IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum requested weighted average rate increases for this state.

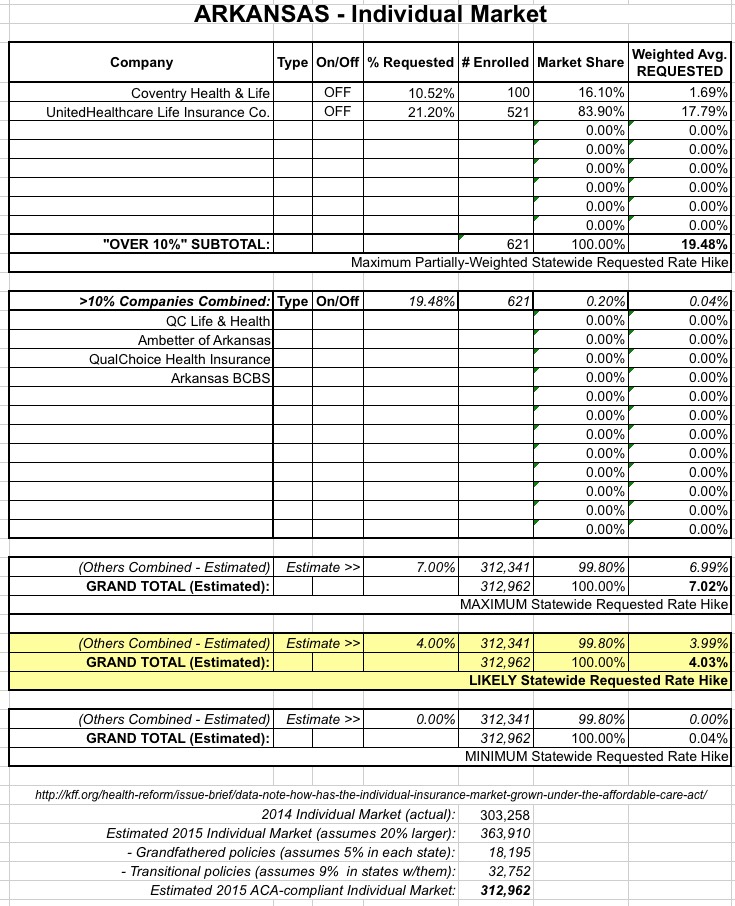

As explained in the first link above, I've still been able to piece together rough estimates of the low, mid-range and maximum possiblerequestedaverage rate increase for the Arkansas individual market. Note: While the table & methodology for Arkansas are the same as most of the other states I've posted on, there's one important difference here; see below for details:

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum requested weighted average rate increases for this state.

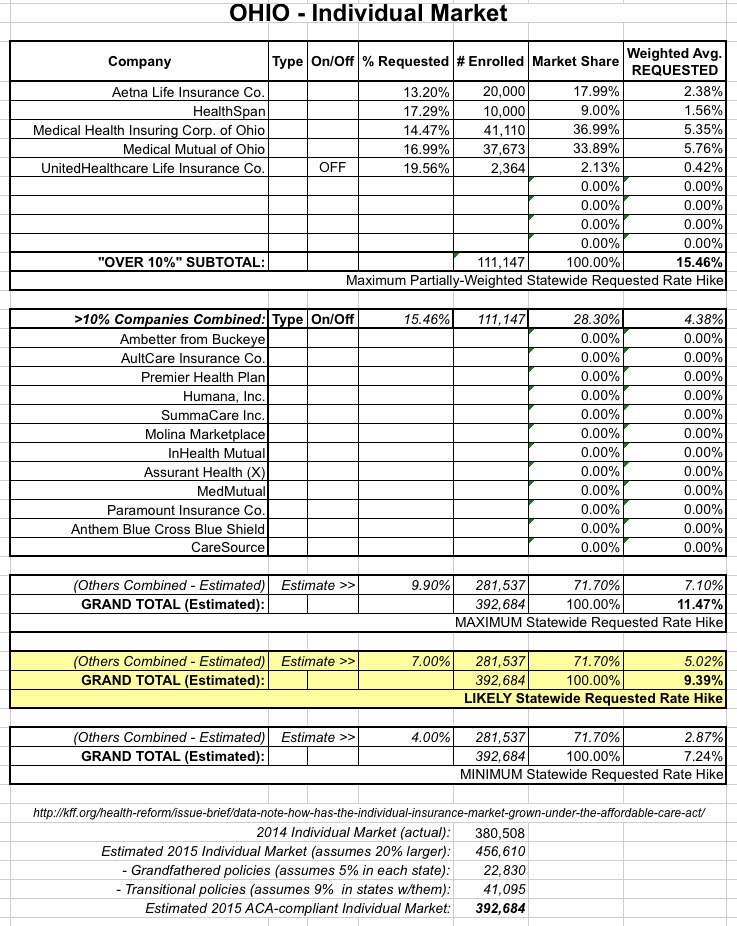

As explained in the first link above, I've still been able to piece together rough estimates of the maximum possible and mid-range requested average rate increase for the Ohio individual market:

