The overall average rate increase for 2020 Indiana individual marketplace plans is 9.0%. CareSource and Celtic (MHS/Ambetter) have filed to participate in the 2020 Indiana Individual Marketplace. The Department of Insurance anticipates that all 92 counties in Indiana will be covered by both CareSource and Celtic (MHS/Ambetter).

Anthem has filed to offer a 2020 Off-Marketplace plan in Indiana. This plan is a catastrophic plan and is offered only in Benton, Jasper, Newton, Warren and White Counties.

Filing a rate does not guarantee it will be approved for use on the Marketplace, nor does the filed rate guarantee to be the final rate. Therefore, the Department of Insurance is not able to ascertain the amount of any final rates at this time. The state has until September 24, 2019 to review and submit dispositions to U.S. Department of Health and Human Services.

Back in June, Indiana's 3 individual market carriers submitted their requested 2019 ACA rate changes, which averaged around 5.1%. At the time I also pegged the impact of #ACASabotage on 2019 rates (mandate repeal + #ShortAssPlans) at around 13 percentage points.

Like last year, there's only three carriers participating in Indiana's individual market: CareSource and Celtic (aka Ambetter) will again be available both on and off the ACA exchange, while Anthem will only be offering a single Catastrophic plan on the off-exchange market in just five counties:

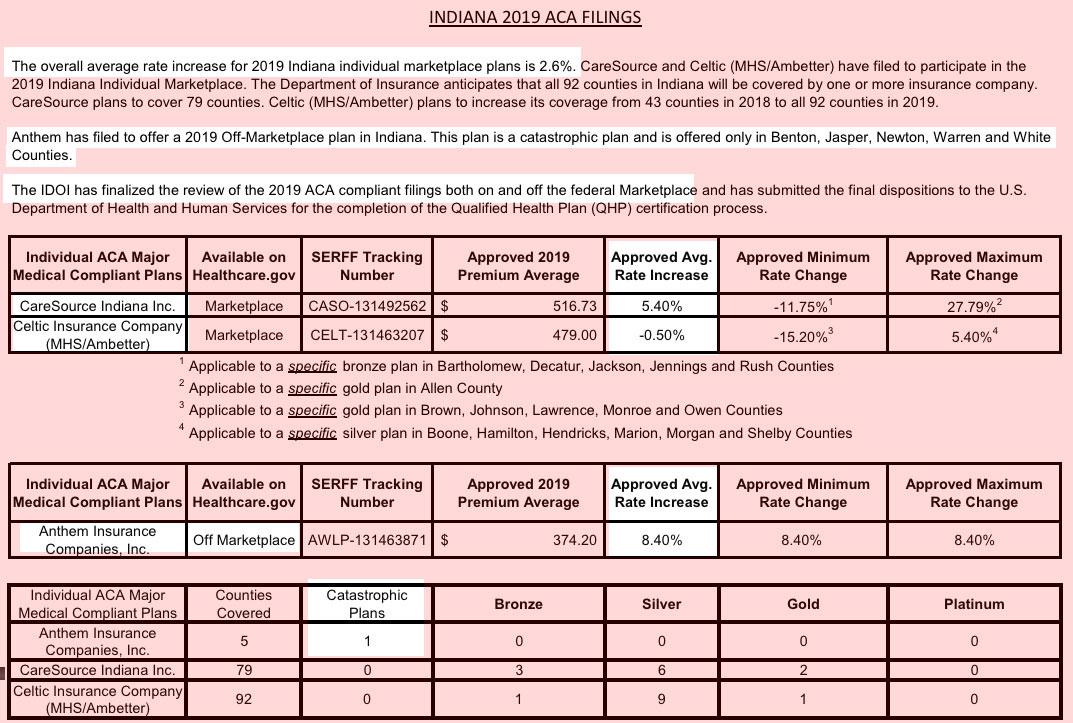

The overall average rate increase for 2019 Indiana individual marketplace plans is 5.1%. CareSource and Celtic (MHS/Ambetter) have filed to participate in the 2019 Indiana Individual Marketplace. The Department of Insurance anticipates that all 92 counties in Indiana will be covered by one or more insurance company. CareSource plans to cover 79 counties. Celtic (MHS/Ambetter) plans to increase its coverage from 43 counties in 2018 to all 92 counties in 2019.

