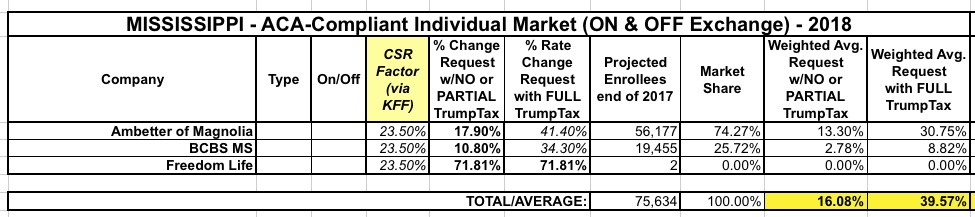

There's only two carriers participating in Mississippi's individual market next year (plus Freedom Life, which once again is just a shell company here). They're asking for 16.1% average rate hikes, and since there's no mention in any of the filings about CSR payments not being made or the mandate not being enforced, I'm assuming that increase doesn't account for those factors.

Massachusetts has one of the stablest statewide insurance markets, no doubt in large part due to their having instituted the precursor to the ACA, "RomneyCare", 4 years earlier. Massachusetts also merged their small business and individual market risk pools, which helps stabilize things. As a result, they have a high number of carriers participating in their ACA exchange and are among the few states with single-digit average rate hikes...assuming CSR payments are forthcoming and the individual mandate is properly enforced.

Assuming CSR payments aren't made, I used the Kaiser Family Foundation's 19% average estimate for Silver plan hikes due to the CSR factor. Since a whopping 92% of MA's exchange enrollees chose Silver plans (it looks like MA's unique "ConnectorCare" plans are considered Silver as well), that means an average CSR factor of around 17.5 points across the entire individual market.

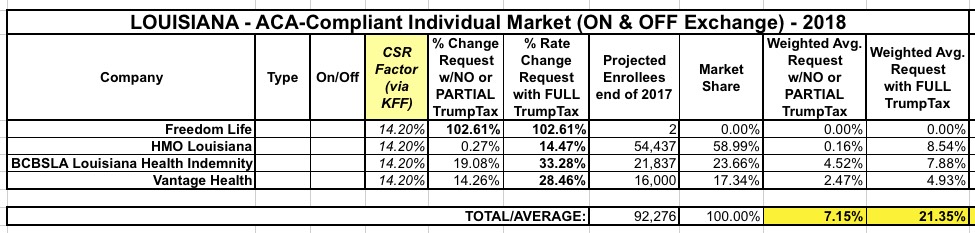

Louisiana has 3 individual market carriers for 2018 (technically there's 4, but "Freedom Life" is basically just a shell company with a placeholder filing). Officially, they're requesting average rate increases averaging around 21.4%...but all three carriers state point-blank in their filing letters that a huge chunk of their request is due specifically to the CSR reimbursement and mandate enforcement issues. The Kaiser Family Foundation estimates the CSR issue alone adds around 20 points to Silver plans, and 71% of Louisiana exchange enrollees chose Silver, so that translatest into roughly 14.2 points across the whole market. This results in just a 7.2% average rate hike if CSR payments are made vs. 21.4% if they aren't:

I SCREWED UP ROYALLY. Instead of making a few simple corrections, I've chosen to completely rewrite this entry. My apologies for the error; full explanation and corrected data analysis below.

Longtime readers know that in addition to the core function of this site (it's right there in the title above), I'm also obsessed with tracking and breaking down the off-exchange individual market. This is easier said than done, because every state except for DC (which isn't actually a state) allows people to continue to purchase individual market policies directly through the insurance carriers...and unlike exchange-based enrollment, off-exchange enrollments don't usually have to be reported publicly. Some states require them to do so as part of internal state regulations, but they're usually a pain to get ahold of and other states protect the data as trade secrets, etc.

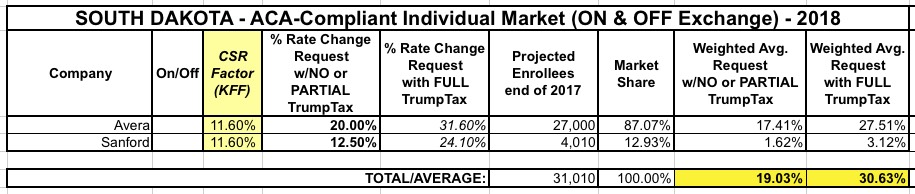

South Dakota is another fairly straightforward state: Two carriers, around 31,000 total ACA-compliant enrollees on & off exchange. Neither filing indicates whether they're assuming CSR payments will be made or not, so I'm assuming they're based on them being paid.

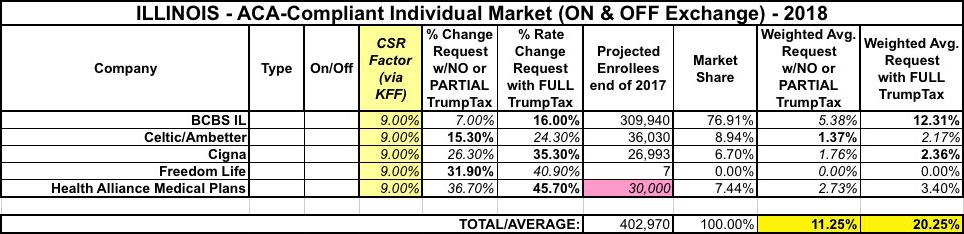

Another major state: Illinois. I've decided to scrap the "Low/High Increase" columns since they just confused people and made the table too wide, but replaced them with a new column showing the CSR factor estimate according to the Kaiser Family Foundation. Note that the percent listed will be smaller than Kaiser's estimate for each state, because their numbers only apply to silver plans, not all metal levels.