Again, the full explanation is included here, but to the best of my knowledge, it looks like the companies with rate increases higher than 10% come in at a weighted 15.5% increase, but only make up about 28% of the total ACA-compliant individual market, with several other companies with requested increases of less than 10% (decreases in some cases) making up the other 72%.

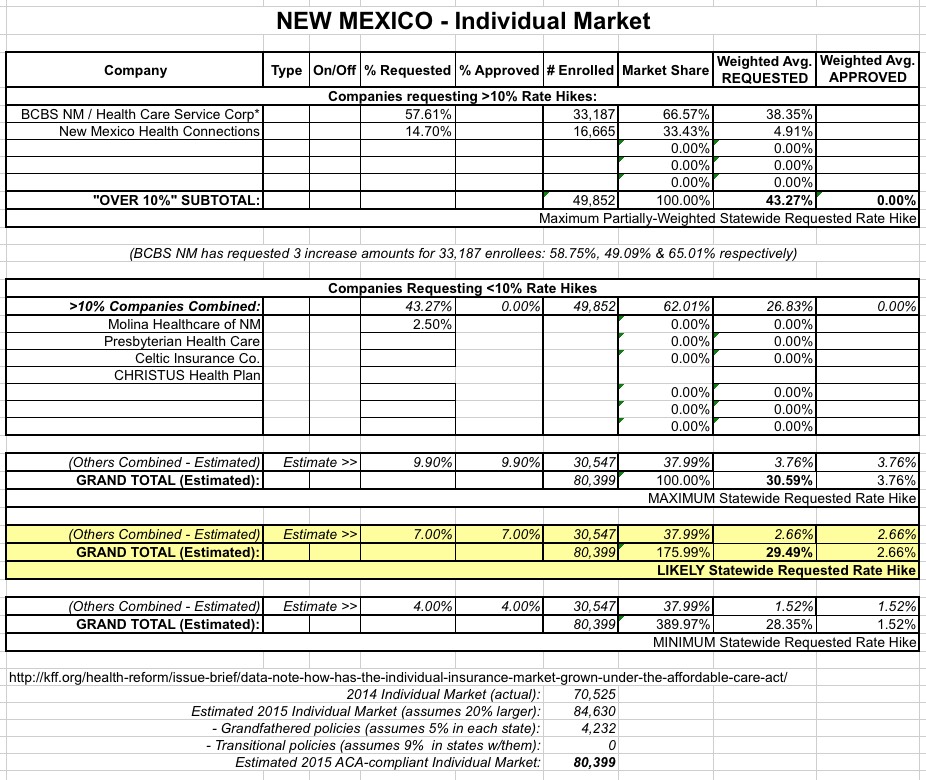

Last week I reported that insurance companies offering individual healthcare policies in New Mexico were asking for some pretty ugly rate hikes (on a percentage basis, anyway), mainly due to Blue Cross Blue Shield of NM (aka "Health Care Services Corp.") putting in for a jaw-dropping 57% hike. This resulted in 30% overall requested increases when weighted by market share.

Then, a few days later, the New Mexico state insurance commissioner announced the approved rate hikes for all 5 (or is it 6? see below...) of the companies in question. For BCBSNM (aka HCSC), they lopped the 57% hike down massively:

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum requested weighted average rate increases for this state.

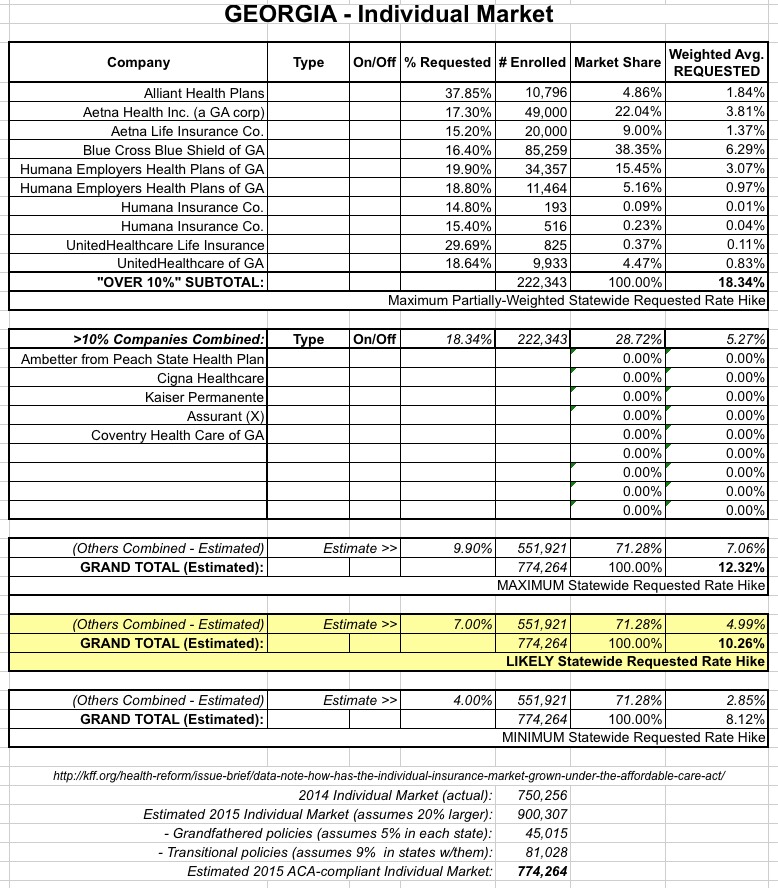

As explained in the first link above, I've still been able to piece together rough estimates of the maximum possible and mid-range requested average rate increase for the Georgia individual market:

Again, the full explanation is included here, but to the best of my knowledge, it looks like the companies with rate increases higher than 10% come in at a weighted 18.3% increase, but only make up about 29% of the total ACA-compliant individual market, with several other companies with requested increases of less than 10% (decreases in some cases) making up the other 71%.

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum requested weighted average rate increases for this state.

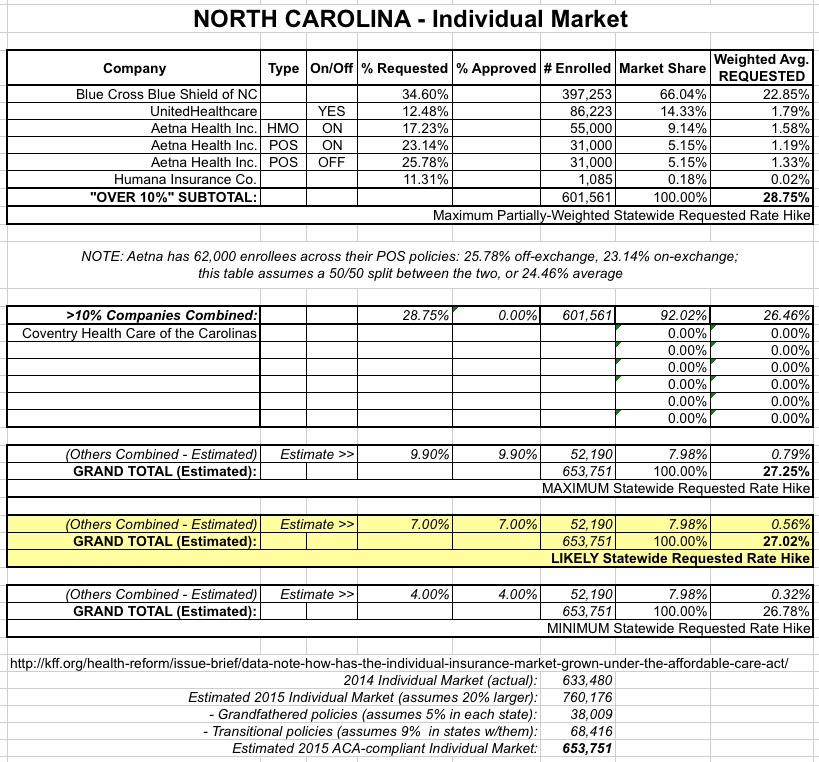

As explained in the first link above, I've still been able to piece together rough estimates of the maximum possible and mid-range requested average rate increase for the North Carolina individual market:

