Last winter and spring, you may recall that I crunched a ton of data to come up with my best estimates about just how many people were projected to lose their healthcare coverage at the Congressional District level in the event various versions of Affordable Care Act repeal/replacement bills were to be signed into law (the AHCA, BCRAP, ORRA and so forth). After the first couple of attempts, the folks over at the Center for American Progress took over much of the heavy lifting on my part.

CAP started breaking the numbers out, leaving me to separate them out into easily-sharable state-level infographics (I also added partisan info for each member of Congress, since every Democrat has been steadfastly opposed to each one of these bills, while just about every Republican has supported most of them so far).

It's not over yet, since the House of Representatives still has to vote on the bill again (either as is, or after hashing out the differences between the House and Senate versions of the bill), but assuming the final version of the bill includes mandate repeal and is indeed signed into law, this is what the ACA's 3-legged stool would look like when the dust settles.

Obviously I'll have much more to say about what happened last night soon, but for the moment I'll leave it at this.

The Centers for Medicare & Medicaid Services’ Center for Consumer Information and Insurance Oversight (CCIIO), part of the Department of Health & Human Services (DHHS), provides national leadership in setting and enforcing standards for health insurance that promote fair and reasonable practices to ensure that affordable, quality health coverage is available to all Americans. The center also provides consumers with comprehensive information on coverage options currently available so they may make informed choices on the best health insurance for their family.

...but among other things, they're the folks who actually implement the ACA, including, among other things, HealthCare.Gov (I'm not sure if it's the same team that operates HC.gov or not...probably a lot of overlap between the two?).

Consumer Information and Insurance Oversight

Ensuring the Affordable Care Act Serves the American People

A few days ago I noted that I had seriously misunderstood the Congressional Budget Office's individual market premium projections in the event the ACA's individual mandate is repealed: Yes, it'd be ugly, but not nearly as bad as I thought, although they still expect up to 13 million people to lose coverage as a result.

Yesterday, the Center for American Progress did an analysis which broke out those 13 million by state...along with the impact on individual market premiums and the 25 billion in immediate Medicare cuts which the GOP's tax bill would implement.

While I have my own doubts about some of the CBO's assumptions, there can be no doubt that premiums would increase substantailly, millions of people would end up without healthcare coverage, and the $25 billion in Medicare cuts do appear to be locked in if the GOP's bill were to become law:

Things were looking pretty dicey for two of Montana's three insurance carriers participating on the individual market the past few days. One of the three, Blue Cross Blue Shield, saw the writing on the wall regarding Cost Sharing Reductions (CSR) likely being cut off and filed a hefty 23% rate hike request with the state insurance department. The other two, however (PacificSource and the Montana Health Co-Op, one of a handful of ACA-created cooperatives stll around), assumed that the CSR payments would still be around next year and only filed single-digit rate increases.

I'm not going to speculate as to the reasons why they both did so when it was patently obvious that having the CSRs cut off was a distinct possibility, although I seem to recall the CEO of the Montana Co-Op said something about their hands being tied since CSR reimbursement payments are legally required, after all. Basically, it sounds like he was genuinely trying to avoid passing on any more additional costs to their enrollees than they had to.

With the 2018 Open Enrollment Period coming up just 5 days from now, it's time to put this to bed: After 6 months of painstaking research and analysis, I've compiled a comprehensive analysis of the weighted average rate changes for unsubsidized ACA-compliant individual market policies in 2018, including both the on- and off-exchange markets. It's already been confirmed by a different analysis by healthcare consulting firm Avalere Health, which used a completely different methodology to arrive at the exact same conclusion: The national average increase is between 29-30%, ranging from as low as a 22% average premium drop in Alaska (thanks to their successful reinsurance program) to as high as a painful 58% increase in Virginia.

With the 2018 Open Enrollment Period coming up just 5 days from now, it's time to put this to bed: After 6 months of painstaking research and analysis, I've compiled a comprehensive analysis of the weighted average rate changes for unsubsidized ACA-compliant individual market policies in 2018, including both the on- and off-exchange markets. It's already been confirmed by a different analysis by healthcare consulting firm Avalere Health, which used a completely different methodology to arrive at the exact same conclusion: The national average increase isbetween 29-30%, ranging from as low as a 22% average premium drop in Alaska(thanks to their successful reinsurance program) to as high as a painful 58% increase in Virginia.

With only 5 days to go before the launch of the 2018 Open Enrollment Period, time is rapidly running out for me to wrap up my 2018 Rate Hike Project. I started this, as I have for 3 years now, back in late early May with the very first requested rate changes out of Virginia, and have been tracking all 50 states as the summer and fall have passed, following every twist and turn of the insane repeal/replace circus in Congress, Trump's bloviating and blathering about "blowing things up" and "letting Obamacare explode", the last-ditch "Graham-Cassidy" sideshow and everything else, right up to and through Trump lowering the boom on cutting off CSR reimbursement payments.

I'm still missing final 2018 rate data for 6 states, but in the meantime I'm also doing some cleanup of some of the states I thought I already had final data for. Today both my home state of Michigan as well as Washington State released their official, approved increase tables.

However, I do give the Michigan Dept. of Insurance & Financial Services huge credit for making it incredibly easy for me to plug their data in. Look at that...they list all carriers, whether they sell on or off exchange, the exact average rate increases, and even include the number of affected enrollees, which is usually the hardest number for me to track down. Thanks, MI DIFS!!

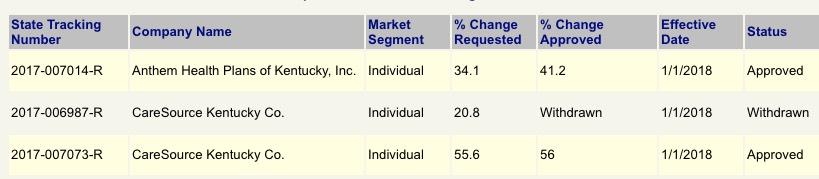

When I ran the requested rate hike numbers for Kentucky in early August, it looked like the only 2 carriers participating in the individual market next year (CareSource and Anthem BCBS) were asking for pretty hefty hikes of around 30.8% on average...and that assumed CSR reimbursement payments would be made next year. If they aren't, based on the Kaiser Family Foundation's estimates, I tacked on an additional 13.8% for a requested average of 44.3%. Ouch.