The Department of Insurance received preliminary 2020 health plan information from insurance carriers on June 1 and began reviewing the proposed plan documents and rates for compliance with Idaho and federal regulations. The Department of Insurance does not have the authority to set or establish insurance rates, but it does have the authority to deem rate increases submitted by insurance companies as reasonable or unreasonable. After the review and negotiation process, the carriers submit their final rate 2020 increase information. The public is invited to provide comments on the rate changes. Please send any comments to Idaho Department of Insurance.

NOTE: This post re. North Carolina's 2020 individual market premium rate change is incomplete because it only includes one of the three carriers participating in NC's market (Blue Cross Blue Shield of NC). The rate change requests for Cigna and Centene haven't been released yet.

Normally I'd wait until I had data for the other two as well, but BCBSNC held around 95% of the state's Individual Market share last year, with Cigna holding the other 5% (Centene was a new entry to the market, so they didn't have any of it). I don't know how much the relative share has changed this year, but I'm assuming that BCBSNC still holds the lion's share of the total.

Blue Cross NC is decreasing 2020 Affordable Care Act (ACA) rates by an average of 5.2 percent for plans offered to individuals and an average of 3.3 percent for plans offered to small businesses with one to 50 employees. With this reduction, we take 238 million steps towards more affordable care in North Carolina.

The good news about the Ohio Insurnace Dept. is that they make it easy to find out which insurance carriers are participating on the ACA market and what the overall, weighted premium change is statewide.

The bad news is that they don't break out that statewide average by carrier rate changes, nor do they make it easy to find out the actual enrollment in the individual carriers...even on the SERFF database, they don't post the relevant filing forms until much later in the year, and tend to redact the critical data.

Still, the big number in the Buckeye State is a 7.0% average premium decrease year over year for 2020:

Insurance companies offering individual and small group health insurance plans are required to file proposed rates with the Pennsylvania Insurance Department for review and approval before plans can be sold to consumers. The Department reviews rates to ensure that the plans are priced appropriately -- that is, they are neither excessive (too high) nor inadequate (too low) -- and are not unfairly discriminatory.

Rates reflect estimates of future costs, including medical and prescription drug costs and administrative expenses, and are based on historical data and forecasts of trends in the upcoming year. In its review, the Department considers these factors, as well as factors such as the insurer's revenues, actual and projected profits, past rate changes, and the effect the change will have on Pennsylvania consumers. For more information on this process, watch our How Are Health Insurance Rates Decided?Opens In A New Window video.

Maine’s three providers of individual health insurance on the Affordable Care Act marketplace have revised their rate requests for 2020, significantly lowering their projected rates.

Previously, the insurers had sought modest average rate increases of 1 percent to 8 percent. Under the revised filings, two of the three insurers are now requesting decreases for individual plans, and the other is seeking an increase of less than 1 percent.

The Arkansas Insurance Dept. just posted their preliminary 2020 individual and small group market premium rate change requests. For the most part it's pretty straightforward: Individual market premiums are increasing about 2.3% statewide, while small group plans are going up 6.5% overall.

However, there's two interesting things to note about Arkansas' individual market: First, unlike most states where over 70% of enrollees do so through the ACA exchange, in Arkansas it's more like 20%, with nearly 80% are enrolled off-exchange. The main reason for this is the state's unique "Private Option" Medicaid expansion waiver, in which around 252,000 residents who would otherwise be enrolled in Medicaid itself are instead enrolled in enhanced ACA individual market policies...with the state paying for their premiums.

I wasn't expecting my analysis of Rhode Island's 2020 ACA premium changes to be of any particular interest; it's a small state with only two carriers offering individual market policies, after all, so there's not usually much to it.

A week or so ago I reported that Covered California had released their preliminary 2020 ACA individual market premium rate changes, with a record-low 0.8% average increase statewide. They detailed in the report how the combination of reinstating the ACA's individual mandate penalty and using that funding to provide additional financial subsidies to the enrollees lowered the average rate increases from 4.0% to 0.8%, saving unsubsidized enrollees around 3.2 points or $167/year on average.

Today, CoveredCA has posted more details about some of the specifics:

Covered California Releases Regional Data Behind Record-Low 0.8 Percent Rate Change for the Individual Market in 2020

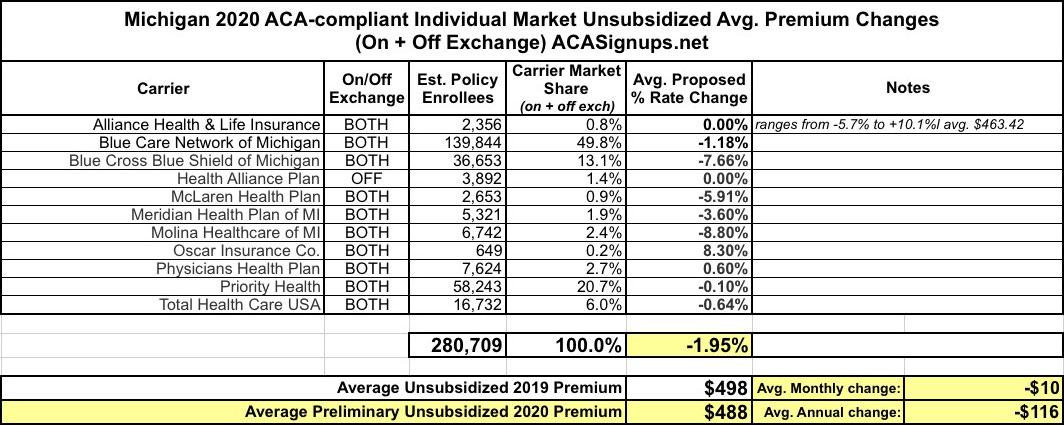

At the time, I concluded that the weighted average change marketwide was a 1.95% reduction in premiums compared to 2019, for around 281,000 Michiganders on the Indy market. This would mean roughly a $10 average premium reduction per unsubsidized enrollee per month, or $116 per year:

Polis Administration Projects 18.2% Average Decrease in Premiums for Individual Health Insurance Plans in 2020

Reducing health care costs has been a top priority for Polis.

DENVER (July 16, 2019) – Today, the Colorado Division of Insurance (DOI), part of the Department of Regulatory Agencies (DORA), announced that for the first time ever, Colorado health insurance companies that sell individual plans (for people who do not get their health insurance from an employer or government program) expect to reduce premiums by an average of 18.2 percent (-18.2%) over their 2019 premiums, provided the reinsurance program is approved by the federal government. These are the health insurance plans available on the Connect for Health Insurance Exchange, the state’s health exchange made possible by the Affordable Care Act (ACA).