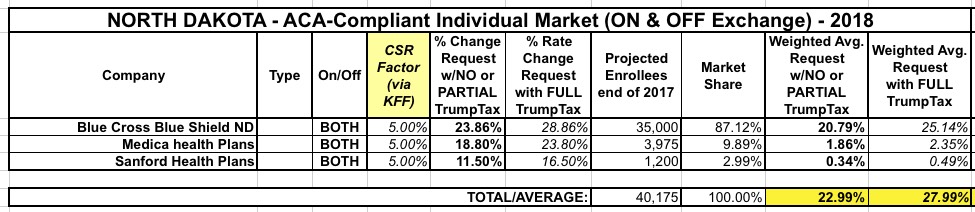

North Dakota's numbers are pretty straightforward. Only three carriers, none of whch say anything about CSR or mandate concerns, so I have to assume that their requested rate increases are the best-case scenario. In addition, the KFF estimates suggest only a 5 point additional CSR factor anyway. This results in roughly a 23% average hike if CSRs are paid vs. a 28% increase if they aren't.

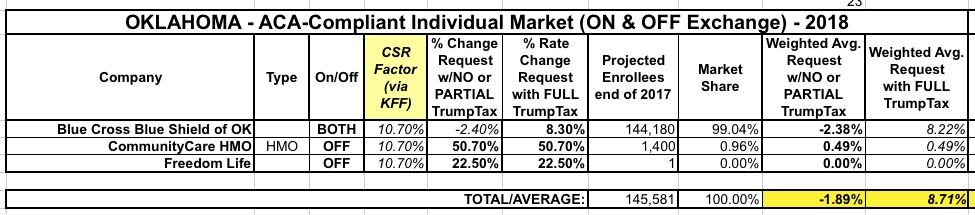

Last year, Blue Cross Blue Shield of Oklahoma, as the only carrier participating on the ACA exchange in the state, jacked up their premiums by a jaw-dropping 76%. This resulted in the highest statewide average rate hike in the country of 71% overall.

Well, that certainly seems to have done the trick: This year BCBSOK (still the only on-exchange player and holding over 99% of the market anyway) is requesting a (relatively) modest 8.3% average rate increase...and their filing specifically calls out both the CSR and mandate enforcement factors as being major reasons. Assuming the Kaiser Family Foundation's estimates are accurate, that means that if the CSR payments were guaranteed for 2018, BCBSOK should actually be lowering their rates slightly, to the tune of around 2.4%.

Adding in the steep hikes from off-exchange only CommunityCare (which only has 1,400 enrollees) brings the averages in at a 1.9% rate drop if CSRs are paid, and an 8.7% increase if they aren't.

The good news is that Wisconsin has one of the most robust and competitive exchange markets in the country. The bad news is that, contrary to popular opinion, "competition" doesn't by itself magically lower prices, at least not by enough. Both Anthem and Molina are leaving the ACA exchange (although Anthem is technically sticking around off-exchange), but there's over a dozen other carriers still duking it out.

According to the 11 carriers I have enrollment numbers for, the statewide average rate increase being requested is around 20.8% assuming CSR payments are made; using the Kaiser Family Foundation estimates, that translates into roughly 32.4% assuming they aren't made. Unfortunately, I can't seem to dig up the enrollment data for four carriers: Aspirus, Compcare, Wisconsin Physician Service and WPS (I think the last two are actually subsidiaries fo the same company). Wisconsin's total individual market should be roughly 280,000 people, and when you add up all the numbers I have (including Anthem/Molina) it only comes to around 180,000, so there appear to be roughly 100,000 enrollees missing among those 4 carriers, or over 35%.

