The Washington Insurance Commissioner just issued the following press release. On the surface, it looks straightforward: 13.5% avg. requested, 13.1% approved. However, it's more complicated than that, because that 13.1% figure only applies to fewer than half of the plans (46 out of 98). The other 52 are still being reviewed:

OLYMPIA, Wash. – The Office of the Insurance Commissioner (OIC) has approved 46 individual health plans from seven insurers who will offer them in the Exchange, Wahealthplanfinder (www.wahealthplanfinder.org), for sale in 2017. The Washington Health Benefit Exchange Board is scheduled to certify the approved insurers and their plans at its board meeting later today.

Regence Blueshield also filed 21 plans for sale in the Exchange and Bridgespan filed 31 plans. Both companies’ filings and rates are still under review. They must be approved by the OIC before they can be considered for certification by the Exchange.

WARNING: This is a pretty long, wonky, number-crunchy post...if you want to skip to the point of it about 2/3 down, click here.

Yesterday I posted an extensive entry in which I reiterated, with a substantial amount of hard data (h/t to Bob Laszewski & Steve Davis) to back me up, that the off exchange individual health insurance market is consdierably larger than many pundits, reporters, politicians and policy wonks seem willing to admit; in fact, it appears to make up around 36% of the ACA-compliant indy market if you include grandfathered/transitional plans, or around 40% if you don't include them.

Arizona’s Pinal County Gains Health-Law Exchange Insurer

Blue Cross Blue Shield of Arizona will offer plans on the Affordable Care Act exchange in Arizona’s Pinal County next year, resolving a situation that drew a national spotlight because it represented a major challenge to the mechanics of the health law.

When Aetna Inc. announced last month that it would withdraw from the exchange in Arizona, among other states, it left Pinal at risk of becoming the first U.S. county without a single insurer selling exchange plans. Aetna had been expected to sell exchange plans in Pinal County, where approximately 10,000 people had signed up for ACA plans.

Given all the ugly ACA-related news over the past month or so (carriers dropping out of markets, average rate hikes going up significantly), it's important to remember the positive impact of the law as well...and today's early release of the latest National Health Interview Survey is very, very good news indeed:

Whenever Gallup releases their quarterly survey re. uninsured rates, I always make sure to note that as accurate as their methods may be in other ways, one major flaw of Gallup's methodology is that they don't include children under 18 whatsoever. This is no small gap, either, since a) children make up about 1/4 of the total population and b) children have historically had a significantly lower uninsured rate than adults (thanks, in no small part, to the Children's Health Insurance Program, spearheaded by Hillary Clinton, I might add). The NHIS, however, includes everyone...and breaks the data out in a whole mess of different ways. Here's what they have to say; note that all data from this survey was as of January - March 2016, so any changes since then (like, say, Louisiana expanding Medicaid to over 278,000 people) is not reflected in it yet):

In the first 3 months of 2016, 27.3 million (8.6%) persons of all ages were uninsured at the time of interview—1.3 million fewer persons than in 2015 and 21.3 million fewer persons than in 2010.

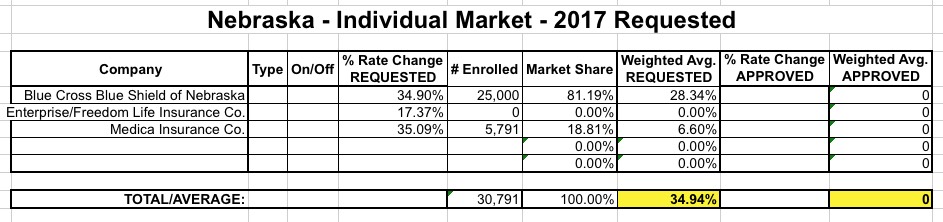

Huh. Back in June, when I first ran the requested rate hike numbers for Nebraska, it looked as though there were only two real carriers offering individual plans, either on or off the exchange: Blue Cross Blue Shield and Medica. UnitedHealthcare announced they were leaving NE along with a bunch of other states, and Coventry (aka Aetna) didn't have any filings for 2017, so I assumed they were bailing as well. Finally, the less time spent talking about "Enterprise/Freedom Life" the better. So...it looked like BCBS and Medica were it. Here's what the table looked like:

For 2 1/2 years, dating back to around February 2014, I've been trying to hammer home the importance of the OFF-exchange individual market. Time and time again I've been stunned at the seeming blind spot that people who should know better (such as Avik Roy) have regarding the millions of people who are enrolled in fully ACA-compliant policies, but are doing so directly through the carriers themselves. There are a few reasons why people buying individual/family policies would do this, but the most obvious one is simple: If you earn more than 400% of the Federal Poverty Level (around 97,000/year for a family of 4), there's no reason to jump through the extra hoops of enrolling through HealthCare.Gov or the other various ACA exchanges...because you don't qualify for federal financial assistance anyway. For whatever reason, however, numerous reporters, pundits and even the HHS Dept. itself keep acting as though this market doesn't exist.

