OK, looks like my QHP estimate over the past week was fairly close, but a bit conservative...actual QHPs selected are up to nearly 119K, with just shy of 100K even having paid their first premium (thus completeing their enrollment).

100K / 119K = an 84% payment rate, but remember that anyone who has enrolled since 1/23 doesn't have to pay their first premium for over 2 weeks, so this isn't cause for concern.

Meanwhile, they have another 95,000 people who have been determined eligible for QHP selections waiting in the queue, of which nearly 6,000 have a plan in their shopping cart but just haven't pulled the trigger.

MA will have to have 51,274 more QHP selections to reach the 170K target (which, admittedly, was my interpretation of their target, not necessarily their target itself). That'd be 4,600/day, vs. the 1,447/day they've averaged so far.

In 1972, Harlan Ellison edited an anthology of sci-fi short stories called Again, Dangerous Visions (a sequel to "Dangerous Visions", naturally). One of the stories, by Edward Bryant, is called "The 10:00 Report Is Brought to You by..."

The premise of the story is a cynical, burnt-out TV news reporter who discovers, to his disgust, that the network that he's working for has figured out a foolproof way of getting exclusive coverage of breaking news stories...by creating them (and yes, a similar plot device was used in the James Bond film, Tomorrow Never Dies).

Specifically, the reporter discovers that the network has set up a bunch of remote camera units throughout a small town and then paid a local biker gang to actually invade the town and loot/pillage/terrorize the place, so that they'll have juicy, compelling live footage of actual arson, robbery and looting taking place.

The Washington State ACA exchange released updated 2015 enrollment numbers today, broken out by county, current through January 31st. They've even broken each county out between renewals from 2014 and new additions for 2015. The grand totals?

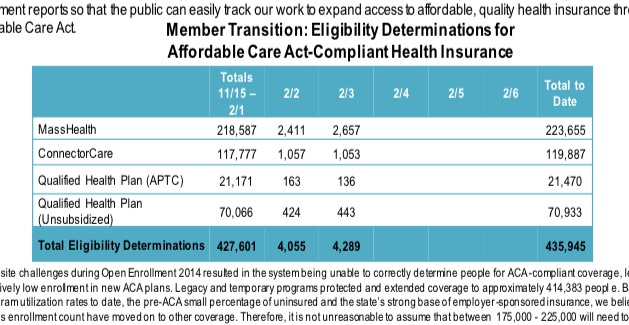

With yesterday's 1,737 QHP determinations, Massachusetts has likely tacked on another 800 QHPs or so, bringing them up to around 117.5K. In order to reach the 170K target I've estimated, they'll have to enroll about 52K in just 11 days, or a whopping 4,700/day.

I won't know until their weekly report tomorrow whether my "45% of determinations" ratio still stands. At this point the other half of the lingering QHP determinations should start to be kicking in...there's over 214K total; if 117.5K have already selected a plan, that means there's still another 96K people who have gone through about 2/3 of the process already; most of them should be coming back to complete the job now.

For comparison, in 2014, with their broken exchange system, they only averaged 158/day. For the current period, they averaged 1,950 through the January deadline (11/15 - 12/23), and 999/day during the February period (12/24 - 1/22), though that was missing the crucial deadline day of 1/23. Since then they seem to have averaged about 726/day, though that's mostly durign the slowest part of the enrollment period.

Regular readers know that I've been a bit obsessed with hunting down the Mysterious World of OFF-exchange QHPs®...enrollees in fully ACA-compliant individual policies which aren't run through the exchanges (ie, no tax credits), but directly through the insurance companies themselves (Blue Cross, Aetna, whatever).

As I noted in my recent piece for healthinsurance.org, last year off-exchange QHPs ended up being a bit higher than as on-exchange: Around 8 million, give or take. However, this was just a rough estimate patched together from various data points, and even then it's likely that some number of those were the so-called "grandfathered" plans (which can continue indefinitely until the enrollee dies or cancels/stops payment) or the "transitional" (aka "grandmothered") plans, which are the ones which were supposed to be discontinued on 12/31/13, but were given up to a 3-year extension period depending on the state and insurance company.

A couple of weeks ago, Maryland blew past the HHS Dept's target for the state (88K QHPs) and hit 94K as of 1/22. I noted that they were on their way towards easily hitting my personal, higher target of 105K by 2/15.

In response, a few days ago I went through all 50 states (+DC) and adjusted my own projections, lowering them in 9 states while bumping them up in 26 others, including Maryland. I tacked another 10K onto MD to 115,000 QHP selections. (Note that I'm leaving my original projections in the actual spreadsheets to avoid confusion; the revisions are more just to confirm that I recognized where the trendlines would be and where my earlier logic fails were).

I've slightly modified the State-Level Goals graph, with color-coded lines at 80% and 90% of the target numbers. As always, the blue lines represent the percent of the official HHS/State Exchange target achieved; the green lines represent the percent of my target achieved. In every state (except New York), the green line is shorter because my target is higher than the HHS/Exchange goal.

Important: The other day I lowered my personal targets for 9 states and raised them for 26 others. However, I'm not changing these on my actual spreadsheet or any of my graphs; I'm curious to see how far off my original targets end up being.

Massachusetts continues to crank along. 1,632 QHP determinations x 45% selecting a plan means they should have added another 700 or so QHPs yesterday, for a total of around 116,700 to date.

This isn't a formal press release, but according to NBC Connecticut, Access Health CT has enrolled "more than 96,000" people into Qualified Health Plans (QHPs). The article ran yesterday, so presumably the number is current as of February 2nd at the latest:

Connecticut residents signing up for health insurance through Access Health CT must enroll by Feb. 15 or face a potential tax penalty from the federal government.

"We're on track to hit our [enrollment] goals," said Access Health CT's acting CEO, Jim Wadleigh.

The state's health care marketplace aims to sign up 100,000 private citizens during the current enrollment period. With less than two weeks left, more than 96,000 residents have signed up for qualifying health plans.

About 30,000 of them are new sign-ups, Wadleigh said, adding that all avenues for enrollment have been successful.