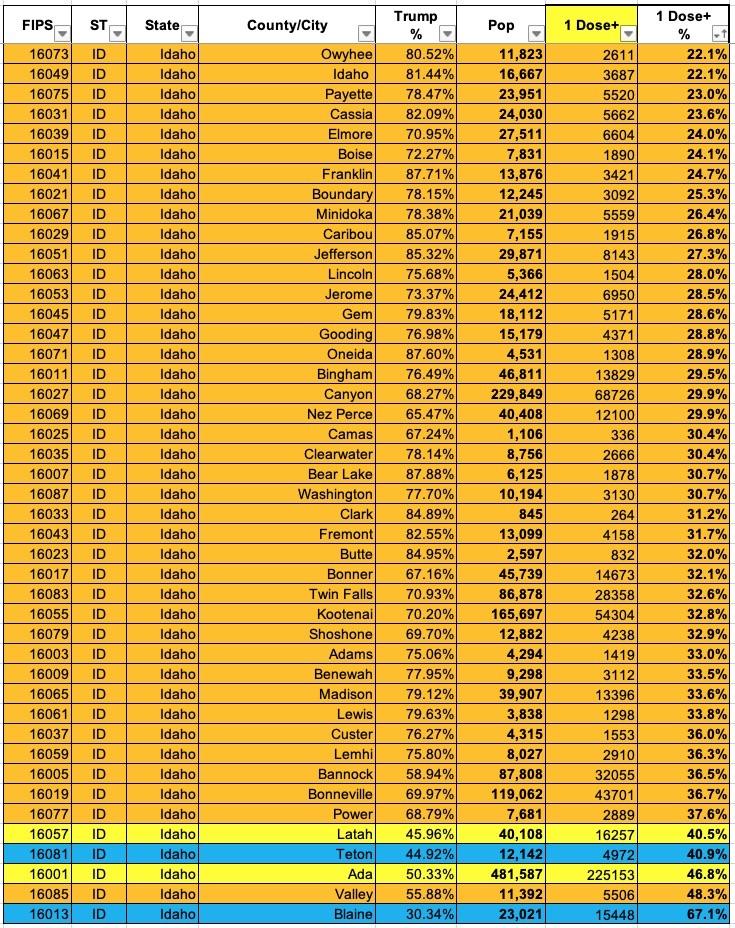

Now that I've developed a standardized format/layout & methodology for tracking both state- and county-level COVID vaccination levels by partisan lean (which can also be easily applied to other variables like education level, median income, population density, ethnicity, etc), I've started moving beyond my home state of Michigan.

Here's Louisiana (reminder: Louisiana calls them Parishes, not Counties):

Louisiana joins the disturbingly-long list of states where the 2021 individual & small group market rate filings are either completely missing or heavily redacted, thus making it impossible for me to break out the market share by carrier and thus running a weighted average rate change.

I really hope this trend is reversed in the future, whether via HHS transparency regulations or through legislation.

In any event, the unweighted average rate increase for the Louisiana indy market is around 6.9%, and for the small group market it's roughly 5.2%.

Louisiana's 2020 Presidential primary was scheduled for April 4th, but the other day Democratic Governor John Bel Edwards and Republican Secretary of State Kyle Ardoin agreed to reschedule it for June 20th...which is actually later than the last previously-scheduled primary in the U.S. Virgin Islands on June 6th:

The presidential primary elections in Louisiana slated for April will be delayed by two months, the latest in a series of dramatic steps government leaders have taken to slow the spread of the new coronavirus.

Secretary of State Kyle Ardoin, Republican, and Gov. John Bel Edwards, a Democrat, both said Friday they would use a provision of state law that allows them to move any election in an emergency situation to delay the primary.

The presidential primary elections, initially scheduled for April 4th, will now be held June 20th. Ardoin said in a press conference he does not know of any other states that have moved elections because of the new coronavirus, or COVID-19.

TO CLARIFY: In pretty much all cases below, when it comes to restaurants, "shut down" refers to dining in only; they're pretty much all still allowing delivery/carryout orders.

As my regular readers know, I've been a strong proponent of encouraging states to pass laws locking in as many ACA "blue leg" protections as possible in the event that the ACA itself is actually struck down by the idiotic #TexasFoldEm lawsuit (again: the ruling by the 5th Circuit Court of Appeals is due to drop at any time).

However, I've also tried to make it clear that there would be a trade-off involved: If you're going to lock in all of those "Blue Leg" protections (Guaranteed Issue, Community Rating, Essential Health Benefits, No Annual/Lifetime Caps, etc), that will mean that the premiums/deductibles will be higher than they are without those protections.

This is precisely why so-called "short-term, limited duration" policies (aka #ShortAssPlans) and other non-ACA compliant policies cost so much less at the front end...they cherry pick their enrollees and don't cover the more expensive treatments many people require.

Personally, I still think states should lock in those protections anyway, since there's only two ways this can play out:

There's only 3 states which are looking at double-digit average unsubsidized premium increases on the 2020 ACA individual market: Indiana, Vermont and Louisiana.

There's actually only 3 carriers offering individual market plans in Louisiana, but there's seven listings because two of the carriers have broken out their submissions into several different product lines. Overall, HMO LA, LA Health Service & Indemnity (Blue Cross Blue Shield of LA) and Vantage Health Plan are requesting average premium increases of 11.7% statewide.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

Huh. This is interesting...after a couple dozen states with near-flat or even reduced 2020 premiums, Louisiana is just the third state I've come across where the carriers are seeking double-digit rate increases for next year.

There's actually only 3 carriers offering individual market plans in Louisiana, but there's seven listings because two of the carriers have broken out their submissions into several different product lines. Overall, HMO LA, LA Health Service & Indemnity (Blue Cross Blue Shield of LA) and Vantage Health Plan are requesting average premium increases of 11.7% statewide.

I should note that there's also one odd listing (see second screenshot below), from UnitedHealthcare. It claims to be for off-exchange ACA-compliant individual market plans, but two things about it make no sense:

On Tuesday, May 21, Governor John Bel Edwards issued an executive order launching the Protecting Health Coverage in Louisiana Task Force after efforts to have protections offered to Louisianans with preexisting conditions repealed.

With the idiotic #TexasFoldEm lawsuit scheduled for oral arguments by the 5th Circuit Court of Appeals this summer, many states have been scrambling to replicate ACA protections for those with pre-existing conditions at the state level, including California, Colorado, Connecticut, Hawaii, Maryland, Nevada, New Mexico and more.

In a red state like Louisiana, unfortunately, it's not so easy...the state has a Democratic Governor, but both the state House and Senate are solidly controlled by Republicans. In addition, the Governor, John Bel Edwards, is up for re-election this November, making everything politicized, thus making it likely impossible to get anything useful through this year. Still, Gov. Edwards is trying to do something to mitigate the problem:

{kind=link}