The Connecticut average requested rate hike has jumped around a lot over the summer. It started out at roughly 21.3% back in June, then increased to 22.2% after the HealthyCT Co-Op announced they were closing up shop. Then, several of the carriers submitted revised rate hike requests, bumping the average up further to around 26.8%.

Well, over the holiday weekend, the CT Mirror reports that the CT Dept. of Insurance released their response to the requests. There were also yet more last-minute filing changes. I've updated the spreadsheet with both the final requests as well as the approvals...but there are a copule of major blank spaces I still have to fill in:

Most Connecticut health insurance plans sold through individual and small group markets will undergo steep rate hikes next year, although in some cases, the prices will not go up by as much as carriers had sought.

When I last crunched the numbers for the 2017 individual market in Arizona, the average requested rate hike statewide was a whopping 68%. However, that was before Aetna dropped their bombshell about dropping out of the exchanges in 11 states (AZ included), leaving about 6,400 residents receiving ACA tax credits in Pinal County with no subsidized policy options whatsoever.

Since Aetna had intended on requesting a jaw-dropping 85.8% average rate hike if they had stuck around, this technically meant that the average requested hike for the other carriers would have dropped somewhat, although this would be limited by Aetna only having about 7% of the individual market in the state.

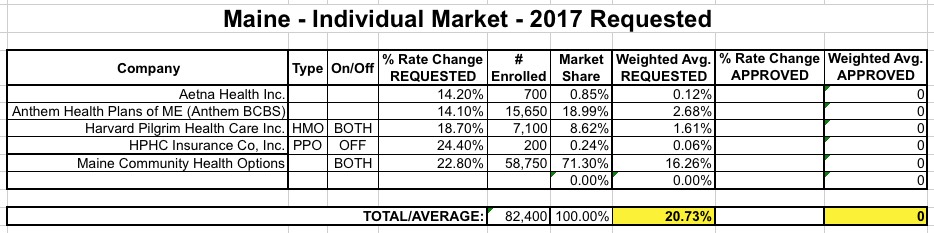

Since then there have been two major changes: First, Aetna, which had been planning on entering the Maine ACA exchange, infamously pulled a complete 180 and not only decided not to expand, but actually pulled out of the exchange in most of the states they're already in. This doesn't really impact Maine since they were only available off-exchange anyway. The second change does, however: Several of the carriers submitted revised requests, pushing the average up higher, to 23.9%.

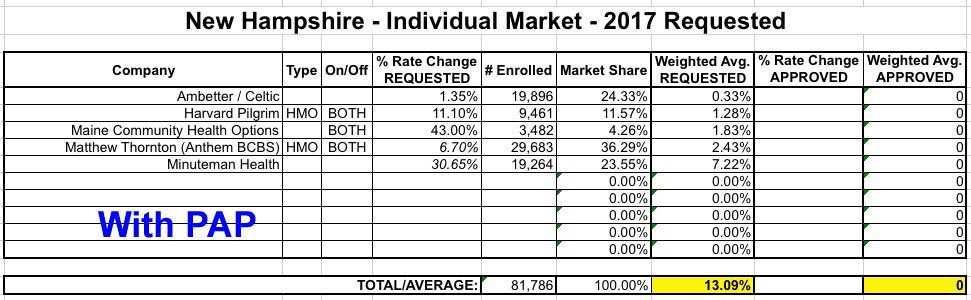

Community Health Options, a Lewiston-based health insurance cooperative, has gotten approval to withdraw from the New Hampshire insurance market in 2017.

The plan was approved this week by the Maine Bureau of Insurance, which has been monitoring CHO’s finances as it tries to recover from a $31 million loss in 2015. The nonprofit cooperative has set aside more than $45 million in reserves to try to avoid another big loss this year.