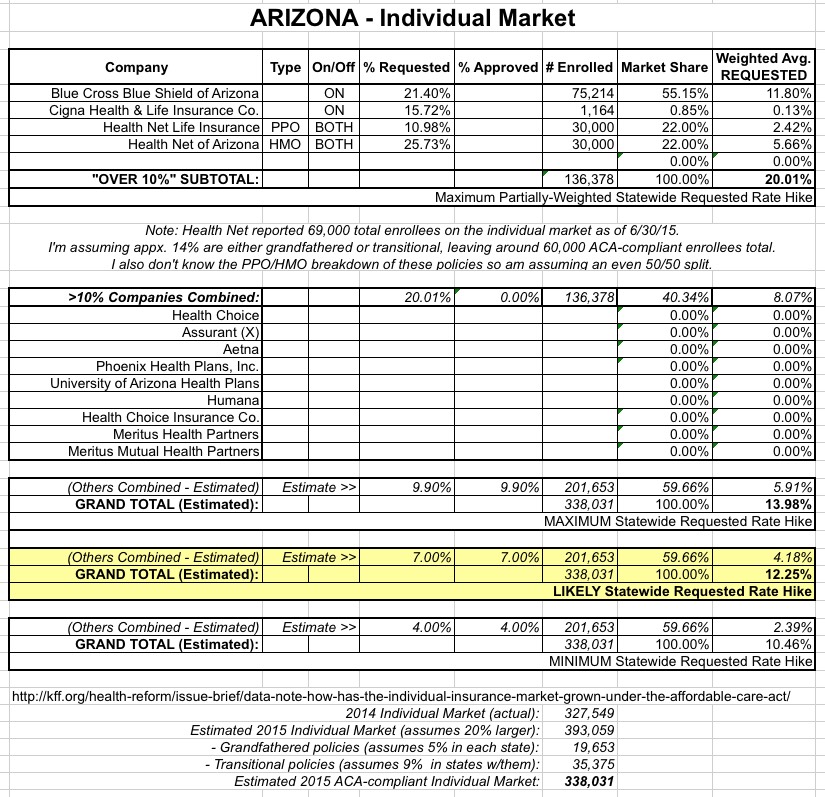

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum requested weighted average rate increases for this state.

As explained in the first link above, I've still been able to piece together rough estimates of the maximum possible and most likely requested average rate increase for the state's individual market:

As noted in the table, the Arizona analysis is even more fuzzy than most other states, because the enrollment/market share estimate for Health Net is a guess. According to their Q2 2015 SEC filing (page 49), Health Net had 69,000 people enrolled in individual policies in Arizona as of 6/30/15. They don't break out grandfathered/transitional policies (I'm assuming about 14% combined), nor do they provide a PPO/HMO split, so I'm just going with 50/50, or 60K total ACA-compliant enrollees.

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum requested weighted average rate increases for New Mexico.

As explained in the first link above, I've still been able to piece together rough estimates of the maximum possible and most likely requested average rate increase for the New Mexico individual market:

Again, the full explanation is included in the Missouri estimate linked at the top of this entry, but to the best of my knowledge, it looks like the companies with rate increases higher than 10% come in at a weighted 43.3% increase, but only make up about 62% of the total ACA-compliant individual market, with several other companies with approved increases of less than 10% (decreases in some cases) making up the other 38%.