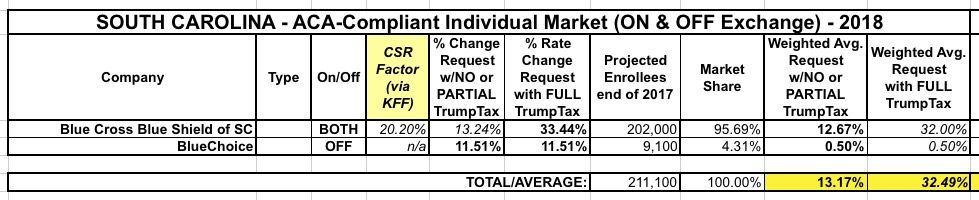

I admit to being a bit confused about the distinction between BCBSSC and BlueChoice HealthPlan, which is also a BCBS carrier...I'm guessing one is for HMOs, the other for PPOs or something. In any event, BlueChoice plans appear to only be available off-exchange, and are thus not subject to the CSR issue. BCBSSC is, however, and the Kaiser Family Foundation estimates that their Silver plans would have to go up 23% if CSR payments are cut off. 87%% of SC exchange enrollees are on Silver plans, so that should be roughly 20.2% across all policies.

If CSR payments are made, South Carolina is looking at around a 13.2% average rate hikes; if they aren't, it's an uglier 32.5%.

We're heading into the home stretch now, with the only remaining "supersize" state, FLORIDA. FL has the largest exchange-based individual market enrollment, and the 2nd largest total individual market enrollment of any state in the country, surpassing California for a variety of local economic/demographic reasons. The Kaiser Family Foundation estimates that FL carriers would have to add about 25% to their Silver plan premiums in order to make up for CSR reimbursements if Trump pulls the plug and/or Congress doesn't formally appropriate them. Since 80% of FL exchange enrollees are on Silver plans, that translates to roughly a 20% additional "Trump Tax" for the CSR factor alone. Note that while none of the carriers mention the CSR issue (meaning they all assume the payments will be made), Molina does call out the individual mandate enforcement issues as being part of their 37.5% rate increase request. Unfortunately, they don't put a hard number on this.

With Blue Cross Blue Shield of Nebraska declining to participate in the Nebraska exchange, that leaves just Medica as the sole individual market carrier. They're asking for a 16.9% average rate hike,

Interestingly, while Medica's rate filing letter clearly states that the 16.9% request assumes CSR payments will be made and the mandate will be enforced, they also list "unprecedented uncertainty/risk inherent in the marketplace" as one of the key drivers of the increase.

