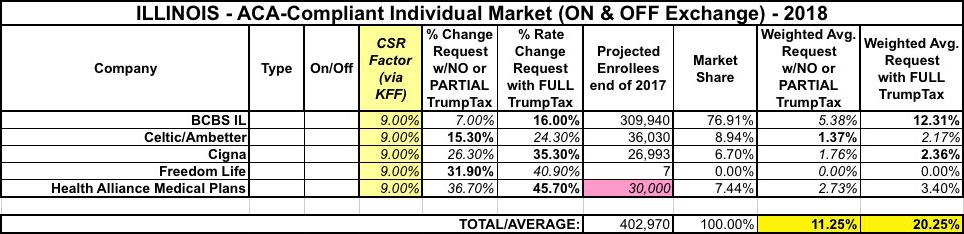

Another major state: Illinois. I've decided to scrap the "Low/High Increase" columns since they just confused people and made the table too wide, but replaced them with a new column showing the CSR factor estimate according to the Kaiser Family Foundation. Note that the percent listed will be smaller than Kaiser's estimate for each state, because their numbers only apply to silver plans, not all metal levels.

For instance in Illinois, Kaiser estimates that carriers would have to raise rates by 14% on Silver plans to cover their CSR losses. However, only 64% of Illinois exchange enrollees have silver plans to begin with, so I'm only plugging in about 9%. There are 5 carriers operating on the Illinois individual market (well, really 4, since "Freedom Life" doesn't count). I have the hard enrollment numbers for 4 of the 5; for Health Alliance Medical Plans I used 30,000 based on their 2016 number. Overall, Illinois is looking at around 11.3% w/partial sabotage, 20.3% with full sabotage:

Whew! OK, Texas was a bear for obvious reasons...13 different carriers (well, 12 really...Centene is new to their market). Several more are dropping out (Aetna, Allegian, Cigna, Humana, Memorial Hermann and Prominence), but suposedly theyonly have around 64,000 enrollees in TX combined. Texas's total individual market is actually closer to 1.6 million, so I'm obvoiusly missing a big chunk of enrollees below (and before my regular commenters say it: Yes, I'm sure the off-exchange TX indy market has shrunk this year, but I find it hard to believe it's shrunk by over 60% already).

Anyway, I've managed to plug in one hard request percent for each carrier--the FULL Trump Tax for 3 of them, the NO/PARTIAL Trump Tax for most. In Vista's case, they're off-exchange only so the CSR issue isn't a factor anyway. Unfortunately, I can't seem to find the enrollment number for Community Health Choice, so I don't know what their share of the market is, which could make a big difference if they have high enrollment. I've plugged in a flat 100,000 enrollees for the moment, but will change that if I'm able to track the actual number down.

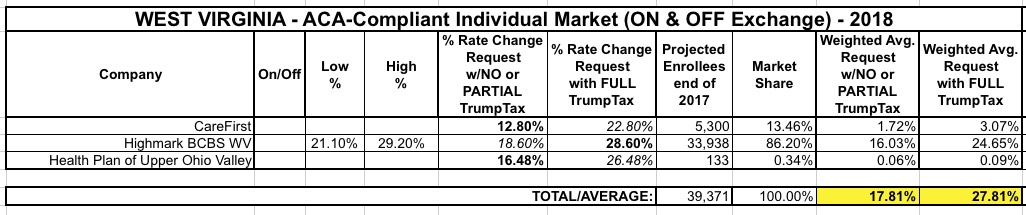

Another fairly straightfoward state: Three carriers, two of which (CareFirst and Health Plan of Upper Ohio Valley) appear to be assuming CSR payments will be paid; the third, Highmark BCBS (which holds the vast bulk of the individual market) openly states that they assume they won't be made and that the mandate won't be enforced to boot. I'm once again assuming roughly 2/3 of Kaiser Family Foundation's "Silver CSR hike", which in this case would be about 10%, giving the following: 17.8% if CSR payments are made, 27.8% if they are:

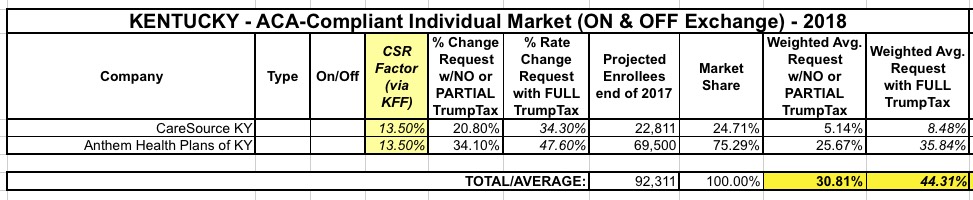

Louise Norris gave me a heads up that the Kentucky Insurance Dept. has posted their 2018 rate hike filings as well. The individual market is pretty straightforward...and pretty grim: Both individual market carriers, CareSource and Anthem, are asking for pretty steep rate hikes even if CSR payments are locked in next year, averaging around 30.8%, while assuming another 13.5 points on top of that (71% of Kaiser's 19% Silver average) would bring the average up to around 44.3%. Not much else to say about this one for the moment.

