Every year, I spend months painstakingly tracking every insurance carrier rate filing (nearly 400 for 2025!) for the following year to determine just how much average insurance policy premiums on the individual market are projected to increase or decrease.

Carriers tendency to jump in and out of the market, repeatedly revise their requests, and the confusing blizzard of actual filing forms sometimes make it next to impossible to find the specific data I need.

I really only need three pieces of information for each carrier:

This is gonna be one of the stranger references I've made on this site, but bear with me.

Back in 1996 there was an HBO movie called "The Late Shift" which told the story of the Late Night TV show battle between David Letterman and Jay Leno over who would succeed Johnny Carson as host of The Tonight Show. As stupid as this may sound today, this was actually a Really Big Deal in the '90's...one of those absurd pop culture stories which dominated the headlines and the tabloids for several years.

The movie itself was decent, with some interesting casting including Kathy Bates and Treat Williams, but nothing special. The main problem is that the audience is expected to root and feel sympathy for a couple of dudes who were already rich & famous and who would both continue to be rich & famous no matter how the story played out. The stakes weren't exactly the fate of the world, is what I'm saying.

9/29/25: Welcome Paul Krugman subscribers! I greatly appreciate the shoutout by him but should add the following clarification:

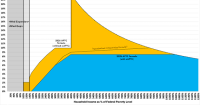

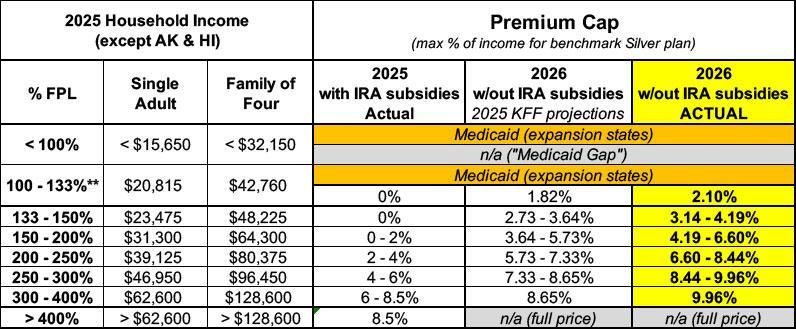

Regarding the chart below which he reposted comparing the original ACA subsidy scale to the current version: You probably think that if the enhanced subsidies expire it will revert back to the original version, which would be bad enough. In fact, however, the Trump Regime has also made THAT version even worse, like so:

Ever since the MAGA Murder Bill (officially H.R. 1, the so-called "One Big Beautiful Bill Act") was passed by Republicans in the U.S. Senate & House and signed into law by Donald Trump a few days ago, I've seen a growing conventional wisdom taking hold on social media: People keep claiming that either all, "nearly all" or at least "most of" the budget cuts & other gutting of various programs and departments won't actually kick in until after the November 2026 midterms.

Now, don't get me wrong--most of those making these claims are well-intentioned; they're saying this cynically, to underscore how disingenuous Congressional Republicans are by back-loading the pain until the midterms are safely in their rearview mirrors. And, to be fair, much of the damage won't being until well after next November.

Over at The New Republic, Greg Sargent has taken this thinking one step further, noting that by delaying so much of the ugliness of the new law until 2027 or beyond...

With the 2026 ACA Open Enrollment Period officially starting on November 1st, and with millions of ACA enrollees being bombarded with scary letters from their insurance carriers and headlines warning of massive premium hikes, residents of six states* (as of this writing) can already enter their own household information to find out how much their net health insurance premiums are going to increase starting January 1st, 2026:

Whether the data posted since January 20, 2025 is accurate or not, I can't say for certain, but at least they're updating it...and so far, at least, I don't see anything in their monthly reports which is setting off any obvious red flags.

