As regular readers know, I've spent the past few months speaking at various political/activist club meetings giving a lengthy presentation which gives a basic overview of the healthcare coverage situation in America, how the ACA was supposed to work, which parts of it are/aren't working, how I think the parts which aren't working should be fixed/improved, and of course what the Republican Party's plan of the day is to screw up everything which works while making the existing problems far, far worse.

By popular demand, I've embarked on a project to bring a version of this presentation to the web, by way of a series of short, simple videos (narrated slideshows, really) which give the basics. The first one can be viewed above.

As I note at the outset: I realize how incredibly basic and crude this is. I actually have some experience in video editing from my wannabe film producer days (long story, don't ask) in the 1990's, but I'm more than a little rusty at it...and frankly, given that the Senate vote is coming up in just a few days, I don't exactly have a lot of time for fancy effects and the like.

NOTE: The original focus of this diary was on the deliberate sabotage by the Trump Administration/HHS Dept. under Tom Price of the individual insurance market in general and HealthCare.Gov in particular, but the screen shot mentioned in passing in the diary below is actually far more important and disturbing the more I think about it than I had originally thought.

As noted below, it's an anonymous note sent to me on Thursday. Since it was sent I’ve confirmed the identity of the sender. This doesn’t prove that their specific claim is true, but there’s absolutely no reason I can think of for this person to risk their job and reputation by lying about this issue, and it matches everything else in the diary.

Several professional journalists have since contacted me and I’ve gotten them in touch with the sender. Stay tuned, this could be a big deal.

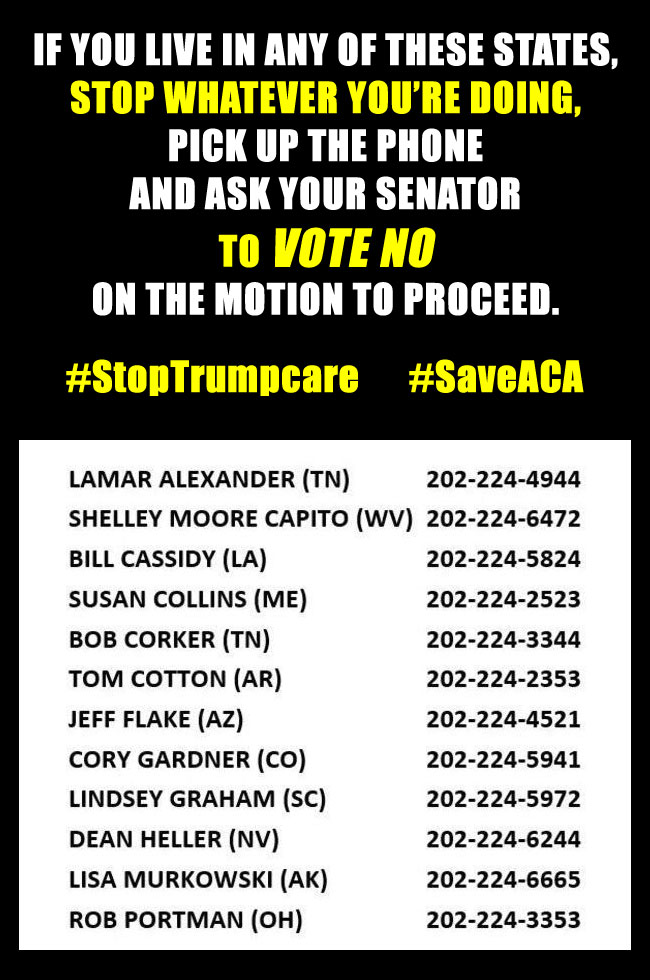

(sigh) I'm not really sure what the point of even writing about this is since it doesn't include the Cruz-Lee amendment which is supposedly the only thing keeping the ultra-conservative wing of the GOP Senate on board with BCRAP in the first place, but whatever:

CBO and the staff of the Joint Committee on Taxation (JCT) have prepared an estimate of the direct spending and revenue effects of the version of H.R. 1628, the Better Care Reconciliation Act, posted today on the Senate Budget Committee’s website.

By the agencies’ estimates, this legislation would lower the federal budget deficit by reducing spending for Medicaid and subsidies for nongroup health insurance. Those effects would be partially offset by the effects of provisions not directly related to health insurance coverage (mainly reductions in taxes), the repeal of penalties on employers that do not offer insurance and on people who do not purchase insurance, and spending to reduce premiums and for other purposes.

“The idea that you can repeal the Affordable Care Act with a two- or three-year transition period and not create market chaos is a total fantasy,” said Sabrina Corlette, a professor at the Health Policy Institute of Georgetown University. “Insurers need to know the rules of the road in order to develop plans and set premiums.”

But actually, he thought as he re-adjusted the Ministry of Plenty’s figures, it was not even forgery. It was merely the substitution of one piece of nonsense for another. Most of the material that you were dealing with had no connexion with anything in the real world, not even the kind of connexion that is contained in a direct lie. Statistics were just as much a fantasy in their original version as in their rectified version. A great deal of the time you were expected to make them up out of your head.

According to Trump's CMS division, the average unsubsidized premium for federal ACA exchange policies (ie, 39 states on HealthCare.Gov) in 2017 is $476/month.

Across the 21 states I've compiled data for so far, the average requested rate increase for ACA-coimpliant individual market policies in 2018 is around 34%.

Of that 34%, roughly 19% of it on average is due specifically to concerns that Cost Sharing Reduction reimbursements won't be made by the Trump administration next year.

Thanks to Emily Gee and the Center for American Progress for this:

This isn't a full/official New Jersey rate hike update, as it only refers to one carrier, and rounds things off a bit, but in the video above, if you watch from around 37:30 to 41:00, you'll hear New Jersey Congressman Frank Pallone talk about the negative impact that the CSR reimbursement threat/uncertainty/sabotage effect is having on Horizon Blue Cross Blue Shield...and since Horizon BCBS happens to hold something like 70% of the New Jersey individual market share (which is confirmed by Pallone in the video), the statewide weighted average rate hike will end up being largely determined by theirs.

The most relevant part:

"So Horizon, which is something like 70% of our market in New Jersey, filed like a 24% increase. And I asked the president (of Horizon) "why are you filing with a 24% increase?" I can't imagine that health insurance costs have gone up that much. And he said "Oh, they haven't, Congressman." I said, "well, what is this?"