The states filings are piling up quickly...Arkansas is pretty straightforward. Interestingly, four of the five carriers seem to be assuming that CSR payments will be made, and have submitted their rate filings accordingly; the fifth (and largest), USAble Mutual (aka Blue Cross Blue Shield of AR) is the only one to break it out specifically. In order to estimate the CSR factor for the other 4 carriers, I'm assuming 2/3 of Kaiser's 15% Silver plan bump estimate, or around 10 percentage points. That brings things in at around 10% even without CSR sabotage or nearly 18% with the CSR factor.

One other important thing to keep in mind regarding Arkansas: Their total individual market, including grandfathered and transitional plans, is something like 430,000 but they only have around 70,000 officially enrolled in ACA exchange policies. The main reason for this is that they have another 320,000 people enrolled in exchange policies via their "Private Medicaid Option"...which is Arkansas' version of ACA Medicaid expansion. For some reason, those folks aren't counted as ACA exchange enrollees even though it's my understanding that the only distinction between them and the 70K official enrollees is where the payments/subsidies come from.

In late May, I noted that Blue Cross Blue Shield of North Carolina, which holds a near monopoly on the individual market in NC with around 95% of total enrollment, had submitted an initial rate hike request for 2018 averageing 22.9% overall. What was remarkable at the time is that while most carriers were pussyfooting around using euphamisms about the reasons for their excessive increase requests, BCBSNC was among the first to come right out and state point-blank that it's the Trump Administration's deliberate sabotage of the market--primarily via the threats to cut off CSR payments and to not enforce the individual mandate--that are responsible for over 60% of the increase. This is from their blog, not mine:

Alabama, Alaska and Wyoming only have a single insurance carrier participating in each of their individual markets. While this is a bad thing from a competitiveness POV, it cetainly makes things easier for me from a tracking-average-rate-hikes POV.

ALSO IMPORTANT: The HHS Dept. is also starting to upload the rate filings to the official RateReview.Healthcare.Gov database, which should make things easier for me going forward (assuming that the data is uploaded properly and isn't messed with, which is a distinct possibility when it comes to the Trump Administration)

Officially, Alabama has the infamous "Freedom Life" phantom plan which is asking for a whopping 71.6% rate hike...to allegedly cover exactly one (1) person statewide. Un-huh.

Aside from that, however, it's Blue Cross Blue Shield across all three states...and they're asking for the following:

This isn't a full analysis, since I only have 2018 rate hike data for one of Arizona's carriers so far...on the other hand, AZ only has a couple of carriers on the individual market these days anyway. From AZCentral:

The Affordable Care Act insurer in 13 of Arizona's 15 counties plans to raise average rates across all plans a moderate 7.2 percent next year.

But Blue Cross Blue Shield of Arizona officials said the rate increases would be flat if President Donald Trump's administration did not plan to eliminate a key Affordable Care Act funding source.

7.2% isn't bad at all...of course, that comes after last years massive 57% average rate hike. Still, 0% would obviously be much better than 7%...

Trump suggested in a weekend tweet that " ... bailouts for insurance companies and bailouts for members of Congress will end very soon" unless Congress acts quickly on a new health bill.

Covered California Releases 2018 Rates: Continued Stability and Competition in the Face of National Uncertainty

Covered California remains stable, with an average weighted rate change of 12.5 percent. The change is lower than last year and includes a one-time increase of 2.8 percent due to the end of the health insurance tax “holiday.”

The competitive market allows consumers to limit the rate change to 3.3 percent if they switch to the lowest-cost plan in the same metal tier.

For 2017, unsubsidized enrollees on the Minnesota individual market faced massive rate hikes averaging 57%. It was so bad that the only way they could convince some carriers to participate in the market was to allow most of them to put a cap on how many people they'd enroll (with the balance being shunted over to Blue Plus, the HMO division of BCBSMN). This resulted in a massive initial surge of enrollment, as it was on a first-come, first-serve basis...but also left off-exchange and unsubsidized exchange enrollees high and dry.

In response, the state scrambled to pull together a $300 million package to help supplement premiums for those folks...knocking a flat 25% off of their premiums for 2017. This helped ease the problem in the short term, but the larger issue still loomed going forward.