Earlier today I received a first: A "cease & desist"-type email from Humana Inc's "Sales Integrity Department" asking me to remove their logo from a blog post about the company:

Dear Website Owner:

Humana encourages agents and agencies (collectively, “Agents”) to promote the Humana Brand in a manner that complies with applicable laws and Humana’s own policies and procedures.

Internet-based capabilities are providing new and interactive ways to sell Humana products and services. Although these capabilities offer tremendous opportunities, they also create responsibilities for Humana and its Agents to maintain a system of controls and monitoring.

The Sales Integrity Department at Humana has done a review of websites containing the Humana logo and we have detected your use of the logo...

Updated 8/17/23: D'oh! I completely forgot about this development when I started running my state-by-state rate filing analyses this summer. No wonder Humana has disappeared from over a dozen states for 2024!

Update 3/15/23: At the request of Humana's Sales Integrity Dept., I've removed their logo from this blog entry.

Before I start, let me say that I've never been a fan of Medicare Advantage, at least as its currently structured, for a number of reasons. I am not advocating for the Medicare Advantage system--again, as currently structured--to be expanded.

Regarding the company’s individual commercial medical coverage (Individual Commercial), substantially all of which is offered on-exchange through the federal Marketplaces, Humana has worked over the past several years to address market and programmatic challenges in order to keep coverage options available wherever it could offer a viable product. This has included pursuing business changes, such as modifying networks, restructuring product offerings, reducing the company’s geographic footprint and increasing premiums.

Oh. Well, I'm sure that was just a sheer coincidence, right? No doubt Aetna will clear this up with an unequivocal statement to put any speculation to...

From Peter Sullivan of The Hill:

Asked if the DOJ’s actions on the merger had any relation to Monday’s announcement, Aetna spokesman TJ Crawford did not directly say yes or no.

For 2017, UnitedHealthcare, along with most of its subsidiaries, is discontinuing its participation in the individual market in Colorado, both on and off the exchange. However, Golden Rule Insurance, a subsidiary of UnitedHealthcare, will continue to offer its individual plans in Colorado off of the exchange. UnitedHealthcare will also continue its small and large group business in the state.

Humana will continue in the small group market for 2017 off the exchange, while exiting the individual market for both Humana Health Plans and Humana Insurance Company.

Health Insurer Aetna Inc on Wednesday said it plans to continue its Obamacare health insurance business next year in the 15 states where it now participates, and may expand to a few additional states.

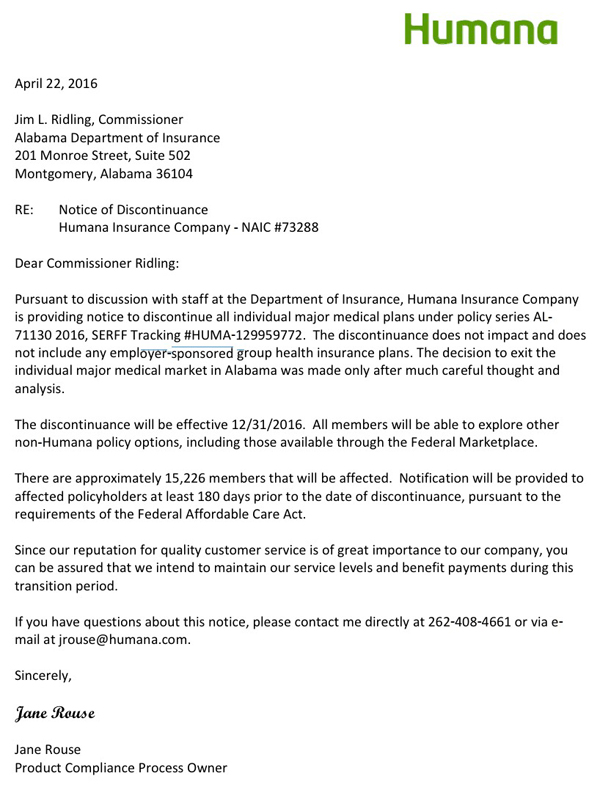

This is really just a summary of my last 4 posts. I've combed through the SERFF databases for every state which uses the system for rate filings, and while very few have the actual 2017 rate filing requests listed yet, at least 4 of them have official individual market exit letters submitted for 2017 from Jane Rouse, the Product Compliance Process Owner for Humana Insurance Co:

This list may grow as additional state filing data and/or press releases come out from Humana, but assuming these are the only 4 states Humana is bailing on, the news isn't quite as bad as it appears at first.

