It feels almost silly for me to spend so much time crunching the average 2018 rate hike numbers at this point. Between the (supposedly failed?) GOP repeal effort and Donald Trump's ongoing sabotage efforts--including what could be him officially pulling the plug on CSR reimbursements as early as sometime today--it's probably a bit of a futile effort. Besides, a dozen other wonks/analyses have already confirmed what the Kaiser Family Foundation projected months ago and which I've been proving on a state-by-state basis for months now: The CSR threat is causing average rate hikes of around 20 points on average, and the threats to individual mandate enforcement are tacking on another 4-5 points on top of that, beyond the ~10 points which rates would normally be increasing on average.

UPDATE 9/27/17: It now looks extremely likely that CSR reimbursement payments will not be guaranteed for 2018 (they may or may not be paid, mind you, but it's unlikely that they'll be legislatively appropriated, which amounts to the same thing as far as most insurance carriers are concerned). With this in mind, I'm re-upping this rather wonky/in-the-weeds tutorial about the #SilverSwitcharoo, since it looks like at least 6 states (California, Connecticut, Florida, Idaho, North Carolina and Pennsylvania) are likely to end up using it this fall.

UPDATE 10/12/17: Welp. Sure enough, Donald Trump is indeed officially planning on pulling the plug on CSR reimbursement payments. Several healthcare wonks, including myself, have been tracking how different states are handling the CSR load issue; so far it looks like 22 are "Silver Loading" and 10 are going "full Silver Switcharoo". This may change over the next week or so, however.

The states we know (or at least are pretty certain) are Silver Switcharooing are: California, Connecticut, Florida, Georgia*, Hawaii, Idaho, Minnesota, Nevada, South Carolina and Washington State.

*(At least one carrier in Georgia)

(Special thanks to folks like Josh Schultz, David Anderson, Andrew Sprung, Amy Lotven, Wesley Sanders and others for helping me make heads or tails out of the CSR brouhaha)

Those were Democratic Senate Minority Leader Chuck Schumer's words tonight in response to Republican Senate Majority Leader Mitch McConnell's claims that those on the left were "celebrating" the defeat of his Godawful "Skinny Repeal" bill late Thursday night. And that's a perfect description of how I feel, for several reasons:

1. This wasn't so much a case of an "Actively Positive" thing happening (as was the case with, say, the Obergefell v. Hodges Supreme Court decision) as it was stopping a negative thing (as was the case with the King v. Burwell SCOTUS decision, which actually was announced the very same day as Obergefell). That is to say, it's not that a good piece of legislation passed, it's that a bad piece of legislation was blocked. This isn't to minimize the importance of what just happened tonight (not just in terms of healthcare policy, but also the state of our democratic process, legislative norms and of course the ramifications for the rest of this ongoing nightmare we call the Trump Administration), but it does tend to dampen my emotional response a bit.

2. As I keep stressing: There are real problems with the ACA as it currently stands, and some of them require more than simple "tweaks" as some ACA defenders are prone towards describing them. All of these problems are definitely fixable, but most of those solutions still won't be easy to push through. Furthermore, these issues are exacerbated by two other problems:

3. THE CLOCK IS TICKING for 2018: The final carrier rate filing deadline is rapidly approaching; the carriers need to make their final decisions about how much to charge next year soon...assuming they decide to stick around the individual market next year at all, which isn't a guaranteed thing, especially due to...

4. THE TRUMP SABOTAGE FACTOR will now almost certainly go into overdrive. I'm about 90% certain that Trump will indeed pull the plug on Cost Sharing Reduction reimbursement payments staring next month (August), which could still devastate the indy market almost instantly. Of course, Congressional Republicans could resolve the CSR issue in about 5 minutes with a simple, 87-word bill which would receive unanimous consent from every Democrat in both the House and Senate as long as it was either standalone or not attached to some other poison pill piece of legislation.

For that matter, while the individual mandate repeal died with the "Skinny Repeal" bill failing, House Republicans have also started pushing through a different bill which would prevent the IRS from enforcing the individual mandate anyway, causing the exact same problems. And even if that doesn't happen, HHS Sec. Tom Price could simply start issuing hundreds of thousands of highly-questionable "hardship exemptions" letting pretty much everyone off the hook for the mandate penalty anyway...which, once again, would amount to the same fallout.

(yes, I know she actually says "bumpy night"...I'll update the title this evening if need be...)

OK...here's where things stood as of last night...

UPDATE 7/27/17 12:00pm: OK, here's the latest (at least, as of around noon, anyway):

Apparently, in order to win over a few more votes and squeeze the bill in under the "budget savings" wire, they're now planning on scrapping repeal of the medical device tax and delaying repeal of the employer mandate (but still repealing it eventually). They're also going to throw in defunding Planned Parenthood even though that was previously scrapped by the Senate parlimentarian.

Finally, they're apparently bringing back theEssential Health Benefit State Waiver provision, which would, once again, blow a massive hole in the "Guaranteed Issue and Community Rating" rules.

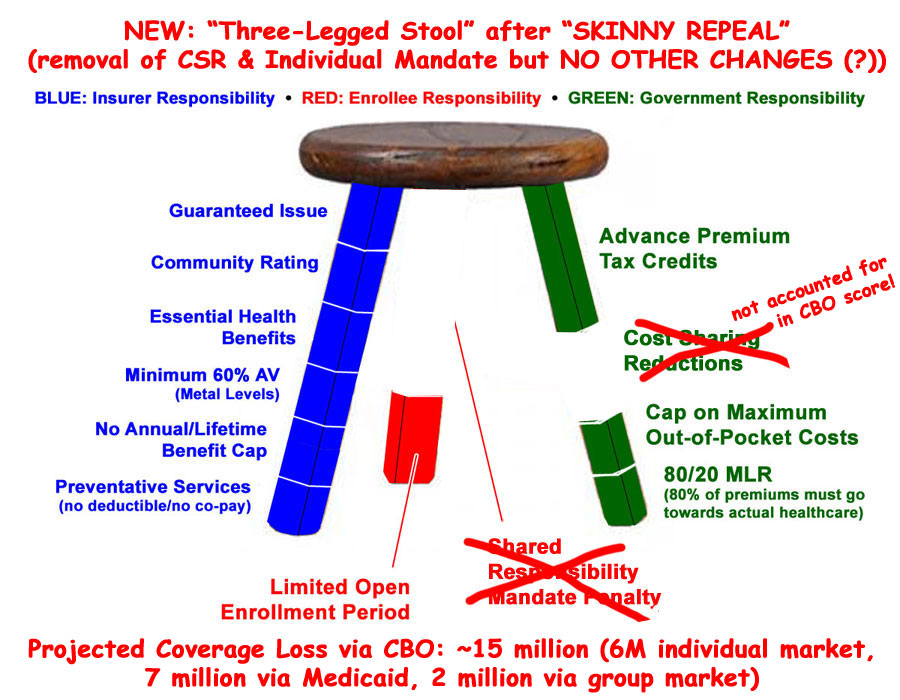

UPDATE: Hey, who's that up there? Why it's the guy who Republicans wanted to become President just 5 years ago, explaining why, if you're going to guarantee solid health insurance policies to everyone regardless of their medical history and without discriminating on price, you have to include some sort of incentive for them to do so: A carrot and a stick. The tax credits and out of pocket maximums are the carrot. The individual mandate and open enrollment period are the stick.

(sigh) I debated whether to even write a post about the last-minute "Skinny Repeal" plan slapped together by Mitch McConnell yesterday morning for a couple of reasons: First, because even if it passes, the sole purpose of "Skinny Repeal" is to get past the 50-vote Senate threshold...at which point it would be scrapped and replaced with whatever Godawful pile of garbage McConnell comes up with via reconciliation afterwards anyway.

Second, and more to the point, they're supposed to be voting on "Skinny Repeal" within the next few hours, so it's possible that it could be a moot point before anyone even reads this.

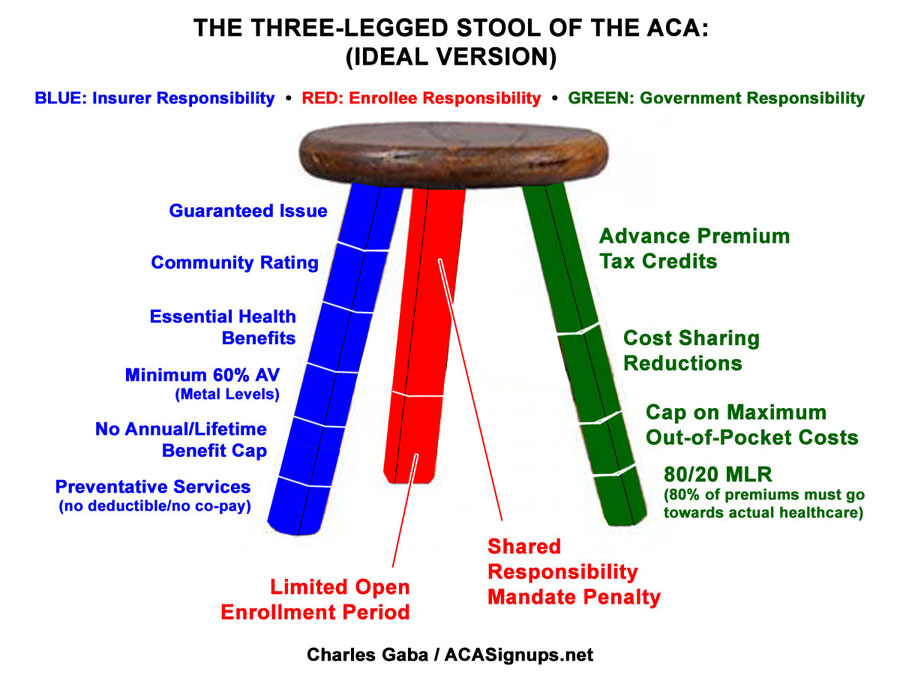

OK. Here we go. First, just as a refresher: Here's what the Individual Market was supposed to look like under the Affordable Care Act:

Here's what it actually looks like for a variety of reasons, including both legitimate glitches in the ACA itself as well as a whole lot of flat-out sabotage by the GOP over the past 7 years. While there are plenty of other issues which need to be addressed, the most obvious ones are that the tax credits need to be beefed up and applied to enrollees over the 400% FPL threshold, and the mandate penalty should really be increased. In short, two legs of the stool need to be lengthened...to continue the metaphor, we need a couple of shims. Around $12 billion per year or so should do the trick on the tax credit side. As it happens, one of the few useful parts of most of the GOP plans is that they do include a good $120 billion or so in "reinsurance/stabilization" funding over 10 years...which, in practice, would amount to about the same thing. The key is that this funding would have to be added to the existing ACA funding, not replacing it, which is what these plans do instead:

NOTE: The original focus of this diary was on the deliberate sabotage by the Trump Administration/HHS Dept. under Tom Price of the individual insurance market in general and HealthCare.Gov in particular, but the screen shot mentioned in passing in the diary below is actually far more important and disturbing the more I think about it than I had originally thought.

As noted below, it's an anonymous note sent to me on Thursday. Since it was sent I’ve confirmed the identity of the sender. This doesn’t prove that their specific claim is true, but there’s absolutely no reason I can think of for this person to risk their job and reputation by lying about this issue, and it matches everything else in the diary.

Several professional journalists have since contacted me and I’ve gotten them in touch with the sender. Stay tuned, this could be a big deal.

(sigh) I'm not really sure what the point of even writing about this is since it doesn't include the Cruz-Lee amendment which is supposedly the only thing keeping the ultra-conservative wing of the GOP Senate on board with BCRAP in the first place, but whatever:

CBO and the staff of the Joint Committee on Taxation (JCT) have prepared an estimate of the direct spending and revenue effects of the version of H.R. 1628, the Better Care Reconciliation Act, posted today on the Senate Budget Committee’s website.

By the agencies’ estimates, this legislation would lower the federal budget deficit by reducing spending for Medicaid and subsidies for nongroup health insurance. Those effects would be partially offset by the effects of provisions not directly related to health insurance coverage (mainly reductions in taxes), the repeal of penalties on employers that do not offer insurance and on people who do not purchase insurance, and spending to reduce premiums and for other purposes.

“The idea that you can repeal the Affordable Care Act with a two- or three-year transition period and not create market chaos is a total fantasy,” said Sabrina Corlette, a professor at the Health Policy Institute of Georgetown University. “Insurers need to know the rules of the road in order to develop plans and set premiums.”

But actually, he thought as he re-adjusted the Ministry of Plenty’s figures, it was not even forgery. It was merely the substitution of one piece of nonsense for another. Most of the material that you were dealing with had no connexion with anything in the real world, not even the kind of connexion that is contained in a direct lie. Statistics were just as much a fantasy in their original version as in their rectified version. A great deal of the time you were expected to make them up out of your head.