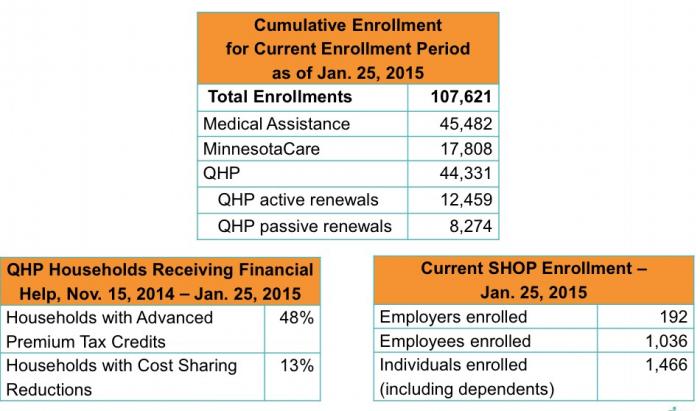

Huh. The actual QHP numbers are fine--that is, Minnesota is still lagging behind where they should be, but they've added 201 over the past couple of days, which is fine given that we're in the slowest part of the enrollment period.

However...what's going on in the lower-left? "Advanced Premium Tax Credits" is the government-ese name for "Tax Subsidies'. In most states they're averaging somewhere between 80-90%...yet in Minnesota, it's less than 50%? What's up with that?

Let's suppose that the Supreme Court, against all logic, legal precedent, reason and decency, does end up ruling in favor of the plaintiffs in the King v. Burwell case and does indeed stop any federal tax credits/subsidies from being provided to people in states which are being run through the federal ACA exchange instead of their own. Let us further assume that this ruling does come out sometime in mid-June, 2015.

Let us further assume that the Republican-held Congress, being the colossal dicks that they are, do not take any action whatsoever--or, more likely, vote on a bill which would fix the "...state exchange" problem but would also have a completely unacceptable poison pill attached (ie, removing the individual mandate altogether, or killing the 80/20 medical loss ratio, or allowing insurance companies to deny coverage based on pre-existing conditions...you get the idea).

Here we go: The Massachusetts Health Connector has issued their weekly report, which confirms 113,887 QHP selections through last night, with 83% of those having paid their first month's premium and thus being fully enrolled. As I projected last week, the overall payment rate has risen by another 7%, and will likely continue to do so (of course, it will then "drop off" again dramatically during the final February surge, only to shoot back up again over the next few weeks as March enrollees start paying up).

Given the official 9.5 million confirmation a few days ago, this isn't going to be as surprising as it might otherwise have been, but it's still an important milestone which should be noted. I was originally estimating that total QHP selections would cross the 10 million mark last night, but after some tweaks I've adjusted this a bit, and am now estimating that we'll cross the 10 Million ACA Exchange-Based QHP Selection total on Saturday, January 31st.

(As a reference point for next Wednesday's "weekly snapshot", I'm also calling for today's HC.gov total to hit 7.45 million).

After that, we're into the February home stretch, which I'm expecting to play out roughly as follows:

Around 10.2 million by February 6th (35K/day)

Around 10.5 million by February 10th (65K/day)

And for the final 5 days, I'm expecting another major "Apple Store"-like surge: An average of 400,000 people per day for 5 days straight, for 12.5 million as of midnight, Feb. 15th.

If you get sick, America, the Republican health care plan is this: "Die quickly." That’s right. The Republicans want you to die quickly if you get sick."

...Consider this question: Should society have as its goal that the government prevents all deaths from any health-related ailment other than natural causes associated with ripe old age? The notion is absurd — to both conservatives and liberals. There are limits to the proper amount of scarce resources, funded by taxpayers, that Washington should redirect toward health care.

So, Mitt Romney, who spearheaded the original version of the Affordable Care Act (aka Obamacare) in Massachusetts a decade ago, and then ran for President on a platform of repealing essentially the same law implemented nationally that he pushed through at the state level, has decided to run for President again.

Some 3 million to 6 million Americans will have to pay an Obamacare tax penalty for not having health insurance last year, Treasury officials said Wednesday. It's the first time they have given estimates for how many people will be subject to a fine.

The penalty is $95, or 1% of income above a certain threshold (roughly $20,000 for a couple). So you could end up owing the IRS a lot of money.

Take a married couple with $100,000 in income - their bill comes to $797, according to the Tax Policy Center ACA penalty calculator.

The penalty for remaining uninsured rises to the larger of $325 or 2% of income in 2015.

OK, this is just an overview of the upcoming tax penalty. Nothing noteworthy. However...

Still, the good news is that it looks as though a certain segment of people have finally started to smarten up; perhaps it was last fall's Ebola panic, because this shift happened before the measles outbreak:

The number of California parents who cite personal beliefs in refusing to vaccinate their kindergartners dropped in 2014 for the first time in a dozen years, according to a Times data analysis.

...Statewide, the rate of vaccine waivers for kindergartners entering school in the fall declined to 2.5% in 2014 from 3.1% in 2013. Bigger declines were seen in districts with some of the larger vaccine exemption rates.

Recalcitrant red states have done little — or nothing — to promote Obamacare. Yet their residents are getting health coverage by the millions.

Across the country, efforts to resist or undermine the law persist. Calls for repeal haven’t died down. Most of the states with Republicans in control aren’t running their own insurance exchanges, but their residents are still getting covered and still getting subsidies — unless the Supreme Court in an upcoming case rules that the subsidies are illegal in states using HealthCare.gov.

Fewer workers received employer-sponsored health coverage after the Great Recession than they did before, but don’t put the blame squarely on the Affordable Care Act, a study released Thursday says.

However, I just realized that they also threw in a new QHP enrollee update:

In addition, Lee reported Wednesday that as of Jan. 26, 273,111 consumers had picked a plan during open enrollment.

Add that to the 944K renewals and you have a grand total of 1,217,111 through 1/26.

That's an increase of 44,345 since January 12, or 3,167/day. Of course, this also includes the January 15th deadline, so it doesn't tell me much about the next week or so. For that, I'd have to look at the increase since 1/18 (1,200,427), which is just 16,684, or 2,085/day.