"Benchmark" in this case refers to the plans which are used as the basis for the ACA's Advance Premium Tax Credit (APTC) formula. How much/little these particular rates change is even more important than the change in other policy rates, because these are the ones which the federal tax credit amounts are based on.

This is really important, because if the benchmark policy rate in your area changes, it can seriously impact how you receive in tax credits...even if nothing has changed at your end.

Maryland was one of the first states to release their list of requested 2016 rate hikes, and caused quite a stir at the time due to the largest player in the state, CareFirst, asking for a whopping 30% rate hike. At the time, I didn't have much to go on in terms of hard enrollment numbers, but it looked like the weighted average request would be somewhat lower, perhaps around 22-23%.

Today, the Maryland Dept. of Insurance has released the final, approved rate changes, and while 5 of the 8 companies on the individual exchange saw reductions in their rate change (2 others were approved as is, and one, Kaiser Health Plan was actually increased from 4.8% to 10%), it's still difficult to lock down a fully weighted average due to some crucial enrollment data missing.

I was able to track down the "covered lives" data for 5 of the eight companies.

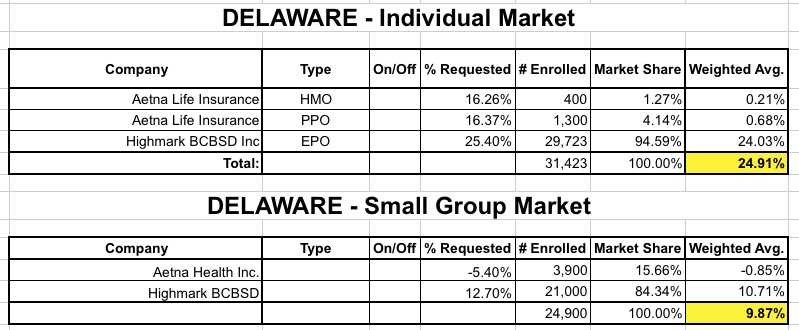

Delaware's 2016 rate hike analysis is about as simple and straightforward as it gets: Two companies (Aetna and Highmark BCBS) for both the individual and small group market, both on- and off-exchange, period...and their website includes the actual affected enrollee tallies for each, giving weighted totals:

Ugh. Nearly 25% requested for the individual market, just under 10% for the small group market. Of course these are requests only, so they might be slashed somewhat by regulators yet.

Louisiana's Insurance Dept. website is refreshingly complete: It includes every company on the individual & small group market, lists both the requested and approved rate hikes, and includes direct links to the filings which list the actual total enrollment in a clear-cut, consistent fashion.

In fact, the only data missing is some of the approved rate hikes; they've only posted the approved numbers for 3 of the 5 small group listings and 1 of the 10 individual listings, making it impossible to plug in the approved weighted average. However, the requested average is complete: About 15.4% for the individual market and 9.4% for the small group market.

Last year, while most state-wide average premium rates increased somewhat (averaging around 5.5% overall nationally, give or take), there were a few states which actually saw rate decreases from the year before: Arkansas, Mississippi and New Mexico saw overall decreases on their individual markets, while the District of Columbia and Hawaii saw decreases on their Small Business markets.

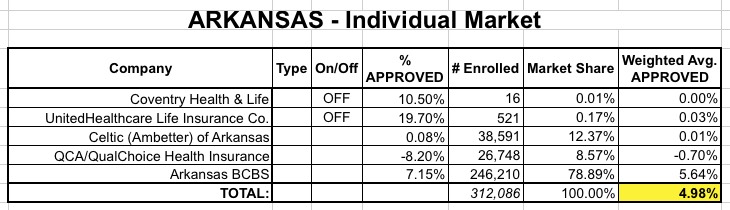

Last week I estimated the overall weighted average rate increases for the Arkansas individual market at "between 4-5%", with a rough estimate of around 4.6%.

Today, Arkansas Times reporter David Ramsey has provided the exact market share numbers for Arkansas. When I plug these in, the weighted average comes in a bit higher, at 4.98%:

HOWEVER, according to Ramsey, the Arkansas Insurance Division says that the actual weighted average is only 4.4% overall.

There could be any number of reasons for the discrepancy; it's possible that there's a few additional minor off-exchange carriers who I've missed, or there could be rounding errors/etc. In any event, these are all just estimates anyway, so I'll go with AID's official 4.4% figure.