For instance in Illinois, Kaiser estimates that carriers would have to raise rates by 14% on Silver plans to cover their CSR losses. However, only 64% of Illinois exchange enrollees have silver plans to begin with, so I'm only plugging in about 9%. There are 5 carriers operating on the Illinois individual market (well, really 4, since "Freedom Life" doesn't count). I have the hard enrollment numbers for 4 of the 5; for Health Alliance Medical Plans I used 30,000 based on their 2016 number. Overall, Illinois is looking at around 11.3% w/partial sabotage, 20.3% with full sabotage:

Hawaii only has two carriers on the individual market (and in fact doesn't even have much of an individual market due to a state law mandating that nearly every business provide coverage anyway). HMSA's filing letter is very specific about calling out both the CSR and mandate enforcement sabotage factors as being part of their request. Kaiser doesn't really mention either issue at all, and the only CSR reference in the filing seemed to assume it would be paid, so I have one in each category. Kaiser Family Foundation assumes a 21% Silver CSR rate hike, and 71% of Hawaii's exchange enrollees are on Silver plans, so that amounts to roughly a 15% overall CSR factor.

Here's what it looks like...15.2% w/partial sabotage, 30.2% with full sabotage:

Whew! OK, Texas was a bear for obvious reasons...13 different carriers (well, 12 really...Centene is new to their market). Several more are dropping out (Aetna, Allegian, Cigna, Humana, Memorial Hermann and Prominence), but suposedly theyonly have around 64,000 enrollees in TX combined. Texas's total individual market is actually closer to 1.6 million, so I'm obvoiusly missing a big chunk of enrollees below (and before my regular commenters say it: Yes, I'm sure the off-exchange TX indy market has shrunk this year, but I find it hard to believe it's shrunk by over 60% already).

Anyway, I've managed to plug in one hard request percent for each carrier--the FULL Trump Tax for 3 of them, the NO/PARTIAL Trump Tax for most. In Vista's case, they're off-exchange only so the CSR issue isn't a factor anyway. Unfortunately, I can't seem to find the enrollment number for Community Health Choice, so I don't know what their share of the market is, which could make a big difference if they have high enrollment. I've plugged in a flat 100,000 enrollees for the moment, but will change that if I'm able to track the actual number down.

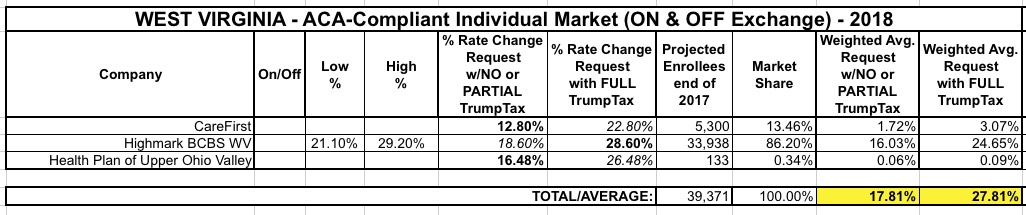

Another fairly straightfoward state: Three carriers, two of which (CareFirst and Health Plan of Upper Ohio Valley) appear to be assuming CSR payments will be paid; the third, Highmark BCBS (which holds the vast bulk of the individual market) openly states that they assume they won't be made and that the mandate won't be enforced to boot. I'm once again assuming roughly 2/3 of Kaiser Family Foundation's "Silver CSR hike", which in this case would be about 10%, giving the following: 17.8% if CSR payments are made, 27.8% if they are:

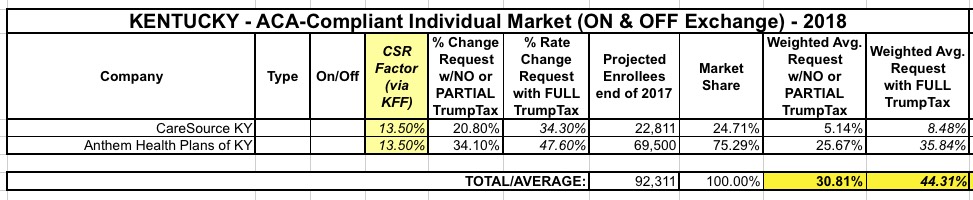

Louise Norris gave me a heads up that the Kentucky Insurance Dept. has posted their 2018 rate hike filings as well. The individual market is pretty straightforward...and pretty grim: Both individual market carriers, CareSource and Anthem, are asking for pretty steep rate hikes even if CSR payments are locked in next year, averaging around 30.8%, while assuming another 13.5 points on top of that (71% of Kaiser's 19% Silver average) would bring the average up to around 44.3%. Not much else to say about this one for the moment.