Last year I assumed, for months, that once March 31st came and went, I'd be free to close up shop. Then they tacked on the 2-week "extension period". Then a whole mess of other stuff happened, and, well, here I am, still chugging along almost 10 months later. This year, however, I was operating on the assumption that once February 15th came along, I'd be able to pull the plug (not saying that I would, just that I'd be free to do so if I wished). However...

Open Enrollment ends February 15. As a retail tax preparer, I'm flummoxed by this. We're barely beginning to see clients--the first ones with nothing but a W-2 are just trickling in the door.

There's several ways of measuring the performance of the states. You could go by sheer number of enrollees, but that's obviously unfair given the massive population differences between them. You can go by enrollments relative to their total population...except that some states have a much higher uninsured population than others, along with huge variations in average income, unemployment and a host of other variables.

In the end, I'm comparing the states across 4 different benchmarks:

1. How they're performing relative to last year's Open Enrollment Period

2. How they're performing relative to the "official" 2015 Open Enrollment Period targets put out by either the HHS Dept. (or the state government/exchange representative in some cases)

3. How they're performing relative to my 2015 Open Enrollment Period targets, and

4. How they're performing relative to the total potential exchange QHP enrollees.

This press release from the Washington exchange about tax credits for 2014 ACA enrollees isn't an official enrollment update, but they do include a rough update about 2/3 of the way down the text:

As of Jan. 25, more than 127,000 residents have enrolled in Qualified Health Plans for 2015 coverage, with approximately 40,000 of those customers signing up for the first time through Washington Healthplanfinder.

127K is about 10K more than they had enrolled as of January 17, or around 1,250/day. At that rate, they'd be likely to add another 26K by 2/15, for 153K total, which would be far short of the 215K that they're targeting (and way short of the 250K I was anticipating for WA). A decent mid-February surge should bring them up to around 175K, and a full surge could max out at 200K even. It's conceivable that they'll even squeak by their own target, but I don't see any way of reaching my own target.

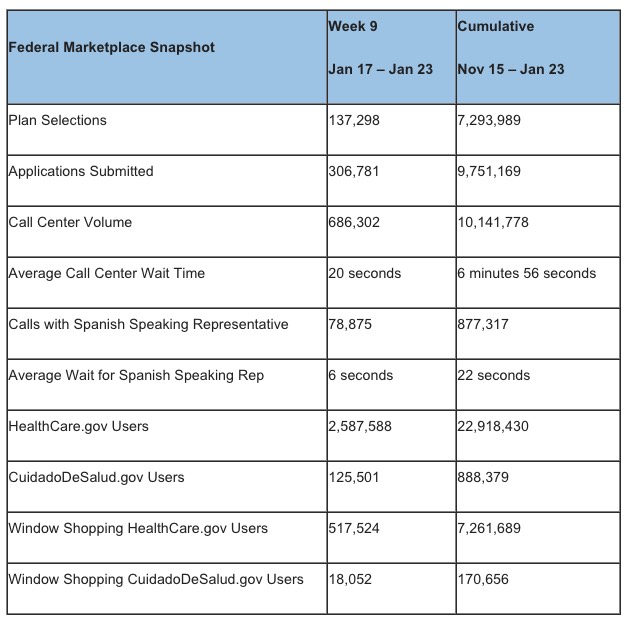

The last 4 weekly HC.gov reports saw 96K (Christmas), 103K (New Year's), 163K (nothing significant) and 400K(the February coverage deadline for most states) on the federal exchange.

With the 1/15 deadline out of the way, the past week (and the next two) should come in somewhere between the last two: Fairly quiet, but steady and not completely dead. I'm assuming roughly 30K/day on HC.gov (around 40K/day nationally), which should have brought the total on HealthCare.Gov up to around 7.36 million as of Friday, January 23rd.

Whoops. Only 137K for the week; I overshot the mark significantly (off by 53% for the week, or about 0.9% cumulatively). The post-deadline drop-off was more significant than I figured. Crud.

As of January 17th, Rhode Island had enrolled about 28.8K people in private plans for 2015, or around 78% of their "official" target (based on the HHS Dept's "30% higher than last year" target).

RENEWAL UPDATE* As of January 24, 2015, 79% of Year One customers have renewed (selected a plan) for 2015 (75% of renewing customers paid the first month’s premium).

Total New Customers: 7,862 (6,539 paid)

Total Renewed Customers: 20,283 (19,189 paid) Total HealthSource RI enrollments for 2015 coverage: 28,145 (25,728 paid)

Hey, cool! That's a 91% payment rate! Um...except for one thing...somehow they've lost 644 people? Oh, wait...

This morning I noted several new developments in the ongoing King v. Burwell saga (formerly Halbig v. Burwell...and yes, I know that's technically a separate case, but cut me some slack here). However, I forgot a couple more:

Here's a list of people who--to the best of my knowledge--have now been proven not to ever have the slightest inkling, hint, suggestion or thought that federal tax subsidies weren't supposed to go to states which didn't establish their own ACA exchanges at any point throughout the many-year process of the law being crafted, drafted, printed, read, debated, argued about, voted on or signed into law:

Now, technically speaking, that exact number isn't precisely what it was as of January 16, because it includes 1 extra day for 13 of the state exchanges and 2 extra days for California. I have no clue why they did it that way, but whatever. Really, though, enrollment dropped off dramatically for a few days after the 15th, because that was the February-start deadline in 46 states +DC (including California), so I don't imagine more than 10-15,000 of this came in on the 17th or 18th.

Since the day I started this project (before it, really), I've been asking for the HHS Dept. to simply release the enrollment data in as much detail as possible on a frequent basis...and by frequent, I didn't mean "monthly"; that's far too long given the 24-hour, 24-second news and political cycle. For 7 months, the HHS Dept. ignored this plea, followed by another 6 months of not just ignoring it but actually going backwards on enrollment data (ie, cutting off even the monthly reports during the off-season). Fortunately, since November, they've done a total 180, issuing not only "weekly snapshot" reports giving the overall HC.gov enrollment numbers, but more recently breaking these down by all 37 states on a weekly basis. This is awesome!

Remember all last summer and into the fall when I kept pointing out to anyone who would listen that just because the official Open Enrollment period had ended back on March 30th (or April 15th, depending on your POV), there were still a good 9,000+ people per day enrolling via the ACA exchanges due to major life changes?

Of course, those people being added were also being cancelled out to some degree by people dropping their policies (or being dropped whether they liked it or not due to non-payment or immigration/residency issues). From what I could tell, the additions seemed to be outnumbering the subtractions for most of the summer, up until around August, at which point the trend reversed. However, it was difficult to know this for certain until the CMS head unexpectedly mentioned that 7.3 million people were still enrolled as of mid-August (going up!), followed by a drop to 7.1 million as of mid-October (going down!).

Here in Michigan, the official estimates of how many residents are eligible for ACA Medicaid expansion ranged from around 477K to 500K, and over the past month or so, the weekly reports from the official MI Dept. of Community Health "Healthy Michigan" website has pegged the current enrollment total at between 490K - 510K. This led me to assume, naturally, that the program has been essentially tapped out, with close to 100% of those eligible already having signed up within the first 10 months.

Yesterday, however, they posted the weekly update again, and guess what?

Healthy Michigan Plan Enrollment Statistics

Beneficiaries with Healthy Michigan Plan Coverage: 533,110

(Includes beneficiaries enrolled in health plans and beneficiaries not required to enroll in a health plan.)

*Statistics as of January 26, 2015

*Updated every Monday at 3 p.m.

Wow. 533,000 people. So, what's going on here? Well, possibilities include: