Nevada Health Link Saves Thousands of Nevadans Money Through 2021 Special Enrollment Periods

CARSON CITY, Nev. (May 17, 2021) –Nevada Health Link, the online health insurance marketplace operated by the state agency, the Silver State Health Insurance Exchange (Exchange), has enrolled more than 7,600 Nevadans since the implementation of two Special Enrollment Periods in 2021, including more than 4,500 enrollees since April 20, attributed to the American Rescue Plan Act (ARPA or American Rescue Plan).

The American Rescue Plan, which was signed into law on March 11, provides Nevadans with a Special Enrollment Period where insured and uninsured Nevadans can take advantage of new, drastically reduced insurance premiums from now until August 15.

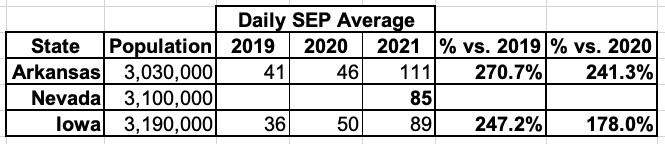

There's no formal press release yet, but I've confirmed that the Nevada Health Link ACA exchange has enrolled 6,908 additional Nevadans in ACA exchange coverage via the COVID Special Enrollment Period as of yesterday (5/06) so far.

This breaks out to around 85 per day from 2/15 - 5/06.

Unfortunately, I don't have Nevada's 2019 or 2020 SEP enrollment handy for comparison, but NV's statewide population (3.10) is right in between Arkansas (3.03 million) and Iowa (3.19 million), which at least allows for a rough comparison:

This strongly suggests that Nevada's 85/day average is perhap 2.5x higher than 2019 and perhaps twice as high as 2020, although 2020 is a fuzzier comparison since HC.gov didn't have a COVID SEP last year while the Nevada Health Link did.

Nevada Health Link Announces Health Insurance Savings Through the American Rescue Plan Act

Nevadans seeking health coverage can access increased or expanded subsidies and premium savings, healthcare tax credits, expanded COBRA protections and increased plan options

CARSON CITY, Nev. (April 16, 2021) – Nevada Health Link, the online health insurance marketplace operated by the state agency, the Silver State Health Insurance Exchange (Exchange), is offering even bigger coverage savings to eligible uninsured and insured off-Exchange Nevadans. These new enhancements are in accordance with the newly-enacted American Rescue Plan Act (ARPA or American Rescue Plan) of 2021 passed by Congress and signed into law by President Biden on March 11, 2021.

Nevada Health Link opened a Special Enrollment Period (SEP) for uninsured Nevadans, starting February 15 through August 15, 2021. The SEP is in accordance with the Executive Order issued by President Biden last month, in response to the ongoing national emergency presented by COVID-19.

Coming soon! Thanks to the recently passed American Rescue Plan, we’ll soon be offering more money to help pay for your coverage. Learn more here.

The Division of Insurance (“Division”) encourages all Nevadans to take advantage of the new saving opportunities offered by the American Rescue Plan Act of 2021 (“ARPA”). The ARPA, enacted earlier this month, creates more opportunities for Nevadans to save on health insurance coverage.

“I urge consumers, especially those who have off-exchange plans, have no insurance or have found themselves uninsured to start thinking now about how they can benefit from this new law because certain benefits in the ARPA have deadlines,” said Insurance Commissioner Barbara Richardson. “Each month that a consumer does not take advantage of these new low or no cost opportunities, they are leaving money on the table.”

The ARPA will lower monthly premium costs; increase subsidy eligibility for consumers making above the 400% of the Federal Poverty Level; provide options for people who are on unemployment for $0 premium plans; and it will provide 100% COBRA subsidy for six months.

Statement re: 11th Anniversary of the Affordable Care Act

Heather Korbulic, executive director, Silver State Health Insurance Exchange

Tomorrow, March 23, 2021, marks 11 years since the passing of the Affordable Care Act (ACA), the landmark reform law that is credited with increasing access to quality healthcare for millions of Americans, forever changing the national healthcare landscape.

Here in Nevada, the ACA is responsible for the creation and ongoing operations of the Silver State Health Insurance Exchange that has provided healthcare coverage to hundreds of thousands of Nevadans who would otherwise be without coverage to receive essential and critical healthcare services. Since the passage of the ACA and the implementation of Nevada Health Link, the Exchange’s online marketplace for ACA-compliant insurance plans, Nevada's number of uninsured has decreased from a staggering 23 percent to 11 percent.

In the face of the continuing COVID-19 pandemic, President Joe Biden reopened enrollment in the Affordable Care Act’s health insurance exchanges.

For Nevadans, that means the Silver State Health Insurance Exchange is back in business.

The exchange connects Nevadans to health plans compliant with the Affordable Care Act, and it’s the only place consumers can access any federal subsidies.

“As soon as Nevada learned of the news from the federal government, we took immediate action to plan and collaborate with our insurance carriers and the statewide network of 750-plus brokers and navigators to implement a seamless, streamlined process for Nevadans,” said Heather Korbulic, executive director of Silver State Health Insurance Exchange.

Korbulic told KNPR's State of Nevada that there has already been a lot of interest from people around the state.

"We're pretty excited about the uptake that we've already started seeing and we think this is a wonderful opportunity for Nevadans to get connected to Nevada HealthLink," she said.

Special Enrollment Period through Nevada Health Link begins February 15

Uninsured Nevadans will have 90 more days to enroll in a qualified health plan for 2021 coverage

Nevada Health Link, the online health insurance marketplace operated by the state agency, the Silver State Health Insurance Exchange (Exchange), begins its 90-day Special Enrollment Period (SEP) for uninsured Nevadans, starting February 15 through May 15, 2021. The SEP is in accordance with the Executive Order issued by President Biden last month, in response to the ongoing national health emergency presented by COVID-19.

Today, the Biden‐Harris Administration announced a Special Enrollment Period, allowing Americans to enroll and purchase on‐Exchange health insurance plans from their respective on‐Exchange marketplaces. On behalf of the Silver State Health Insurance Exchange and Nevadans statewide, we are pleased to see positive change taking place at the federal level and to witness the fast‐moving actions to protect the Affordable Care Act (ACA), upon which so many Americans rely for quality, affordable and comprehensive health insurance coverage.

This news comes on the heels of our announcement that nearly 82,000 Nevadans enrolled on Nevada Health Link for coverage in 2021. That’s nearly a six percent increase from last year’s enrollment total.

Today’s news from the White House speaks volumes about how the new Administration will continue to support the ACA and help to bolster the health insurance marketplace, protecting hundreds of millions of Americans.

Nevada’s State Based Exchange enrolls nearly 82,000 Nevadans during Open Enrollment Period for 2021 coverage

Enrollment exceeds 2019 figures by nearly 6 percent

(CARSON CITY, NV) – The Silver State Health Insurance Exchange (Exchange), Nevada’s state agency that helps individuals get connected to budget-appropriate health coverage through the online marketplace, Nevada Health Link, enrolled 81,903 Nevadans during the 2020 health insurance Open Enrollment Period, connecting tens of thousands of Nevadans statewide to Affordable Care Act (ACA) compliant health plans. These enrollment figures exceed 2019’s enrollment figures by 4,493 – a 5.8 percent increase.