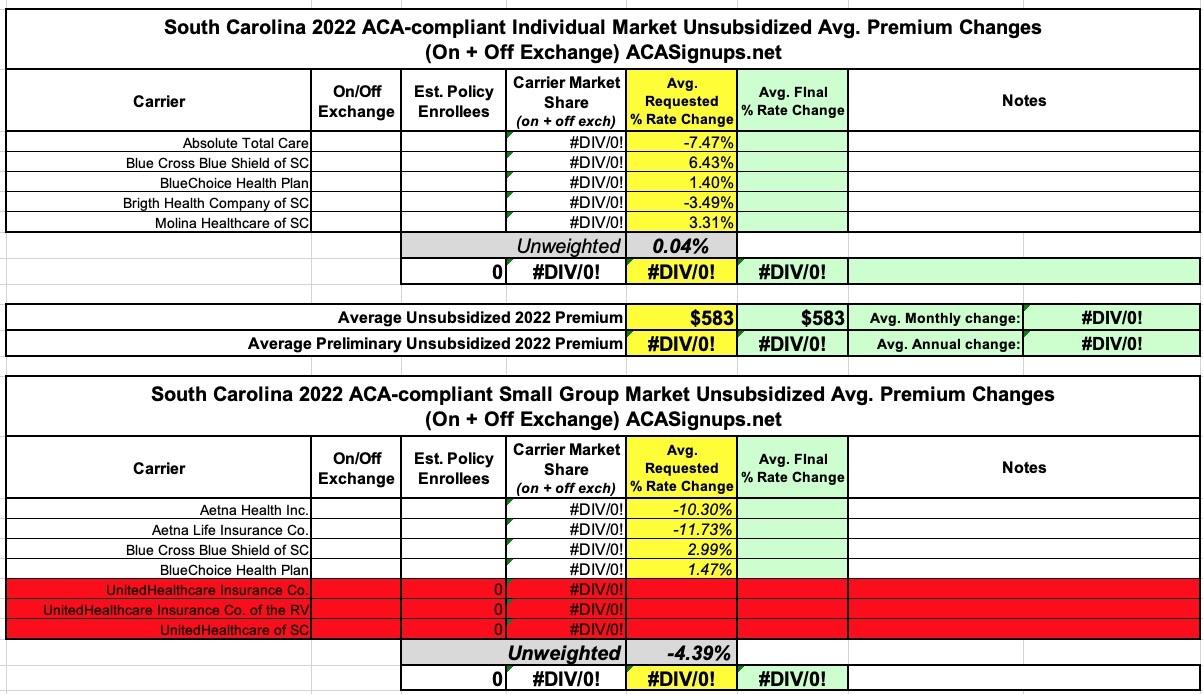

A week or so ago, I posted an analysis of the preliminary rate filings for South Carolina's 2022 individual & small group markets.

At the time, I wasn't able to find the actual filing forms and was thus limited to running unweighted averages for both markets, which came to a flat year over year increase in the individua market and a 4.4% reduction in small group plans.

Since then, however, I've managed to find the SERFF database filings for all carriers, and can now run weighted averages for approved rates in both markets.

Overall, they come in at a weighted average increase of 3.1% for the individual market and 2.1% for small group plans. It's also worth noting that I was wrong about UnitedHealthcare dropping out of the small group market--it looks like they're instead replacing all of their current policies with new ones, which means there's technically no actual "rate changes" since the existing offerings are being terminated and thus have nothing to compare against:

Unfortunately, the South Carolina Insurance Dept. website isn't particularly helpful when it comes to getting the annual rate filing data for these analyses--they post a link to the federal Rate Review website and the SERFF database, but that's it...and most of the filings don't show up in SERFF, while the Rate Review database actuarial memos are all heavily redacted.

As a result, all I have is the unweighted 2022 average rate changes, which are basically flat for the individual market and down around 4.4% for small group plans.

The other noteworthy item is that it looks like UnitedHealthcare is pulling completely out of South Carolina's ACA-compliant small group market, though it's possible that they just haven't been added to the federal Rate Review database yet.

I've once again relaunched my project from last fall to track Medicaid enrollment (both standard and expansion alike) on a monthly basis for every state dating back to the ACA being signed into law.

For the various enrollment data, I'm using data from Medicaid.gov's Medicaid Enrollment Data Collected Through MBES reports. Unfortunately, they've only published enrollment data through December 2020. In most states I've been able to get more recent enrollment data from state websites and other sources; unfortunately, South Carolina isn't among them, though I've estimated January enrollment based on CMS's just-released Monthly Medicaid & Chip report (which use a slightly different methodology than the MBES reports).

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

The South Carolina Insurance Dept. released their final/approved 2021 Individual and Small Group Market premium rate changes.

I actually never got around to analyzing the preliminary rate filings for SC, so I don't actually know whether any of these are changes from the original filings, but whatever. In the end, the Palmetto State's individual market premiums will be dropping by about 1.5%, while their small group rates will be increasing by 4.7% on average.

It's also worth noting that UnitedHealthcare of SC is joining the South Carolina small group market for the first time next year (not to be confused with "UnitedHealthcare Insurance Co." and "UnitedHealthcare Insurance Co. of the River Valley...no confusion there I'm sure...)

Last March I wrote an analysis of H.R.1868, the House Democrats bill that comprises the core of the larger H.R.1884 "ACA 2.0" bill. H.R.1884 includes a suite of about a dozen provisions to protect, repair and strengthen the ACA, but the House Dems also broke the larger piece of legislation down into a dozen smaller bills as well.

Some of these "mini-ACA 2.0" bills only make minor improvements to the law, or make improvements in ways which are important but would take a few years to see obvious results. Others, however, make huge improvements and would be immediately obvious, and of those, the single most dramatic and important one is H.R.1868.

The official title is the "Health Care Affordability Act of 2019", but I just call both it and H.R.1884 (the "Protecting Pre-Existing Conditions and Making Health Care More Affordable Act of 2019") by the much simpler and more accurate moniker "ACA 2.0".

Yes, that's right: Not only did they lop 50,000 people out of the loop entirely, the other 90 - 100K enrollees will also be subject to...wait for it...work requirements. Well...sort of; keep reading.

First, it looks like they'll have to apply to at least 48 employers as well. So...what, if they get hired by the first one they still have to apply with 47 more?

Note that it says "and" before the fourth item, not "or"...which means all of them will have to register online, complete a training assessment, apply to at least 48 companies and complete an online training course.

...Oh by the way, one more thing: The minimum wage in Utah is $7.25/hour.

The South Carolina Insurance Dept. released their final/approved 2020 Individual and Small Group Market premium rate changes a few days ago.

Previously, I only had the unweighted averages, which were a 1.9% decrease on the Indy market and an 11% increase for small group enrollees...but SCDOI has included the weighted averages for each in their approved numbers: A 3.9% drop and 7.6% increase respectively.

It's also worth noting that the Individual market is growing from three carriers to five next year--both Bright Health Co. and Molina Healthcare are joining the South Carolina market for the first time.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

{kind=link}