Given how much I've been shouting from the rooftops about the importance of everyone #GettingCovered the past month or so, I'm fully aware of the irony of what I'm about to say:

My wife and I finally #GotCovered this morning at HealthCare.Gov.

We logged into our current account, reviewed our options and in the end settled on...pretty much the same Gold HMO we already have today. It's actually a slightly different policy--Blue Care Network of MIchigan elimiated the "HMO Select" option and replaced it with the "HMO Preferred" option. As far as we can tell, the only differences are the (unsubsidized) premium price, which shot up by about $300/month (ouch.) and the deductible, when went up from $500 to $1,000.

For us, we had two major decisions to make: Gold vs. Silver...and (assuming we had gone with Silver), On-Exchange vs. Off-Exchange.

Until today, I operated under the assumption that my home state of Michigan was among the 18 states which took the "Silver Load" approach to dealing with the Cost Sharing Reduction (CSR) cut-off by the Trump administration. Reviewing the SERFF rate filings of the various carriers participating in the individual market, it looked like most of them were loading the CSR cost onto both on and off-exchange Silver plans. I didn't check every single carrier, but that seemed to be the trend, so I filed the state under "Silver Load".

I'm signing up for a plan off the exchange with Priority Health in Michigan. ON-Exchange, the plan is $365 a month, but off exchange (directly from their website), the price is $300 per month. I don't qualify for a subsidy, but it's still cheaper than my 2017 plan with BCBSM. That was the Multi-State Plan in Region 7 with Dental and Vision.

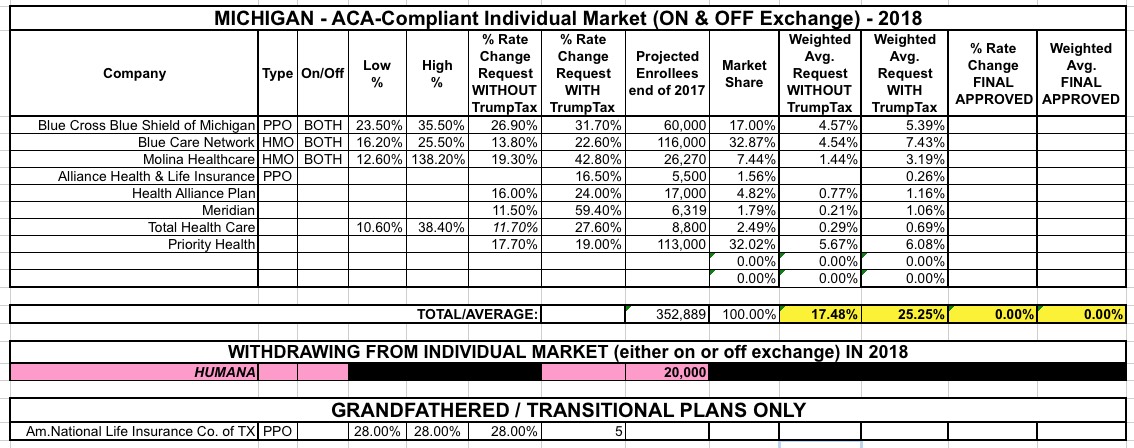

I'm still missing final 2018 rate data for 6 states, but in the meantime I'm also doing some cleanup of some of the states I thought I already had final data for. Today both my home state of Michigan as well as Washington State released their official, approved increase tables.

However, I do give the Michigan Dept. of Insurance & Financial Services huge credit for making it incredibly easy for me to plug their data in. Look at that...they list all carriers, whether they sell on or off exchange, the exact average rate increases, and even include the number of affected enrollees, which is usually the hardest number for me to track down. Thanks, MI DIFS!!

IMPORTANT: I need to stress that I am not in any way supportive of having CSR reimbursement payments cut off. I've written dozens of blog posts for the past year and a half about the danger this poses and I've repeatedly explained why this is a reckless, dangerous move by Donald Trump, I've even repeatedly noted how incredibly easy it would be to resolve the issue with a simple, one paragraph bill. Having said that, assuming the payments do stop being made, this is an explainer of how to turn it into a "lemonade out of lemons" situation for as many people as possible. Make no mistake, however: Millions of people will still be hurt by this...just not the people Trump thinks he's hurting.

As in most states, the Michigan Dept. of Financial Services, seeing the potential writing on the wall, sent out a memo to all individual market insurance carriers instructing them to submit two different sets of rate filings for 2018: One assuming CSR payments would continue, the other assuming they won't:

Just a few days ago I noted that Michigan's Dept. of Insurance issued the semi-final 2018 individual market rate changes for the 10 carriers offering indy policies in the state (9 of which are on the ACA exchange; one of them is only offering plans off-exchange). At the time, the breakout was roughly 16.8% average increases assuming CSR payments are made next year or 26.8% assuming they aren't made.

A major health insurer is leaving Michigan’s individual marketplace, ending its policies offered here under the Affordable Care Act as the federal government slashes funding for enrollment and outreach groups.