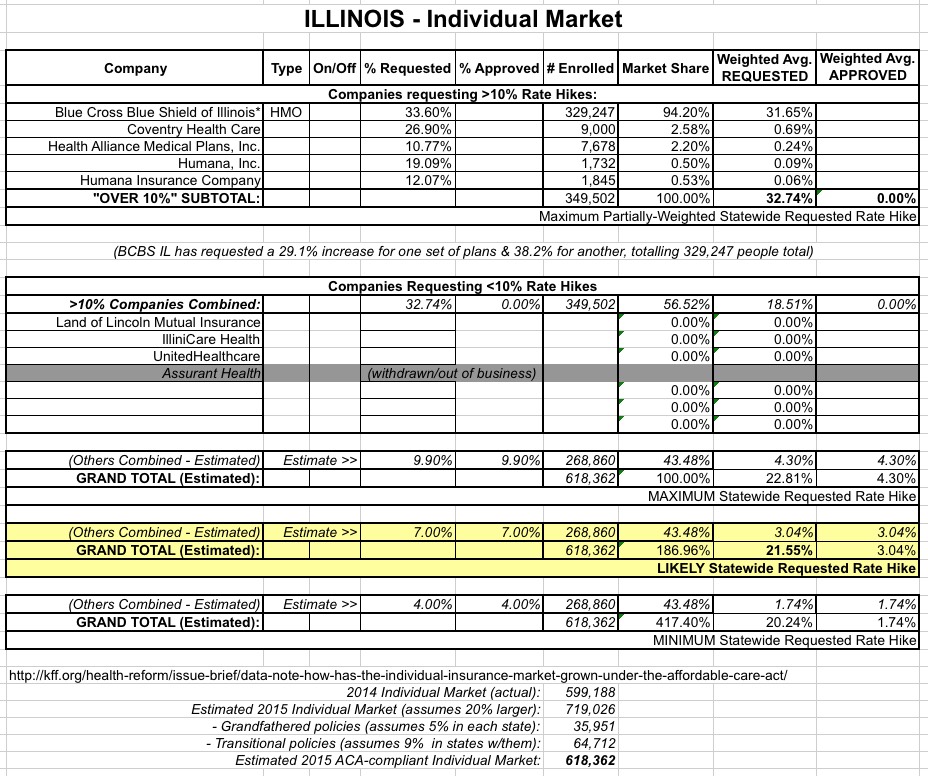

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum requested weighted average rate increases for Illinois

As explained in the first link above, I've still been able to piece together rough estimates of the maximum possible and most likely approved average rate increase for the Illinois individual market:

Again, the full explanation is included in the Missouri estimate linked at the top of this entry, but to the best of my knowledge, it looks like the companies with rate increases higher than 10% come in at a weighted 32.7% increase, but only make up about 57% of the total ACA-compliant individual market, with several other companies with approved increases of less than 10% (decreases in some cases) making up the other 43%.

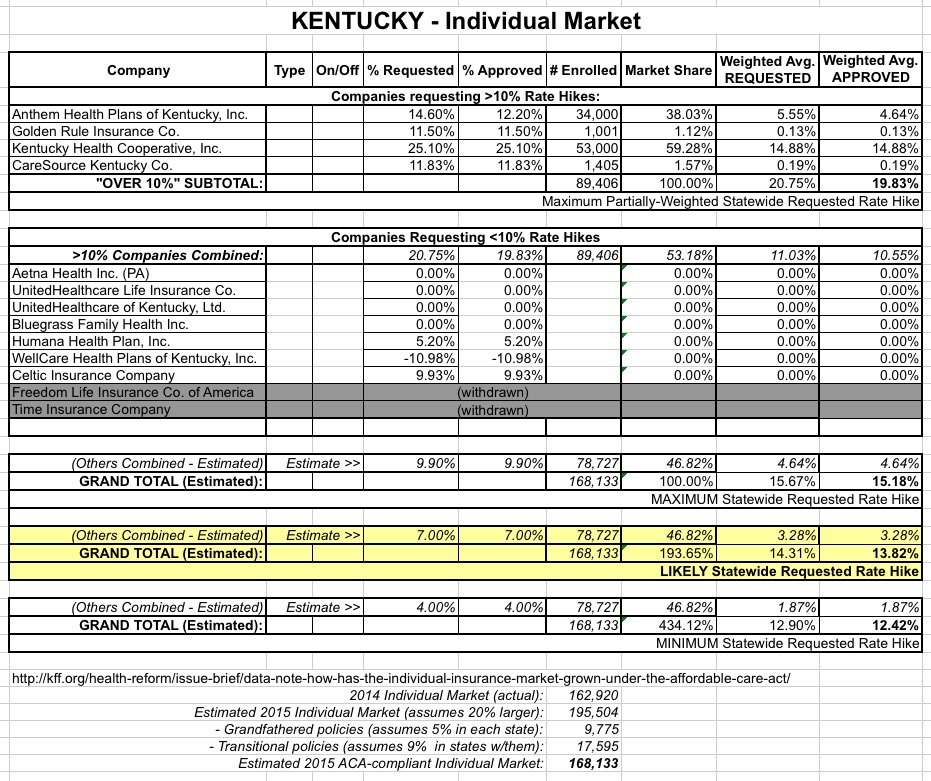

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum approved weighted average rate increases for Kentucky.

Fortunately, as I explain in the first link above, I've still been able to piece together rough estimates of the maximum possible and most likely approved average rate increase for the Kentucky individual market: