Enrollment increased by 16% over last year – seventh annual increase in a row.

BALTIMORE (Jan. 17, 2025) – Nearly a quarter-million Marylanders enrolled for 2025 through Maryland Health Connection – a new record for the state-based health insurance marketplace.

A total of 247,243 enrolled during the open enrollment period that began Nov. 1, 2024 and ended Wednesday. That was up 16% from 213,895 enrollments one year ago. An additional roughly 150 people who were in line with the Maryland Health Connection call center at midnight Wednesday may be in the process of completing their enrollments this week.

This marked the seventh consecutive year of enrollment increases in the health insurance marketplace that Maryland established in 2013 following the passage of the Affordable Care

Act. Total enrollment is up 56% since the pandemic.

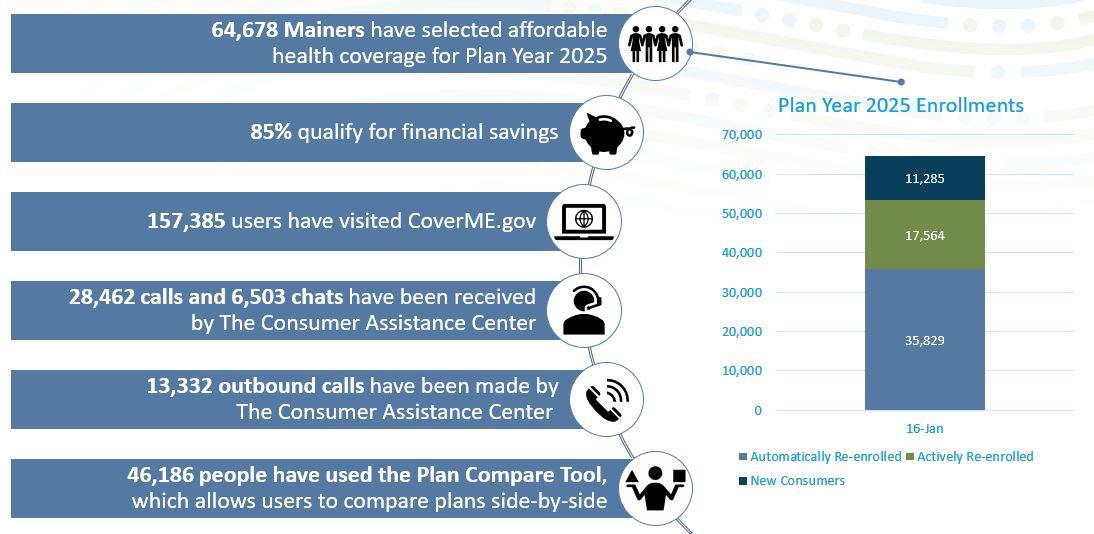

The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) will release biweekly updates on plan selections through CoverME.gov, Maine’s Health Insurance Marketplace.

Plan selections provide a snapshot of activity by new and returning consumers who have selected a plan for 2025. “Plan selections” become “enrollments” once consumers have paid their first monthly premium to begin insurance. These numbers are subject to change as consumers may modify or cancel plans after their initial selection.

The deadline to select a plan for coverage beginning January 1, 2025 is December 15, 2024. Consumers who select a plan between December 16, 2024 and January 15, 2025 will have coverage beginning February 1, 2025.

Federal and state subsidies are driving record enrollment

OLYMPIA, Wash. – More Washingtonians than ever before have signed up for health and dental insurance for 2025 through Washington Healthplanfinder. Washington Health Benefit Exchange runs Washington Healthplanfinder, the state’s online marketplace for Affordable Care Act (ACA) coverage.

As of the close of open enrollment on Jan. 15, more than 308,000 Washingtonians had selected health and dental plans for 2025. This preliminary number includes people renewing their coverage and nearly 50,000 new customers.

IMPORTANT: See caveats below regarding the impact of Medicaid Unwinding & other enrollment changes over time on these estimates.

12/12/24: Note: ACA Medicaid Expansion data has been updated by 3 months for most states, from March 2024 to June 2024.

With another GOP trifecta and Trump's Project 2025 promising draconian cuts to federal spending, there's a very good chance that the Affordable Care Act is, once again, on the chopping block.