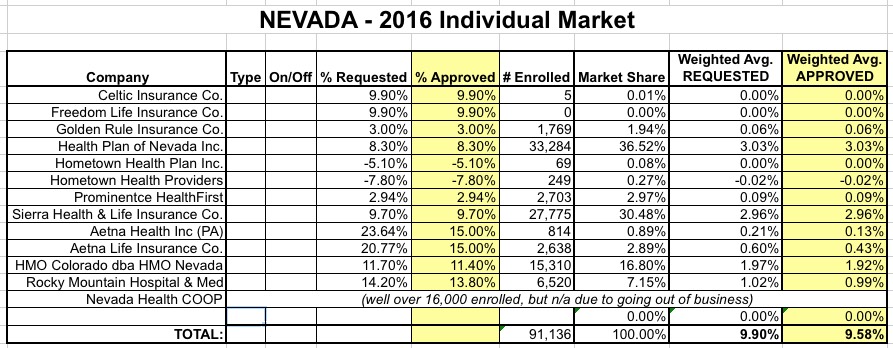

Nevada's insurance dept. rate filing website has an extremely user-friendly, interactive website which lets you drill down and find exactly what you're looking for: Individual or Small Group policies, HMO or PPO, Under Review or Reviewed. From what I can tell, there are 12 companies offering individual policies in 2016 (a 13th, the Nevada Health COOP, just announced that they've gone belly-up and are being dissolved, meaning a minimum of 16,000 Nevadans will have to switch to a different insurance carrier).

The requested rates were approved for 8 of the companies, but were reduced significantly for Aetna (from 21-24% down to 15%). Here's what it looks like in the end:

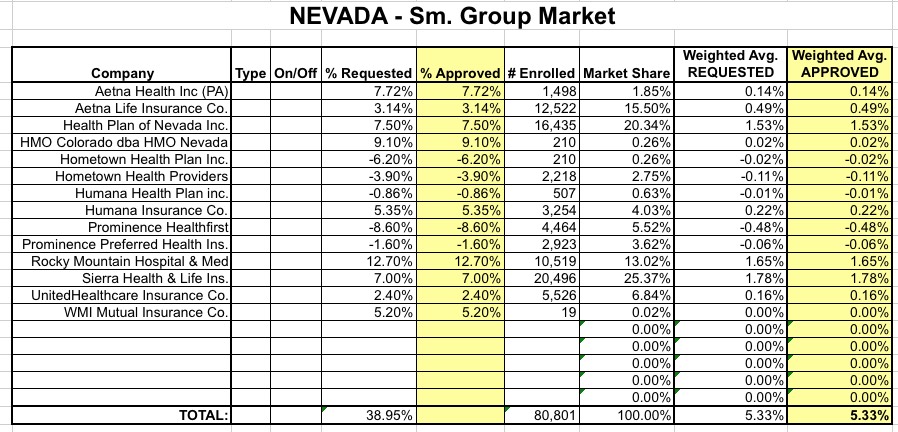

The Small Group market is faring somewhat better, with just a 5.3% overall weighted average increase:

When I last checked in on Rhode Island's 2016 rate increase status, the three companies operating in the state (BCBSRI, Neighborhood and UnitedHealthcare) had requested hikes of 7%, 8.6% and 11% respectively. There was no off-exchange enrollment data, but the exchange-based market share breakdown was roughly 48.5% / 48.5% / 3%. This meant a requested average hike of around 7.9%.

Still unresolved is how much Blue Cross and Blue Shield of Rhode Island may raise rates for its individual plans, which cover about 25,000 people. The nonprofit insurer initially requested an 18-percent increase, but no decision has yet been made because, by law, its rate hike requests are reviewed in a separate process that reserves a key role for the state's attorney general.

When I last checked in on the ongoing saga between the New Mexico Insurance Commissioner and Blue Cross Blue Shield of New Mexico, BCBS was threatening to take their ball and go home if NM Insurance Commish John Franchini didn't cave and agree to let them jack rates up by 51% on the individual market (Franchini had agreed to a 24% hike instead).

Thousands of New Mexicans will need to shop for new health insurance plans later this year after a decision by Blue Cross Blue Shield to stop offering individual insurance plans through the state health exchange beginning Jan. 1.

...The letter said Blue Cross Blue Shield of New Mexico lost $19.2 million in 2015 on the 35,000 individuals covered by plans they purchased on and off the exchange.

...Blue Cross will offer a basic-level insurance plan outside the exchange in 2016, which will be available to all consumers at the same rate as in 2015.