To be clear, I'm not saying this is a good development; when you combine it with the recent UnitedHealthcare Dropout Odometer it's more of a drip-drip-drip sort of thing. But it isn't disasterous for the exchanges either (at least not yet).

UPDATE: I've been informed by a reliable source that Humana is also dropping out of the individual market in Nevada next year, although I don't have any actual enrollment data there. Humana is not currently participating on the Nevada exchange, however, so any dropped enrollments would be OFF-exchange only. In fact, I'm pretty sure that the only individual market enrollees Humana has in Nevada are grandfathered policies anyway, so the numbers should be pretty nominal there.

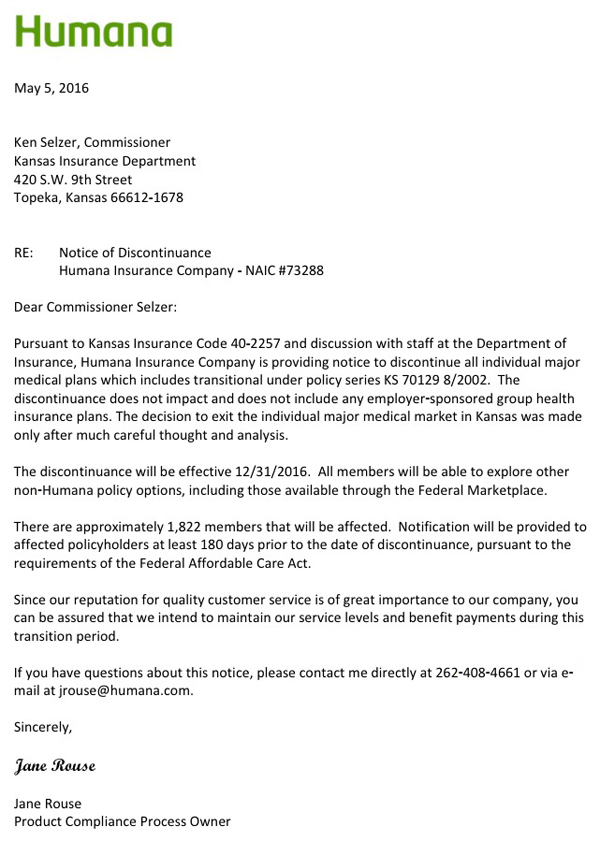

Yep, sure enough, Humana is following UnitedHealthcare out the door of multiple states next year. That's 1,800 people impacted, although they're all OFF-exchange only:

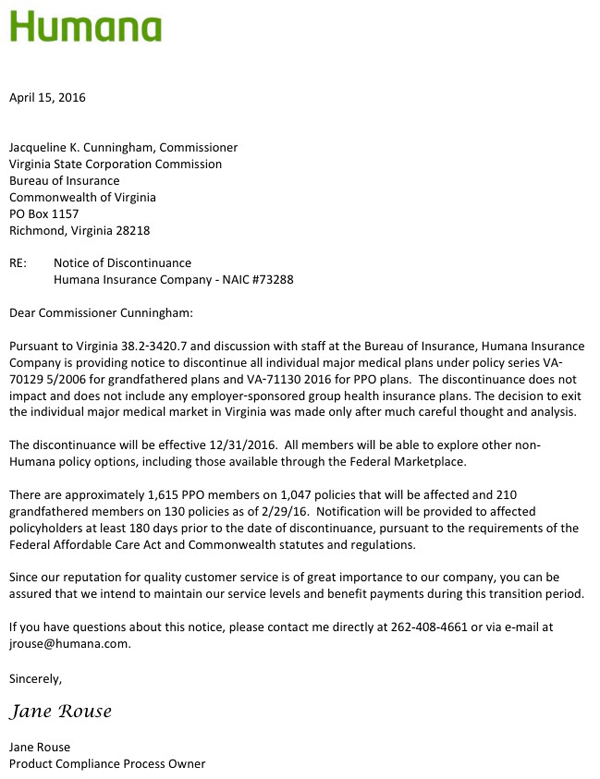

It's also worth noting that "grandfathered" enrollees only make up around 11% of Humana's total Virginia individual market as of this spring, which is somewhat higher than my overall ballpark estimate of around 1 million nationally.