The last 4 weekly HC.gov reports saw 96K (Christmas), 103K (New Year's), 163K (nothing significant) and 400K (the February coverage deadline for most states) on the federal exchange.

With the 1/15 deadline out of the way, the past week (and the next two) should come in somewhere between the last two: Fairly quiet, but steady and not completely dead. I'm assuming roughly 30K/day on HC.gov (around 40K/day nationally), which should have brought the total on HealthCare.Gov up to around 7.36 million as of Friday, January 23rd (around 210K for the week).

Now, here's the thing: We're 1/3 of the way through what should be a fairly consistent 3-week period before the final rush kicks in around February 9th/10th. My guess is that whatever the tally was this past week should stay pretty close for the next 2 weeks as well...so if the past week turns out to be higher (say, 250K), the following 2 weeks should each hit that number or higher as well. I'm estimating that the national total should reach the HHS's target (10.4 million) around February 6th.

No, I'm not gonna go into a "Dental Gate"-style rant against the HHS Dept. about this. Without knowing more details about the information in question or how it's being used, this may be another "nontroversy". Even so, it strikes me as being a bit of an unforced error on the part of the administration:

The government's health insurance website is quietly sending consumers' personal data to private companies that specialize in advertising and analyzing Internet data for performance and marketing,The Associated Press has learned.

The scope of what is disclosed or how it might be used was not immediately clear, but it can include age, income, ZIP code, whether a person smokes, and if a person is pregnant. It can include a computer's Internet address, which can identify a person's name or address when combined with other information collected by sophisticated online marketing or advertising firms.

A few days ago, I posted an article over at healthinsurance.org which delved into the mysterious world of OFF-exchange QHPs...ie, people who just enroll in a private, individual/family healthcare policy the old-fashioned way, by contacting Blue Cross, Aetna, UnitedHealthCare or whoever directly instead of going through one of the ACA exchange websites.

I also posted an accompanying piece here which noted how hard it is to lock down these enrollment numbers, since the carriers aren't generally required to provide that information publicly except in a general sort of way (and even then, usually only once a year or so). Only Oregon and Washington State really post off-exchange data with any sort of frequency, and only Oregon is doing so weekly.

OK, that's 92,886 QHPs total, or 208/day since the December 15th deadline. At that rate, they'll likely add a minimum of 5,000 more by 2/15 if there's no mid-February surge; more likely they'll add between 10-15K more, for a total of perhaps 108K at the outside, just barely hitting the HHS Dept's target (107K), but coming up short of mine (130K)...but we'll have to see...

MNsure will release 2015 enrollment metrics weekly, and will present a more robust metrics summary to the MNsure Board of Directors at each regularly-scheduled board meeting. During weeks that MNsure is closed on Friday, the enrollment metrics update will be released earlier in the week.

Health Coverage Type Cumulative Enrollments

Medical Assistance 44,308

MinnesotaCare 17,506 Qualified Health Plan (QHP) 44,130

TOTAL 105,944

* (actually as of 1/22)

OK, let's see here...that's exactly 400 more QHP enrollees since 1/19, or 133/day, although they've averaged 194/day since New Year's Eve.

At that rate (with no mid-February bump), they'll add another 4,600 by 2/15, or 49K, well short of their target of 67K. However, it's more likely to be more like double or even triple that when you include the final surge, for a total of perhaps 58,000 or so. Reaching their internal target may still be feasible; reaching mine (75K) seems very unlikely at this point, but anything's possible.

As of Jan. 22, 185,199 Marylanders have enrolled in quality, affordable health coverage for calendar year 2015, since the 90-day open enrollment period began Nov. 15. That includes 93,806 people enrolled in private Qualified Health Plans (QHP) and 91,393 people enrolled in Medicaid.

As of Jan. 21, the total number of Medicaid and MCHP enrollment is 1,281,999. Compared to Dec. 31, 2013, the net change in Medicaid enrollment as of Jan. 21, 2015 is +241,337. This figure takes into account that individuals lose Medicaid coverage because of changes in household, age and income, as well as redeterminations.

OK, that's 2,669 in 11 days, or 242/day. This is down substantially from the prior week or so, but it includes the days leading up to and following the 1/15 deadline for February coverage (when they'd drop off again), so that doesn't really mean much.

This is an incredibly depressing post for me to write. Last month I received word that CoOportunity Health, one of the 23 co-ops set up as part of the ACA to offer competition with the Big Boys, had run into serious financial trouble and was being yanked off of Healthcare.Gov (they were operating in Iowa and Nebraska, both of which are on the federal exchange).

Anyway, as of December 10th, my contact at CoOportunity was unaware of any issues; they reported that everything was going great. On Christmas Eve, I was tipped off about CMS dropping CoOportunity from the exchange completely, but there wasn't a whole lot of detail given as to what had gone wrong beyond vague references to quarterly financial statements, cash flow and annual audits.

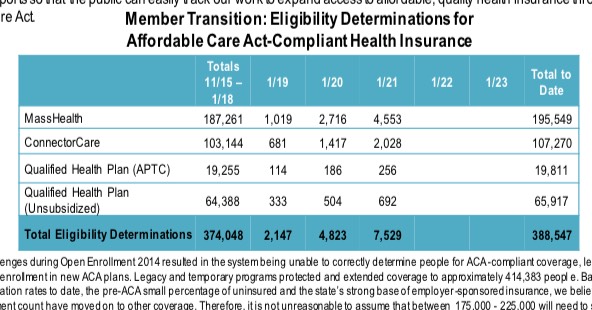

And there you have it: As I've been expecting all week, not only has the MA Health Connector broken the 100K milestone, they blew past it, with 108,051 private policy selections as of last night (the Medicaid number is still hovering just below 200K, but that doesn't include yesterday; they should have easily tacked on another 5,000 to put MassHealth over the top).

In addition, the overall payment rate continues to climb, reaching 76%...but likely much higher when you consider that about many of the 108,000 total aren't scheduled to have their policies kick in until February anyway. I know that at least 50K of those who paid were for January-start policies, so it could easily be something like: 50K paid / 57K (January) + 32.2K paid / 51K (February), which would mean 88% of the January enrollees are paid up + 63% of the February enrollees so far. The larger point is that we won't know the real payment rate until late March (over a month after the enrollment period itself ends), so there's nothing to worry about for now.

A few days ago I posted an article about how Rhode Island is having trouble scraping together the $19 million or so that they need to operate HealthSource RI, now that the federal funds have pretty much dried up and the exchange has to pull its own weight. Some exchanges were set up with a funding mechanism in place (generally by charging either the insurance companies operating on the exchange, or the enrollees themselves, some sort of tax or fee), but others, like Rhode Island, were funded with federal dollars but never got around to setting up a way to pay for themselves after that funding stopped.

Anyway, a Republican state legislator in RI came up with an ingenious solution: Dump the exchange, even though it's functioning perfectly well. The reasoning is that the federal exchange, Healthcare.Gov, is operating more efficiently, so why not just do what Oregon and Nevada had to do this year (due to technical problems) and add themselves to the pile of 3 dozen states already being run through HC.gov?

Today's update makes that even more clear: Another 2,976 QHP determinations likely means at least 1,300 more QHP selections, which should bring the total up to around 98,800 through last night. Another 1,200 today should put them over the top...and that's quite likely since the numbers should be ramping up further today (MA's February-start enrollment deadline is tomorrow).

For the record, this also means that Massachusetts has now officially enrolled 3x as many people in private policies as they did all of last year.

The Medicaid (MassHealth) side, meanwhile, isn't an estimate--those 195,549 people are enrolled immediately as I understand it. 4,500 more today and they've hit the 200K milestone.