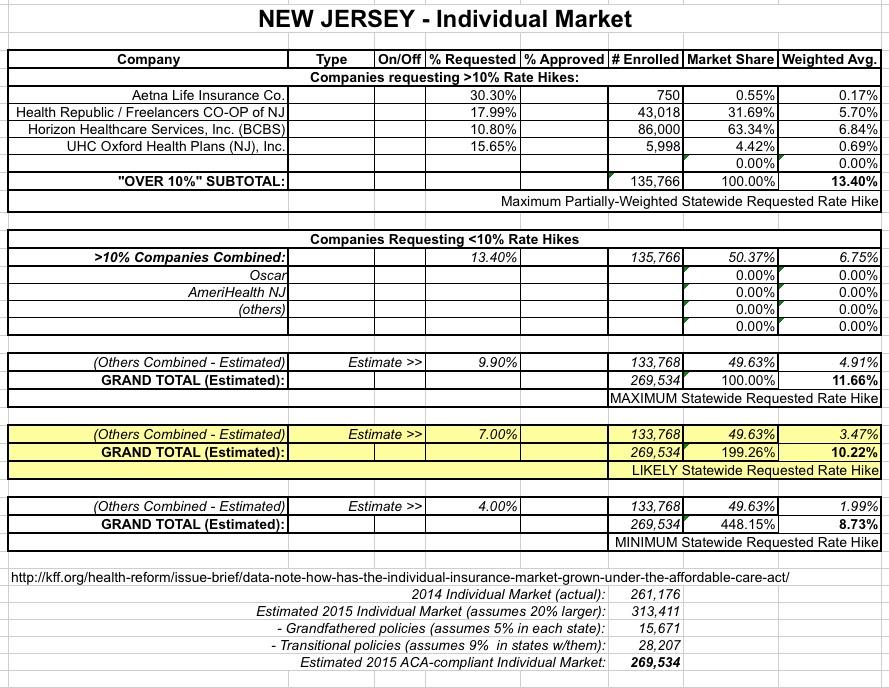

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum weighted average rate increase request for New Jersey

Assuming you've read through the explanation linked to above, here's my best estimate of the maximum possible and most likely average rate increase requests for the New Jersey individual market:

Again, the full explanation is included in the Missouri estimate, but to the best of my knowledge, it looks like the companies requesting rate increases higher than 10% come in at a weighted 13.4% increase, but only make up about 50% of the total ACA-compliant individual market, with several other companies (Oscar, AmeriHealth & possibly other off-exchange only companies) requesting increases of less than 10% (or possibly even decreases in some cases) and making up the other half.

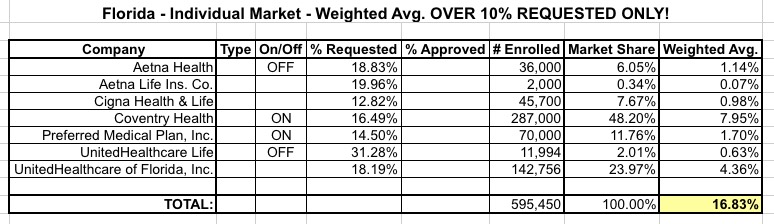

Last week I took the known 2016 Florida rate increase requests (around 14.7% weighted average for 10 companies with around 713,000 enrollees) and took my best shot at trying to estimate what the rest of Florida's ACA-compliant individual market might look like.

In order to do this properly, I'd need 2 pieces of data: First, the weighted average increase request for the 6 additionalcompanies which I didn't already have rate requests for; and second, the total ACA-compliant enrollment number for those 6 companies.

Just 2 days ago I posted an analysis of the New York individual market rate increase requests for 2016. My takeaway was that the weighted average requested was 10.0%, with the usual caveats about rounding errors, estimates of the total individual market size and so forth. Plus, of course, these were just requested increases, not final ones.

NEW YORK STATE DEPARTMENT OF FINANCIAL SERVICES ANNOUNCES 2016 HEALTH INSURANCE PREMIUM RATES, INCLUDING RATES FOR NY STATE OF HEALTH

Individual Rates for 2016 Remain Nearly 50% Lower than Before Establishment of New York’s Health Exchange

DFS Rate Reduction Actions Will Save Consumers More than $430 million

New Essential Plan Will Lower Premiums to $20 or Less and Provide Better Benefits for Lower-income New Yorkers

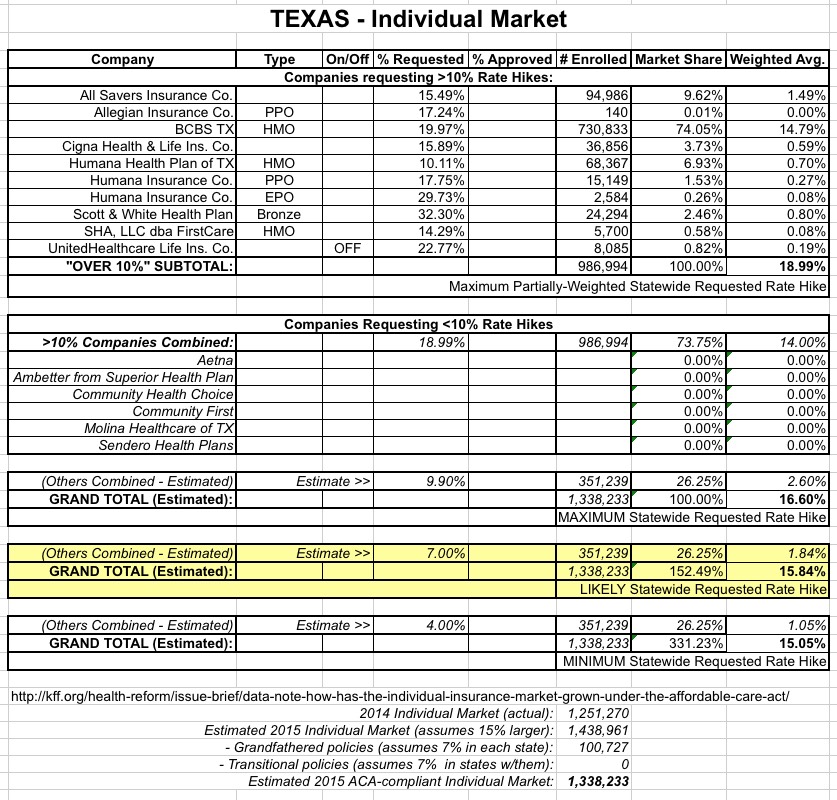

IMPORTANT:See this detailed explanation of how I've come up with the following estimated maximum weighted average rate increase request for Texas.

UPDATE 8/4/15: Revised table to display maximum, likely and minimum statewide average increase requests:

Assuming you've read through the explanation linked to above, here's my best estimate of the maximum possible rate increase requests for the Texas individual market:

Not sure how this slipped by me earlier today...I've been so busy trying to figure out the 2016 rate increases for each state that I missed this report from HHS about the 2015 premium and competition changes at Healthcare.Gov (this doesn't include the state-based exchanges, but still covers 2/3 of the states and 3/4 of total private enrollments):

Competition and Choice in the Health Insurance Marketplace Lowered Premiums in 2015

The Health Insurance Marketplace established by the Affordable Care Act allows consumers to compare health insurance plans based on key factors, such as covered services, providers, and importantly, price. According to a report released today, choice and competition increased in the 2015 Marketplace and consumers benefitted as new issuers entered and price competition intensified. In 2015, 86 percent of Marketplace-eligible consumers could choose from at least three issuers, up from 70 percent in 2014.

The Rate Review database at Healthcare.Gov is a very useful tool for any insurance company requesting rate increases above 10%, but it's completely useless for requests below 10%. As such, I have hard data on the requested increases for about 600,000 Florida residents:

If Florida's entire ACA-compliant individual market was only 600K people, that would be the end of the story.

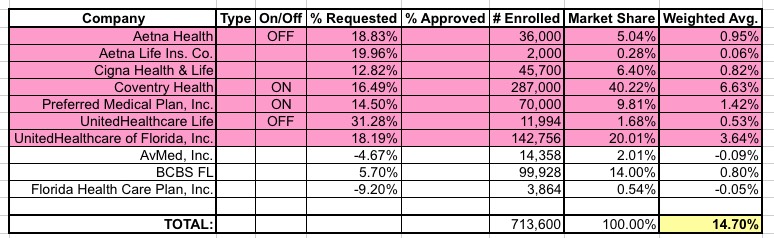

However, Florida actually has 16 different insurance companies selling individual policies...and the other 9 are all asking for lower than 10% hikes. After poking around the Florida Office of Insurance Regulation website as well as contacting the department directly, I've been able to pull together covered lives data for all 16, and requested rate change data for 3 more of them...2 of which are actually requesting rate decreases. When I add those 3 companies into the mix, the picture changes like so:

UPDATE 8/27/15: I've been writing up a whole mess of *approved* state rate updates today; look for this entry to be updated on Friday.

Recently, Richard Simpkins (aka icowrich) gave me the idea to take the known state-wide 2016 rate increase requests and go a step further, by plugging the weighted average rate increases for each state into a spreadsheet and then running a weighted average based on each state's proportion of the total U.S. population, like so (scroll to bottom of this entry for links to analysis for each state):

Most Mainers buying Affordable Care Act insurance will see modest increases in their premiums for 2016, below the national average and much lower than the double-digit increases projected in some cities by a recent study of initial rate filings.

About 80 percent of the 75,000 Mainers purchasing ACA marketplace insurance have a plan through Lewiston-based Community Health Options – formerly Maine Community Health Options. The ACA marketplace, operated on the Web as healthcare.gov, is where those without insurance – often part-time or self-employed workers – can obtain subsidized benefits.