Back in July, I noted that the Minnesota Commerce Department announced the preliminary 2020 rate changes for carriers on the individual and small group markets. At the time, the weighted average increases were roughly 1.6% and 5.5% respectively, although the enrollment estimates for each carrier were estimates only.

Today, the MN Commerce Dept. announced the approved rates for 2020, and in both markets, they shaved average premiums down a couple of points. Here's the actual Commerce Dept. press release:

Commerce releases 2020 health insurance rates for Minnesota

Minnesota’s individual and small group health insurance market rates for 2020 reflect stabilized markets, according to information released today by the Minnesota Department of Commerce in advance of the open enrollment period beginning November 1.

LAS VEGAS (KLAS) — In a statement issued by Nevada Health Link, the organization announced that it had become aware that the Federal Health Insurance Marketplace, known as HealthCare.gov had incorrectly sent notices to Nevada consumers regarding the upcoming open enrollment period.

The incorrect notices were sent to Nevada consumers via mail, email and through notices on the HealthCare.gov portal.

"These notices from the Marketplace were sent in error. Nevadans who received these notices from the Marketplace should be aware that NevadaHealthLink.com is the only place to get enrolled in a qualified health plan during the next open enrollment period beginning on November 1, 2019," said Heather Korbulic, Executive Director for the Silver State Health Insurance Exchange.

Nevada consumers are asked to reach out to the Nevada Health Link consumer assistance center for further questions by calling 1-800-547-2927.

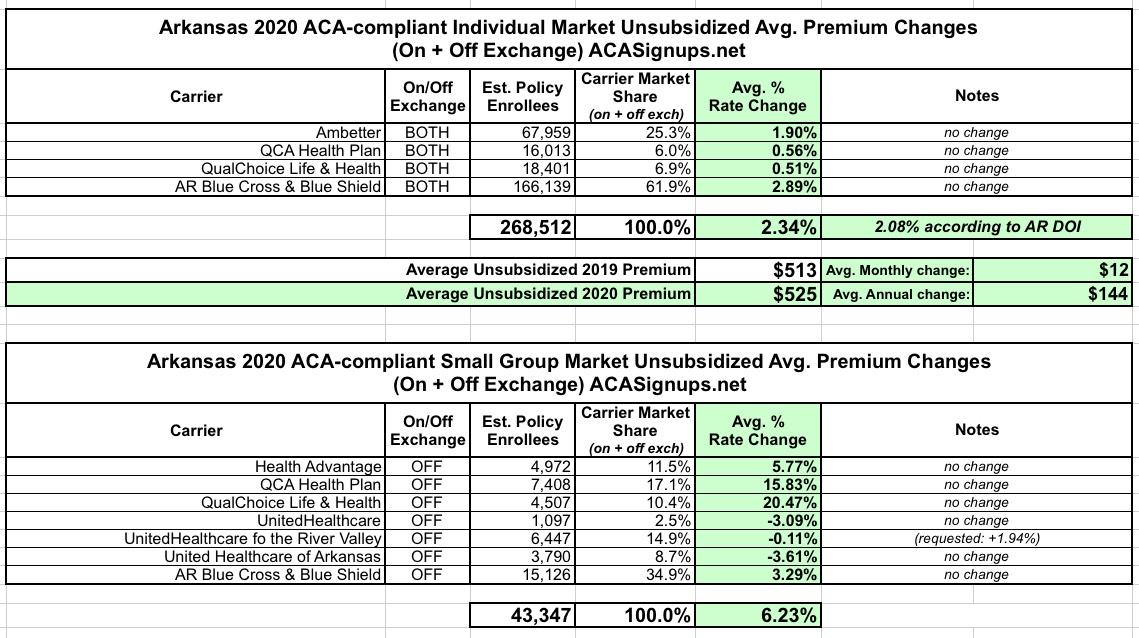

The Arkansas Insurance Dept. just posted their approved 2020 individual and small group market premium rate change requests. For the most part it's pretty straightforward: Individual market premiums are increasing about 2.3% statewide, while small group plans are going up 6.2% overall. This is virtually unchanged from their preliminary rate requests in July, although a single small group carrier had their request reduced from +2% to -0.1%, lowering the overall weighted average by a mere 0.2 points:

Regular readers may have noticed that this is my first blog entry in several days, which is unusual for me. I admit I've been mesmerized by the dramatic Trump/Ukraine/Impeachment saga which has exploded over the past few days.