I have no idea what's going to happen to either it, Medicaid, Medicare, the Children's Health Insurance Program (CHIP), the VA or the Indian Health Service, but whatever it is probably isn't gonna be pretty.

With that in mind, I figured it would be helpful to take stock of just how many Americans are actually receiving healthcare coverage through the ACA...and while I've crunched this number several times before, I'm taking it several steps further this time and breaking it out not only by state, but by Congressional District (CD).

But actually, he thought as he re-adjusted the Ministry of Plenty’s figures, it was not even forgery. It was merely the substitution of one piece of nonsense for another. Most of the material that you were dealing with had no connexion with anything in the real world, not even the kind of connexion that is contained in a direct lie. Statistics were just as much a fantasy in their original version as in their rectified version. A great deal of the time you were expected to make them up out of your head.

For example, the Ministry of Plenty’s forecast had estimated the output of boots for the quarter at 145 million pairs. The actual output was given as sixty-two millions. Winston, however, in rewriting the forecast, marked the figure down to fifty-seven millions, so as to allow for the usual claim that the quota had been overfulfilled. In any case, sixty-two millions was no nearer the truth than fifty-seven millions, or than 145 millions.

I recently published an ambitious spreadsheet which attempted to compile a comprehensive & up to date tally of total ACA healthcare coverage (including both exchange-based Qualified Health Plans (QHPs), Basic Health Plans (BHPs) and ACA Medicaid expansion enrollment), broken out by not just state but by Congressional District.

Doing this on a state-by-state level is easy. Doing so by Congressional District (CD) gets a lot trickier.

As I noted in my prior article, for state level ACA enrollment I'm using official data reports from the Centers for Medicare & Medicaid Services (CMS) for the "baseline" numbers, supplemented by more recent state-level data from some of the state-based ACA exchanges & state Health & Human Services departments.

There's only a single CD in Alaska, Delaware, Montana, North Dakota, South Dakota, Vermont and Wyoming, as well as one non-voting House member in the District of Columbia, so no further work is needed for those. For the other 43 states, however, breaking the enrollment data out by CD gets trickier.

SACRAMENTO, Calif. — Covered California has announced a special-enrollment period for residents of Los Angeles and Ventura counties, where a state of emergency has been declared due to the Palisades and Eaton Fires that have destroyed over 12,000 homes and displaced hundreds of thousands of Californians.

“These fires have caused unprecedented destruction and have upended the lives of so many living in Southern California,” said Covered California Executive Director Jessica Altman. “Everyone who is uninsured and has been affected by these fires, directly or indirectly, will have an extended opportunity to obtain health insurance through Covered California or Medi-Cal over the next two months.”

Californians have 60 days from the date that the state of emergency was declared in their county to sign up for coverage, so this special-enrollment period will last until March 8.

Other resources made available to Californians affected by the fires can be found here:

A week or so ago the Centers for Medicare & Medicaid Services (CMS) issued a semi-final 2025 ACA Open Enrollment Period report, which noted that 23.6 million Americans had selected 2025 plan year coverage via the various ACA marketplaces since November 1st...as of either January 4th or December 28th, depending on the state.

Those thru dates are important, of course, because the 2025 OEP was still ongoing in every state except Idaho at the time...and in fact it's still going on in several of them, including CA, DC, MA, NJ, NY, RI & VA. In some of these states the final deadline is still up to 2 weeks away.

The biggest program on the hit list, however, is Medicaid, which would make up nearly half of the $5 TRILLION in budget cuts Republicans have in mind in order to pay for...massive tax cuts for corporations & the wealthy, of course.

In October 2024, 79.3 million individuals were enrolled in Medicaid and CHIP.

72.1 million individuals were enrolled in Medicaid, and 7.2 million individuals were enrolled in CHIP.

41.7 million adults were enrolled in Medicaid, and there were 37.6 million Medicaid child and CHIP enrollees.

Medicaid and CHIP Applications Received

In October 2024, Medicaid, CHIP, Human Services agencies, and State-based Marketplaces received 2.6 million applications, or 2 percent more applications, as compared to September 2024.

The number of applications received has increased by 20 percent since October 2023 and increased by 66 percent since October 2022.

Total Medicaid/CHIP enrollment in October 2024 still dropped very slightly from September...by just 55,000 people.