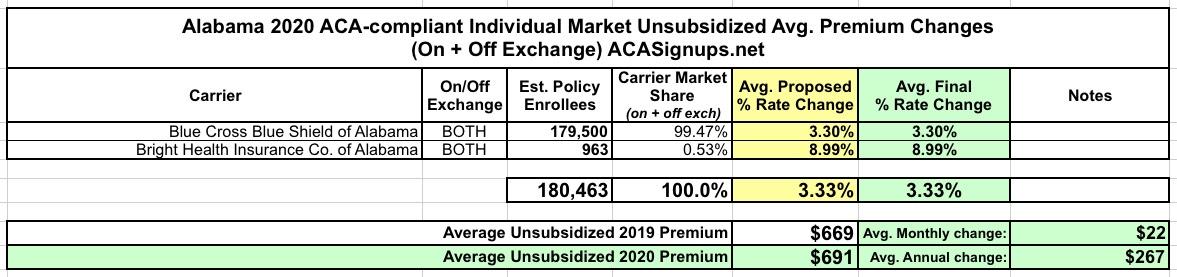

When I first ran the preliminary 2020 ACA premium rate filing requests for Alabama in August, I came up with a weighted average increase of 3.9%.

CMS has just posted the final, approved rates for Alabama's 2 carriers (Blue Cross Blue Shield and Bright Health). Both carriers had their requested rate hikes approved without any changes, but the final weighted average for unsubsidized enrollees still dropped a bit to 3.3%...because I had the wrong market share ratios. It looks like Bright has an even smaller share of the market than I thought (less than 1%), bringing the weighted average down a bit.

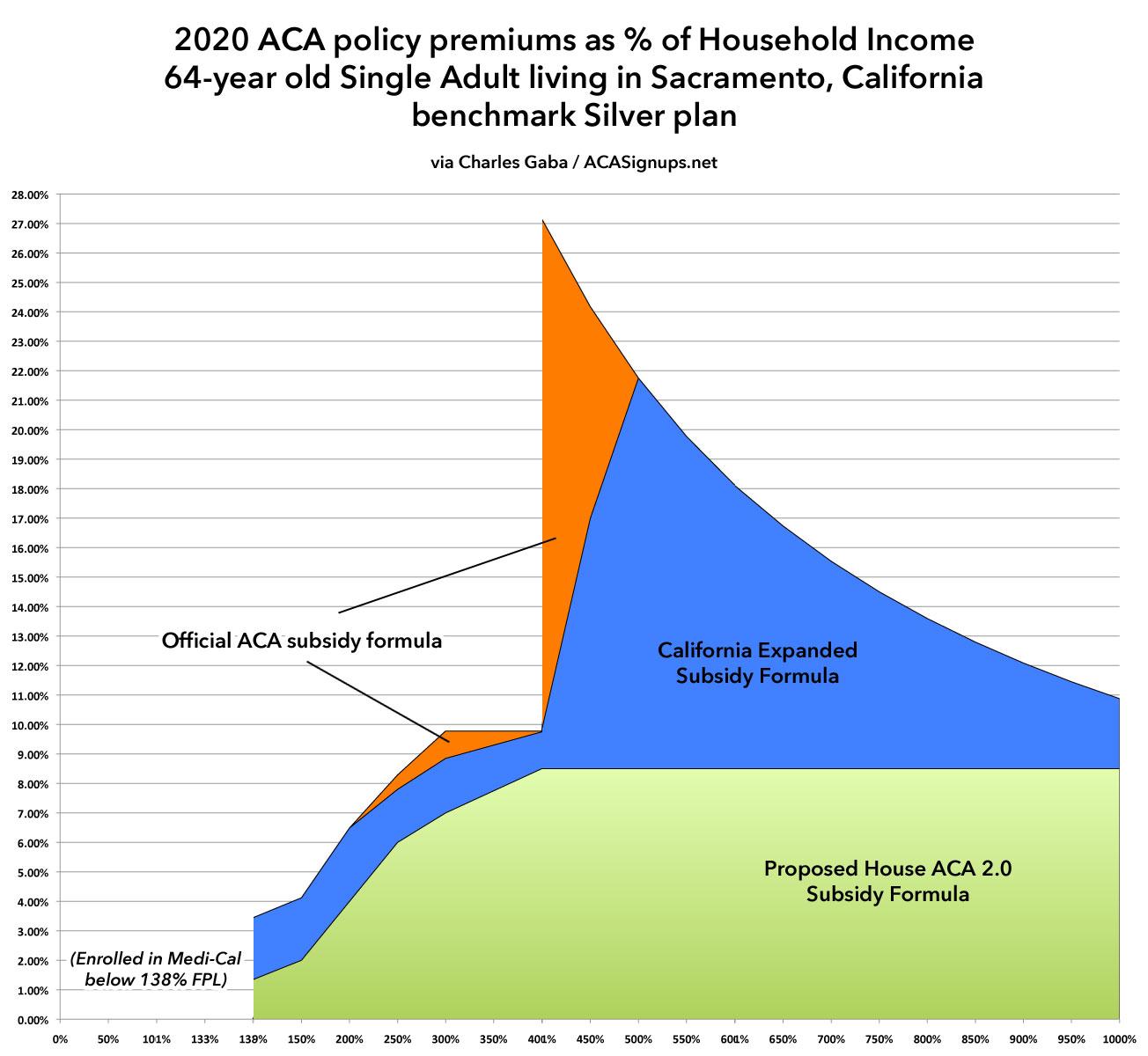

It's also important to keep in mind that due to how the ACA's subsidy formula is structured (combined with Silver Loading and Silver Switching), a lower benchmark premium will actually result in higher net premiums for many subsidized enrollees (although it's still good news for those who are unsubsidized). Here's why:

Let's say the unsubsidized premiums for a given enrollee in 2019 is $400 for Bronze, $600 for the benchmark Silver and $700 for Gold.