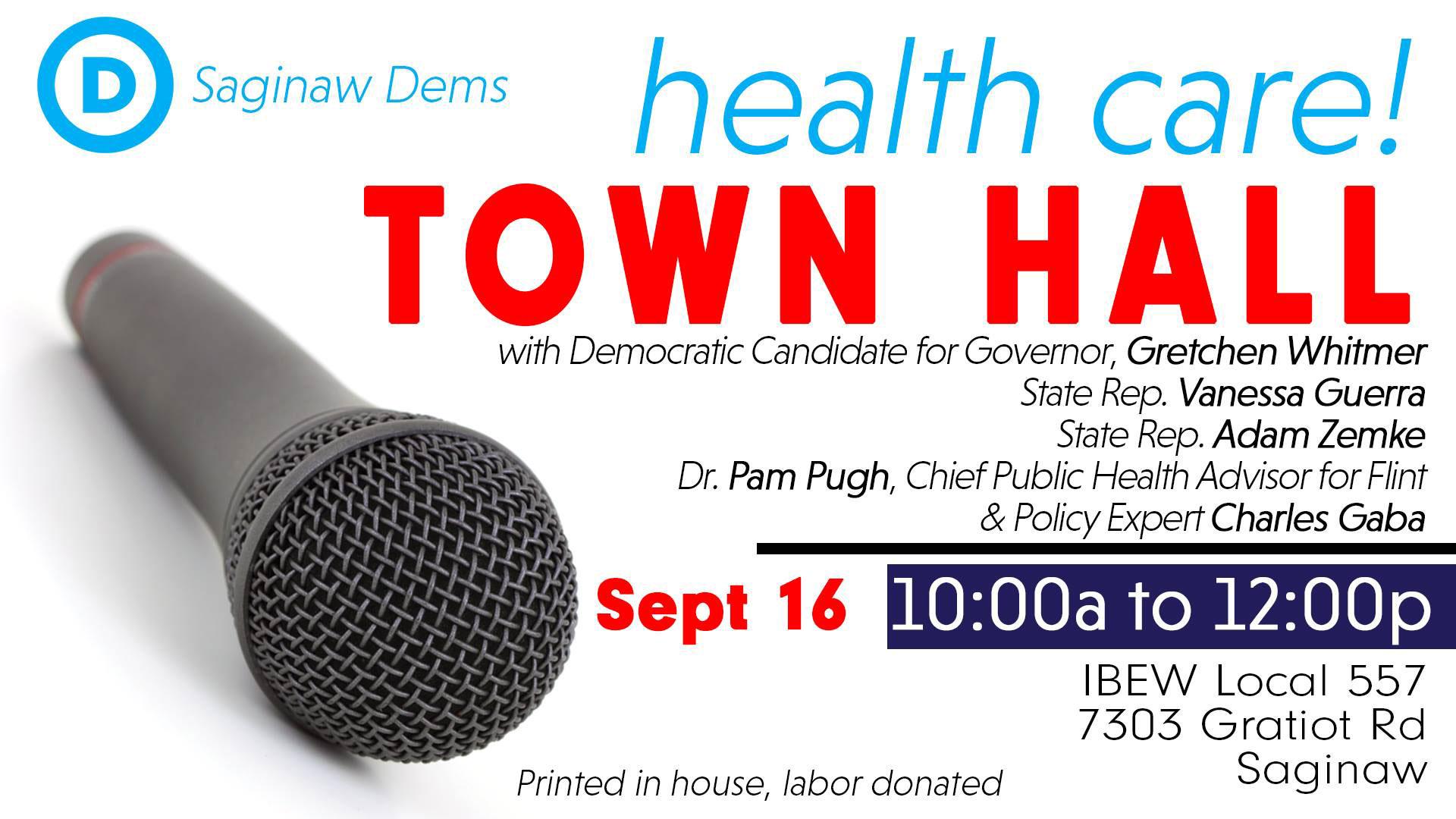

Hey Michigan Residents! Do you live in the SAGINAW area?

If so, come on out to Saginaw on Saturday, September 16th, and join former State Senator (and current gubernatorial candidate) Gretchen Whitmer, State Representatives Vanessa Guerra & Adam Zemke, Chief Public Health Advisor for Flint Dr. Pam Pugh and myselfas we explain what the latest craziness is regarding the ACA, the GOP attempts to repeal and/or sabotage it and healthcare policy in general from 10:00am - 12:00pm at IBEW Local 557 at 7303 Gratiot Road.

Michiganders purchasing health insurance through the federal marketplace will see an average rate increase of 27.6 percent in 2018, the Michigan Department of Insurance and Financial Services announced Friday.

One reason for the big increase: Uncertainty over whether President Trump will continue to fund Cost-Sharing Reduction payments, which subsidize plans for low- and moderate-income households.

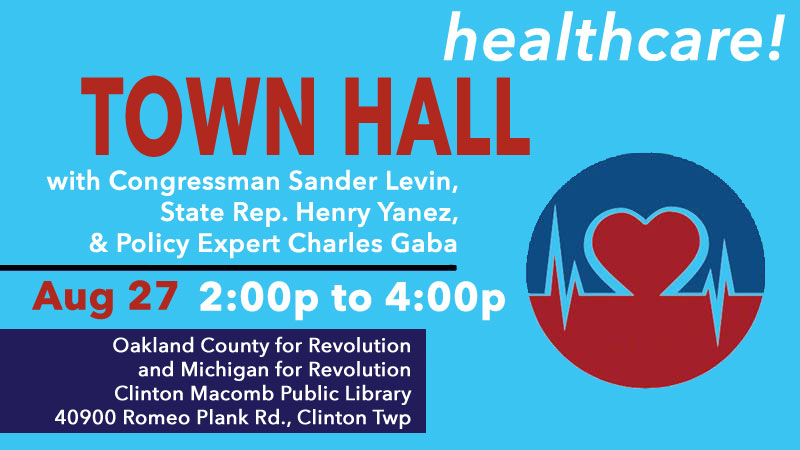

Hey Michigan Residents! Do you live in the Clinton Township area?

If so, come on out on Sunday, August 27th, and join Congressman Sander Levin, State Representative Henry Yanez and myself as we explain what the latest craziness is regarding the ACA, the GOP attempts to repeal and/or sabotage it and healthcare policy in general from 2:00pm - 4:00pm at the Clinton Macomb Public Library: