*IMPORTANT: This assumes that everyone currently enrolled sticks with their current policy next year. If enough people shop around and consider their options, the average premiums for various plans, various companies, in vartious states and nationally could end up being considerably lower (possibly coming in under 10% overall).

Again: Do not blindly autorenew! Contact your ACA exchange website/call center (or your insurance carrier, if you're enrolled directly through them) and check out your options before committing to your existing plan! In many cases, there will be a different plan which is a better value for you!

At last!! It's been extremely frustrating trying to lock down the 2016 average premium hikes for Pennsylvania, especially because their Insurance Dept. website has actually been very good about posting every requested rate change in an easy-to-read, comprehensive fashion.

The problem with PA's rate filings hasn't been on the percentage change side, it's on the covered lives side. I was able to compile enrollment numbers for some carriers but not others...including First Priority, which was requesting a 29.5% rate hike. Without knowing whether they had a huge chunk of the market or not, posting the "average" rate hikes without including theirs was kind of meaningless, since it could potentially jack that average up or down dramatically.

So, I finally kind of gave up on it, figuring that even when the approved rates were posted, they probably still wouldn't include the number of covered lives for each insurance company.

A couple of weeks ago, both Louise Norris and I crunched the South Carolina data and came up with different estimates of the weighted average requested 2016 rate hikes for the ACA-compliant individual market. She used a worst-case scenario and estimated it to be around 16.8%; I took a slightly more optimistic approach and came up with 15.2%.

As you can see, even though there are only 5 carriers operating on the ACA exchange and another 5 offering policies off-exchange only, the overall average is still 15.9% either way:

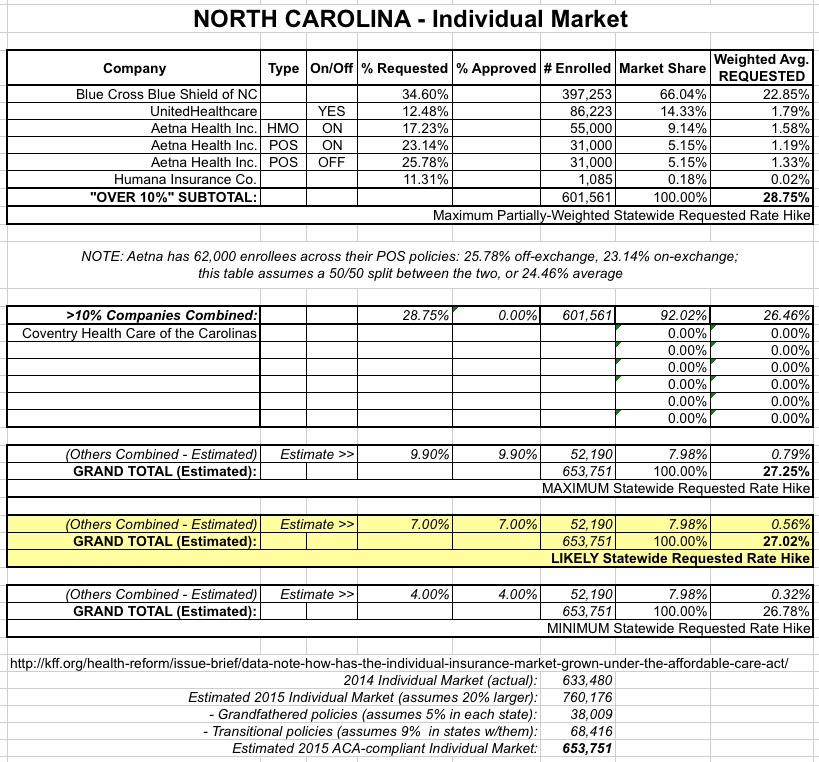

Two more health insurers in North Carolina are asking to increase their already-proposed rate increases.

UnitedHealthcare, which had requested an average rate increase of 12.5 percent, now is asking regulators to allow an an average increase of 20.4 percent. The range is 2.5 percent to 50.3 percent.

Humana had requested 11.3 percent and is now asking for an average of 24.9 percent.

Last month I wrote a quick post about the Montana individual market; with only 3 players, all of whom had requested >10% increases, it was pretty easy to plug the numbers in: 22.2%, 29.3% and 34.0%.

Commissioner Monica Lindeen's office says the average rate increase for all plans next year will range between 22 percent and 34 percent. For the popular Silver plan, the increase will range from $80 to $88 a month for a 40-year-old person.

Lindeen said Thursday the rates affect about 41,000 people. They don't include people who receive federal tax credits or those who have insurance through their employers.

The "good" news here is that the affected number is only 41K instead of the 76K I had on record. It's possible that the middle carrier had their rates changed, but overall it looks like the commissioner just signed off on the original requests, for a roughly 26% average increase.

When I ran the numbers for Georgia's individual market in August, I didn't have a whole lot to work with. The requested rate changes were only publicly available for carriers representing around 222,000 enrollees, out of a state-wide individual market of (likely) around 750,000. The weighted average increase for the companies I had data for was around 18.3%; all I knew about the rest of them is that they had asked for hikes of under 10%. My best ballpark estimate was that Georgia residents were likely looking at roughly a 10-13% increase overall.