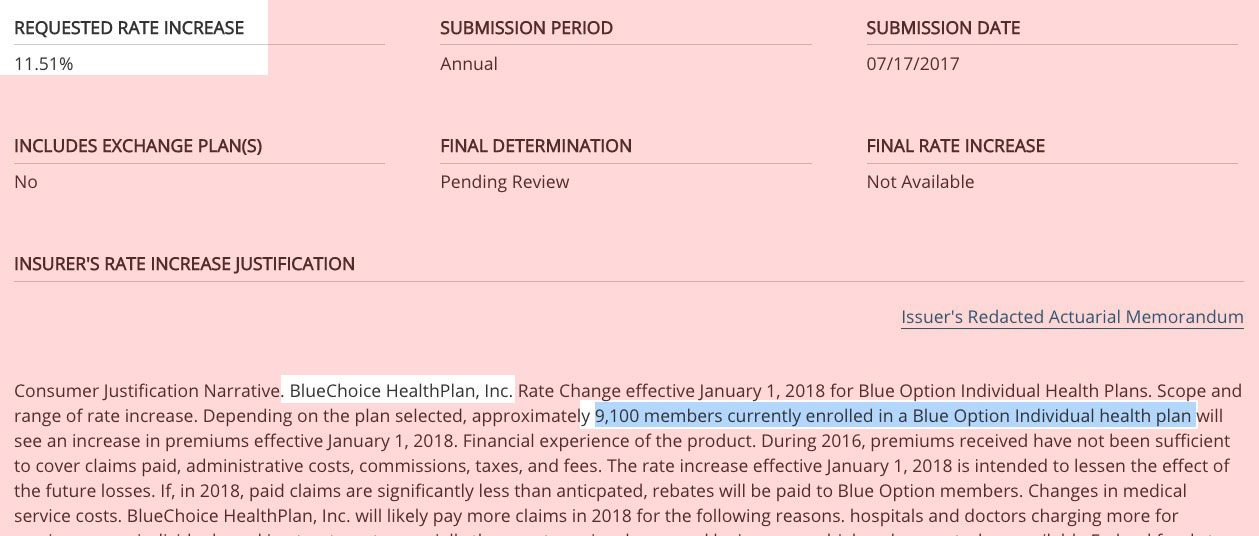

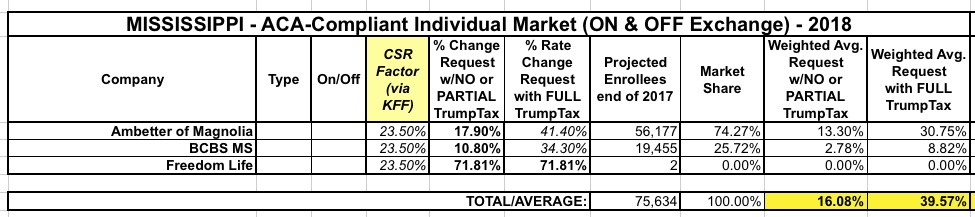

There's only two carriers participating in Mississippi's individual market next year (plus Freedom Life, which once again is just a shell company here). They're asking for 16.1% average rate hikes, and since there's no mention in any of the filings about CSR payments not being made or the mandate not being enforced, I'm assuming that increase doesn't account for those factors.

Massachusetts has one of the stablest statewide insurance markets, no doubt in large part due to their having instituted the precursor to the ACA, "RomneyCare", 4 years earlier. Massachusetts also merged their small business and individual market risk pools, which helps stabilize things. As a result, they have a high number of carriers participating in their ACA exchange and are among the few states with single-digit average rate hikes...assuming CSR payments are forthcoming and the individual mandate is properly enforced.

Assuming CSR payments aren't made, I used the Kaiser Family Foundation's 19% average estimate for Silver plan hikes due to the CSR factor. Since a whopping 92% of MA's exchange enrollees chose Silver plans (it looks like MA's unique "ConnectorCare" plans are considered Silver as well), that means an average CSR factor of around 17.5 points across the entire individual market.

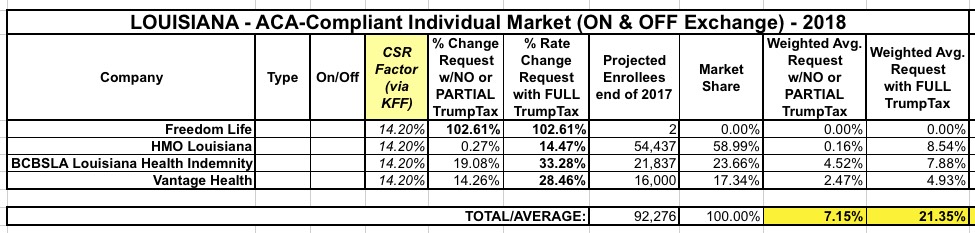

Louisiana has 3 individual market carriers for 2018 (technically there's 4, but "Freedom Life" is basically just a shell company with a placeholder filing). Officially, they're requesting average rate increases averaging around 21.4%...but all three carriers state point-blank in their filing letters that a huge chunk of their request is due specifically to the CSR reimbursement and mandate enforcement issues. The Kaiser Family Foundation estimates the CSR issue alone adds around 20 points to Silver plans, and 71% of Louisiana exchange enrollees chose Silver, so that translatest into roughly 14.2 points across the whole market. This results in just a 7.2% average rate hike if CSR payments are made vs. 21.4% if they aren't:

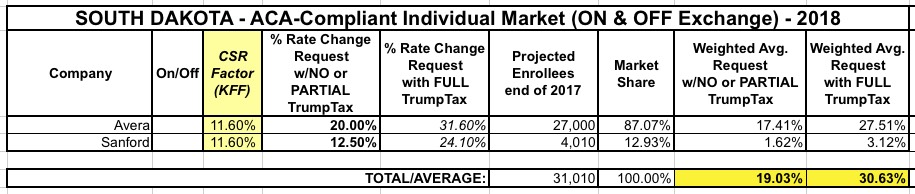

South Dakota is another fairly straightforward state: Two carriers, around 31,000 total ACA-compliant enrollees on & off exchange. Neither filing indicates whether they're assuming CSR payments will be made or not, so I'm assuming they're based on them being paid.