In any event, according to the latest report, as of June 2025:

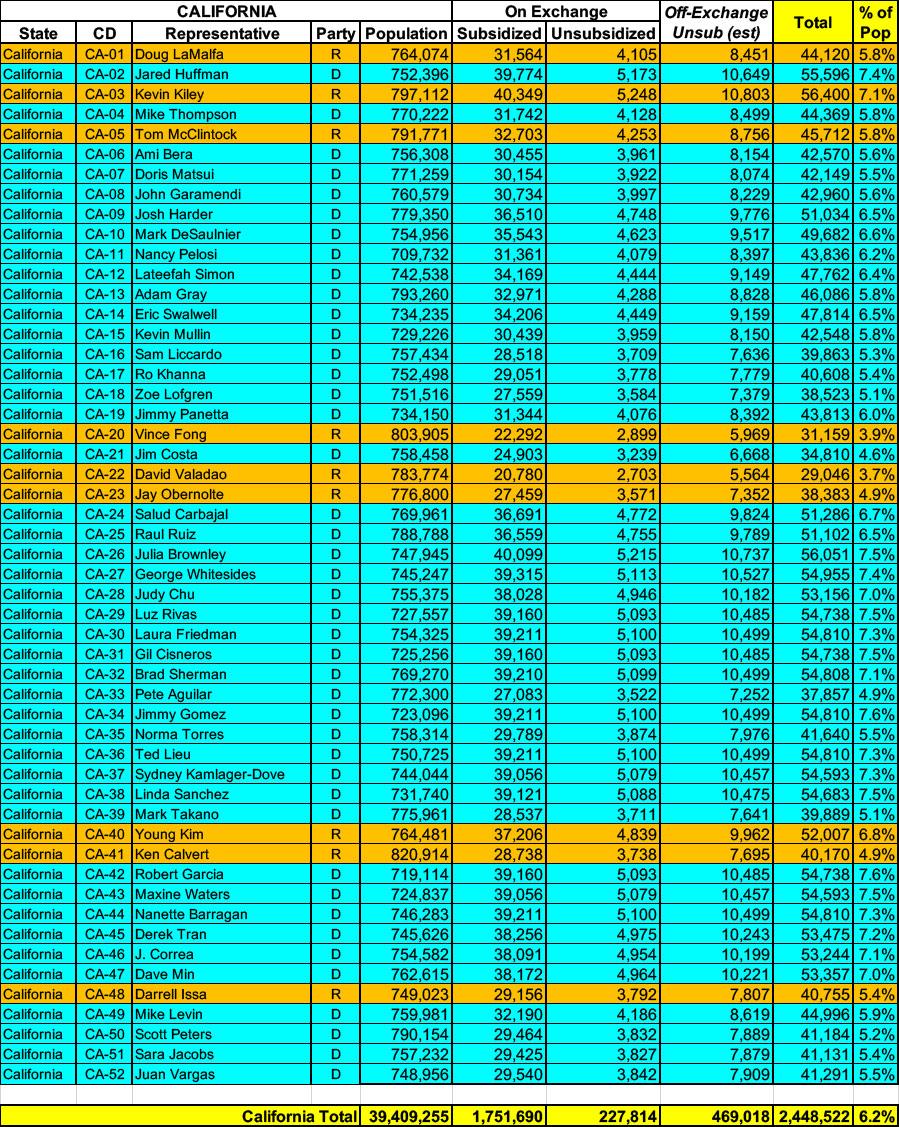

California has ~1.98 MILLION residents enrolled in ACA exchange plans, over 88% of whom are currently subsidized. They also have an estimated ~470,000 off-exchange enrollees. Combined, that's over 2.4 million people, or 6.2% of their total population.

Twelve years ago, the Wall St. Journal ran a story about the impact of the American Taxpayer Relief Act of 2012, a sweeping tax bill signed into law by President Obama which locked in the Bush tax cuts for lower & middle-class households while allowing them to expire on schedule for wealthier Americans:

A compromise measure, the Act gives permanence to the lower rate of much of the Bush tax cuts, while retaining the higher tax rate at upper income levels that became effective on January 1 due to the expiration of the Bush tax cuts. It also establishes caps on tax deductions and credits for those at upper income levels. It does not tackle federal spending levels to a great extent, rather leaving that for further negotiations and legislation. The American Taxpayer Relief Act passed by a wide majority in the Senate, with both Democrats and Republicans supporting it, while most of the House Republicans opposed it.

(Aetna/CVS is pulling out of the entire individual market nationally)

Anthem Blue Cross of CA (DMHC)

This is a rate filing for the Individual market ACA‐compliant plans offered by Anthem Blue Cross (Anthem). The proposed rates in this filing will be effective for the 2026 plan year beginning January 1, 2026, and apply to plans both On‐Exchange and Off‐Exchange.

Anthem will continue to participate in its 2025 marketplace footprint consisting of rating areas 1-10 and 12-14 with EPO plans and rating areas 11 and 15‐19 with HMO plans.