I'm back in gear today, however, and I'm starting things off with my latest freelance piece over at healthinsurance.org. It's basically a summary explainer of where things stand re. 2020 ACA individual market premiums. As anyone who follows this site knows, the answer this year is basically...FLAT, at least nationally.

The irony of this, of course, is that the 800 pound gorilla in the room is the pending #TexasFoldEm lawsuit decision by the 5th U.S. Court of Appeals, which could potentially tear down the entire Affordable Care Act...and their decision in the case is expected to be released any time over the next five weeks...just ahead of the 2020 Open Enrollment Period.

Long-time readers may have noticed that, while I've obviously ripped on the Trump Administration a lot for the various ways they've screwed around with administration of the ACA over the past 2 1/2 years, there's a handful of actions they've taken which I haven't criticized them for...or at least, which I've been fairly circumstpect about being too critical about.

The biggest, and perhaps most surprising, of the latter is the Centers for Medicare & Medicaid (CMS) decision to shorten the offiical Open Enrollment Period (OEP) roughly in half, from three months (Nov. 1st - Jan. 31st) down to just six weeks (Nov. 1st - Dec. 15th). There's a couple of reasons for this.

Overall individual rates increased an average of 9.0 percent and small group rates increased an average of 10.5 percent. In the individual market, CareFirst proposed an average increase of 7.7 percent for HMO plans, and 15.6 percent for PPO plans. Kaiser proposed an average increase of 5.0 percent. For small group plans, CareFirst filed average rate increases of 13.5 percent for HMO plans and 18.5 percent for the PPO plans. Kaiser small group rates proposed an average increase of 3.0 percent. Aetna filed for an average increase of 16.1 percent for HMO plans and 5.0 percent for PPO plans. Finally, United proposed an average increase of 13.0 percent and 7.4 percent for its two HMOs and 11.2 percent for its PPO plans.

Cigna extended its individual healthcare exchange products for the 2020 plan year, the insurer said Sept. 18.

For 2020, individuals can purchase individual health plans in 19 markets across 10 states. The expansions will take place in counties in Kansas, South Florida, Utah, Tennessee and Virginia. The other states include Arizona, Colorado, Illinois and North Carolina.

The plans will be available for purchase on the individual marketplace during the 2020 open enrollment period, which begins Nov. 1. Plans will take effect Jan. 1.

Interactive tracker helps tell the story of insurer participation in the ACA market.

The seventh open enrollment season is almost upon us, and all signs point to growing stability, as measured by moderate premium increases and increased participation by health plans. The tracker shows the change over time in participation at the county level, and allows users to follow individual companies or categories of health insurers. The data reveal a business narrative that has been closely intertwined with the political story of the Affordable Care Act (ACA) marketplace.

One of the interesting quirks of how the Affordable Care Act's enhancement of our crazy patchwork heatlhcare system works is that there's something of a zero-sum game when it comes to enrollment numbers.

For instance, Virginia's ACA exchange enrollment numbers dropped by 18% this year, from 400,000 to 328,000, due primarily to the state finally getting around to expanding Medicaid to enrollees earning less than 138% of the Federal Poverty Level. Since people earning between 100-400% FPL are eligible for ACA subsidies if they enroll through the exchange, that means there's an overlap for those in the 100-138% range which these folks fell into. The same thing happened in Louisiana, even more dramatically, after they expanded Medicaid halfway through 2016...the following year exchange enrollment dropped by 33%.

Last month I noted that North Dakota had posted their requested 2020 premium rate change requests, including two different filings: One assuming the states' ACA Section 1332 Reinsurance Waiver didn't get approved, the other assuming it did. It was pretty unlikely that their waiver would be denied, however, so the general assumption was that they'd be looking at a significant rate reduction, especially compared with the rate increase if the waiver didn't go through.

At the time, I didn't have access to the actual enrollment figures for the three carriers on North Dakota's individual market, so I had to go with an unweighted average rate change, and came up with a drop of 7.9%.