Today I ran across an article in the Rome News-Tribune which gives some of the final, approved rate hike numbers for 2016...but just bits and pieces, nothing to hang your hat on:

Many Georgians buying individual or family health insurance will see double-digit increases in their premiums for 2016.

For 2016, HMSA has proposed a 45.5 percent rate increase for their individual HMO plan, and nearly a 50 percent rate hike for their individual PPO plan (49.1 percent overall). The carrier justified their rate hikes based on claims costs, explaining that while virtually everyone in Hawaii was already insured, the uninsured pool – many of whom purchased new ACA-compliant plans – had significant medical needs.

Ouch. Yup, that's a pretty ugly requested increase, no way around it.

The following day, Kaiser proposed an 8.7 percent rate increase for their individual market policies.

If approved as is, this would have resulted in a 33.7% average rate increase, when weighted by market share between the two companies.

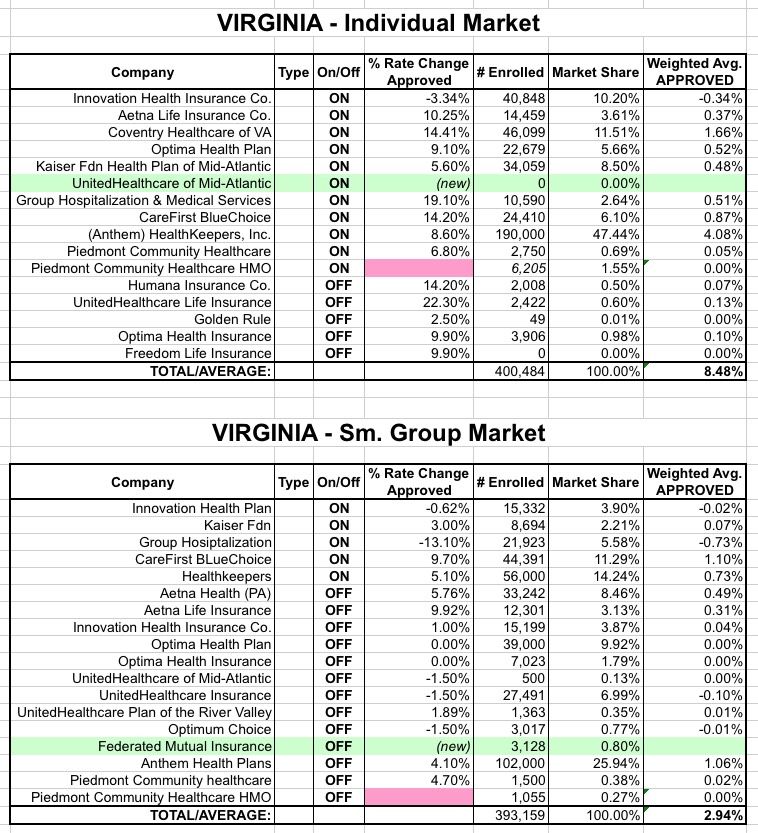

Some relatively welcome news going into the home stretch: After a series of ugly (over 20%) rate hike averages from Alabama, Delaware, South Dakota and especially Minnesota, I've just completed the Virginia analysis:

Unlike many other states, there's no guesswork or educated guesses here; the Virginia Dept. of Insurance SERFF filings are quite complete and straightforward, so I have every company providing individual and/or sm. group coverage listed, both on and off the exchange, with the exact average rate changes and affected enrollee numbers for pratically every one of them.

The only exceptions are Piedmont Community Healthcare HMO, whose SERFF filings, oddly, included the enrollee count but not the rate change (usually it's the other way around). In addition, there's a couple of new additions to each (UHC of Mid-Atlantic on the indy market, Federated Mutual on the sm. group market). However, none of these have large enough enrollment numbers to amount to more than a rounding error in either category.

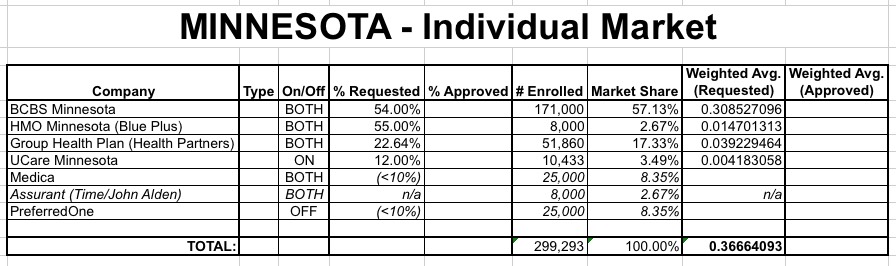

When I crunched the numbers for Minnesota's requested rate hikes, the results were pretty scary-looking; based on partial data, I estimated that the weighted average was something like a 37% overall requested increase:

Note that there were several crucial missing numbers: I didn't know the actual market share for several companies (I made a rough guess based on an estimate of the total missing enrollments), nor did I know what the requested increases were for Medica or PreferredOne, other than thinking that both were under 10%.