Let's say that enrollee earns exactly $32K/year (256% FPL), meaning they only have to pay 8.54% of their income for the benchmark plan.

That means they qualify for ($7,200 - $2,733) = $4,467 in subsidies ($372/month).

This would leave them paying $228/month for the benchmark Silver...but they can apply that towards a Bronze plan if they wish so they'd only pay $28/month, or a Gold plan so they only pay $328/month.

A week or so ago I noted that several of the 13 state-based exchanges (remember, Nevada split off of HC.gov this year) had opened up their ACA exchange websites for prospective enrollees to window shop for 2020 coverage. One of them, Covered California, actually started allowing people to enroll already; the rest were for comparison shopping only.

Well, as of today, residents of every state can window shop for 2020 healthcare policies, because HealthCare.Gov has followed suit and is now letting you plug in your household & income info to see what plans are available next year, what the unsubsidized premiums are, and (most importantly for a lot of people) what sort of financial assistance you may be eligible for.

There have been some interesting modifications to the interface and workflow of HC.gov this year:

Premiums for HealthCare.gov Plans are down 4 percent but remain unaffordable to non-subsidized consumers

Today, the Centers for Medicare & Medicaid Services (CMS) announced that the average premium for the second lowest cost silver plan on HealthCare.gov for a 27 year-old will drop by 4 percent for the 2020 coverage year. Additionally, 20 more issuers will participate in states that use the Federal Health Insurance Exchange platform in 2020 bringing the total to 175 issuers compared to 132 in 2018, delivering more choice and competition for consumers. As a result of the Trump Administration’s actions to stabilize the market, Americans will experience lower premiums along with greater choice for the second consecutive year.

Back in early August, I ran the preliminary average unsubsidized 2020 individual market rate changes in Arizona. At the time, I had the requested rate changes for both the individual and small group markets, but not the actual enrollment numbers for each carrier, so I had no way of calculating the weighted average. I instead settled for a simple unweighted average, which came in at around a 2.4% reduction in premiums on the individual market and a 5.2% increase on the small group market.

A few days ago, the Arizona Insurance Dept. released the final/approved 2020 rate changes, and there was only one significant change: Health Net of AZ (dba Arizona Complete Health), which had requested a 2.9% rate reduction, will instead be keeping their premiums flat year over year on average. With Health Net holding over 50% of the market share, this meant that the statewide average is a bit higher than I had it previously.

Back in July, the Pennsylvania Insurance Dept. posted the preliminary/requested 2020 average premium rate changes for the individual and small group markets. The ACA-compliant individual market average increase was around 4.6%; for small businesses, the average was 9.6%.

Today they finally posted the approved rate changes for each...and the indy market average has dropped to a 3.8% increase, while the small group market has gone up just a hair to 9.7%.

I'm not sure how this slipped by me, but in addition to Covered California already having launched their 2020 Open Enrollment Period yesterday, five other state-based ACA exchanges are already partly open as well. That is, you can shop around, compare prices on next year's health insurance policies and check and see what sort of financial assistance you may be eligible for:

I'm not sure when the other 7 state-based exchanges will launch their 2020 window shopping tools, nor do I know when HealthCare.Gov's window shopping will be open for the other 38 states, although I believe they usually do so about a week ahead of the official November 1st Open Enrollment Period launch date.

I also noted that there's two important points for CA residents to keep in mind starting this Open Enrollment Period:

First: The individual mandate penalty has been reinstated for CA residents. If you don't have qualifying coverage or receive an exemption, you'll have to pay a financial penalty when you file your taxes in 2021, and...

Second: California has expanded and enhanced financial subsidies for ACA exchange enrollees:

Until now, only CoveredCA enrollees earning 138-400% of the Federal Poverty Line were eligible for ACA financial assistance. Starting in 2020, however, enrollees earning 400-600% FPL may be eligible as well (around $50K - $75K/year if you're single, or $100K - $150K for a family of four). In addition, those earning 200-400% FPL will see their ACA subsidies enhanced a bit.

While the 2020 Open Enrollment Period doesn't officially start until November 1st across the rest of the country, in California it begins two weeks earlier, for whatever reason:

In most states, open enrollment for 2020 coverage will run from November 1, 2019 to December 15, 2019. But California enacted legislation (A.B.156) in late 2017 that codifies a three-month open enrollment period going forward — California will not be switching to the November 1 – December 15 open enrollment window that other states are using.

Instead, California’s open enrollment period (both on- and off-exchange) will begin each year on October 15, and will continue until January 15. Under the terms of the legislation, coverage purchased between October 15 and December 15 will be effective January 1 of the coming year, while coverage purchased between December 16 and January 15 will be effective February 1.

I posted Wisconsin's preliminary 2020 rate filings in early August. Yesterday the state insurance department posted this press release, which includes the final, approved rate changes. As far as I can tell, nothing has changed (the final statewide weighted average is a 3.2% average premium reduction over last year, thanks primarily to them implementing a fairly robust ACA Section 1332 reinsurance waiver:

Gov. Evers Announces More Health Insurance Options for Wisconsinites in 2020 Ahead of Open Enrollment

{kind=link}