Anthem has filed to offer a 2019 Off-Marketplace plan in Indiana. This plan is a catastrophic plan and is offered only in Benton, Jasper, Newton, Warren and White Counties.

Indiana Adds Work Requirement To Medicaid, Will Block Coverage If Paperwork Is Late

PHIL GALEWITZ

Indiana on Friday became the second state to win federal approval to add a work requirement for adult Medicaid recipients who gained coverage under the Affordable Care Act. A less debated provision in the state's new plan could lead to tens of thousands of people losing coverage if they fail to complete paperwork documenting their eligibility for the program.

The federal approval was announced by Health and Human Services Secretary Alex Azar in Indianapolis.

Medicaid participants who fail to promptly submit paperwork showing they still qualify for the program will be locked out of enrollment for three months, according to updated rules.

Protect Our Care is a healthcare advocacy coalition created last December to help fight back against the GOP's attempts to repeal, sabotage and otherwise undermine the Affordable Care Act. This morning they released a report which compiled the approved 2018 individual market rate increases across over two dozen states.

Needless to say, they found that the vast majority of the state insurance regulators and/or carriers themselves are pinning a large chunk (and in some cases, nearly all) of the rate hikes for next year specifically on Trump administration sabotage efforts...primarily uncertainty over CSR payment reimbursements and, to a lesser extent, uncertainty over enforcement of the individual mandate penalty.

Louise Norris gave me a heads' up regarding the Indiana 2018 rate filings. Anthem BCBS and MDwise, which currently have around 46,000 and 30,800 exchange enrollees each, are dropping out next year, meaning nearly 77,000 people will have to shop around. Anthem is sticking around the off-exchange market....but only in a handful of counties. Norris indicates around 64,687 total Anthem enrollees; minus the 46K on-exchange, that leaves roughly 18.7K off-exchange enrollees, virtually all of whom are expected to drop due to Anthem dropping out of all but 5 counties (plus, of course, the large rate hike).

Of the 31 states which have expanded Medicaid under the Affordable Care Act, only a handful issue regular monthly or weekly enrollment reports.

I noted in February that enrollment in the ACA's Medicaid expansion program had increased by around 35,000 people across just 4 states (LA, MI, MN & PA).

It's early June now, so I checked in once more, and the numbers have continued to grow. I have the direct links for 5 states now (including New Hampshire)...

The last official ACA Medicaid expansion enrollment number I have recorded for Indiana (via their modified "Healthy Indiana 2.0" program) was 290,000 people way back in July 2015. At the time, the maximum potential HIP 2.0 enrollment total was 680,000 Hoosiers, made up of 350,000 newly covered plus another 330,000 being transferred over from the HIP 1.0 program.

This NPR article from a couple of weeks ago states that as of January, "the Healthy Indiana Plan that he established in 2015 as the state's governor has brought Medicaid coverage to more than 350,000 people." However, that number is a bit confusing given that they were also supposedly transferring the other 330K over from the other program as well. I'm not sure if 350K refers to total HIP 2.0 enrollment or only those who were previously uninsured.

Normally I post screenshots from the revised/updated SERFF filings and/or updates at RateReview.HealthCare.Gov, but it takes forever and I think I've more than established my credibility on this sort of thing, so forgive me for not doing so here. Besides, #OE4 is approaching so rapidly now that this entire project will become moot soon enough, as people start actually shopping around and finding out just what their premium changes will be for 2017.

The other reason I'm not too concerned about documenting the latest batch of updates/additional data is because in the end none of it is making much of a difference to the larger national average anyway; no matter how the individual carrier rates jump around in various states, the overall, national weighted average still seems to hover right around the 25% level.

Still, for the record, here's the latest...in four states (Iowa, Indiana, Maine & Tennessee) I've just updated the requested and/or approved average increases. In the other four (Massachusetts, Montana, North & South Dakota) I've added the approved rate hikes as well.

(sigh) I thought that last Friday was the deadline for carriers to decide whether they were in or out of the exchange for 2017, but between today's news out of Tennessee and now this, apparently that deadline only applies to those who will be participating in the 4th Open Enrollment Period:

IU Health Plans said Monday afternoon it had “restructured its product offerings for 2017” and no longer will be offering individual plans on the exchange. It said the change was necessary “to adapt to new market dynamics” as well as uncertainty created by withdrawals of several other insurers.