As always, the Texas individual and small group markets are pretty messy. For starters, they have up to 20 individual market carriers depending on the year, along with over a dozen small group market carriers some years (this year they're at 17 and 8 respectively).

On top of that, as is also the case in some other states, some of the names of the insurance carriers can be confusing as hell. There's the "Insurance company of Scott & White" which seems to have changed its name to "Baylor Scott & White Insurance Co.," which isn't to be confused with "Scott & White Health Plans" and so on.

I was only able to acquire hard enrollment data for five of the carriers on the individual market this year, and one of those doesn't really count since they're brand new and don't have any (Wellpoint Insurance Co.). For another 11 of them the rate filings include the number of policyholders but not the actual number of covered lives; for those I'm using an average 1.4x multiplier, based on the actual multiplier found in the carriers I have both numbers available for.

Tennessee's preliminary 2025 individual & small group market health insurance rate filings are now available. Unfortunately, I can't find any unredacted filing forms for any of them (and in fact most of the rate filings aren't showing up in the SERFF database at all).

For the most part there's not much to see at first glance: Requested rate changes range from a 1.3% drop to a 3.9% increase on the individual market and from a 9.7% to 11.2% increase for small group plans. The unweighted averages are +1.4% and +10.6% respectively.

However, it also looks like several carriers are dropping out of each market in Tennessee: Alliant and US Health & Life (Ascension) don't show up on the federal Rate Review database for the individual market, while Aetna and CIGNA are missing for small group listings.

Assuming the exchange-based market makes up roughly 85% of total individual market enrollment in Tennessee, the total indy market should be around 628,000 people.

Pretty straightforward in the Mount Rushmore state. Three carriers on the individual market; around 56.4K enrollees total. The weighted average rate change across all three is +2.3% if approved as is.

Note that I've added a new feature to my rate change spreadsheet this year: I've started including the on exchange effectuated enrollmentas well as the subsidized on exchange enrollment as of February for every state. This will allow me to calculate the percent of the total individual market which is receiving ACA subsidies...at least in states where I'm able to figure out what total off-exchange enrollment is (typically only around half of them).

In South Dakota, for instance:

95.7% of on exchange enrollees are subsidized (49,250 / 51,416)

87.2% of the total market is subsidized (49,250 / 56,457)

On exchange enrollment makes up around 91% of the total individual market

For the small group market, there are five carriers this year; Medica Insurance Co. appears to be pulling out of the state. The weighted requested average rate change is a 2.8% increase.

I got so far behind on my annual rate filing project that some of the states have started issuing their APPROVED changes before I got around to analyzing the REQUESTED rate changes. Ah, well...

LINSEY DAVIS: This is now your third time running for president. you [Trump] have long vowed to repeal and replace the Affordable Care Act, also known as Obamacare. You have failed to accomplish that. You now say you're going to keep Obamacare. Quote, unless we can do something much better. Last month you said, quote, we're working on it. So tonight, nine years after you first started running, do you have a plan and can you tell us what it is?

Oklahoma is another state where I have no access to the actual enrollment data--all I have to go by are the average requested rate changes for each carrier on the individual and small group markets. As a result, the averages for each market are unweighted.

For individual market plans, that unweighted average is a slight decrease of 0.7%, though the carriers range from as low as a 12% drop to as high as a 10% increase.

It's worth noting that BlueLincs HMO, which was only added to the OK individual market last year, is already being removed from it. In fact, as shown below, it looks like BlueLincs was a special line of policies offered at the point of a regulatory gun; apparently Blue Cross was required to create it as an option for group coverage members who move off of employer coverage. However, that regulation was apparently changed shortly thereafter, and no one ever actually enrolled in a BlueLinc plan anyway, so that's that.

For the small group market, average requested rate hikes range from as little as 4.0% to as much as a 15.2. The unweighted average is 8.3%

1 in 7 U.S. residents covered through Affordable Care Act health insurance marketplaces over the last decade, with all-time high enrollment under Biden-Harris Administration

WASHINGTON – Today, the U.S. Department of the Treasury released new data showing that nearly 50 million Americans, or 1 in 7 U.S. residents, have been covered through the Affordable Care Act marketplaces since January 2014. Under the Biden-Harris Administration, which has lowered the cost of marketplace coverage by expanding the premium tax credit, the number of Americans covered through the marketplaces has significantly increased, reaching an all-time high of 20.8 million following open enrollment for 2024—18.2 million Americans have enrolled for the first time since January 2021.

As a result, I've been able to put together a weighted average requested rate increase for the individual market, which comes in at +3.9%.

For the small group market, I have to go with an unweighted average of +12.0%. It's also worth noting that it looks like one of Aetna's divisions is pulling out of the OH small group market, as are two fof the 4 (!) UnitedHealthcare divisions and possibly AultCare, although I'm not sure about that one.

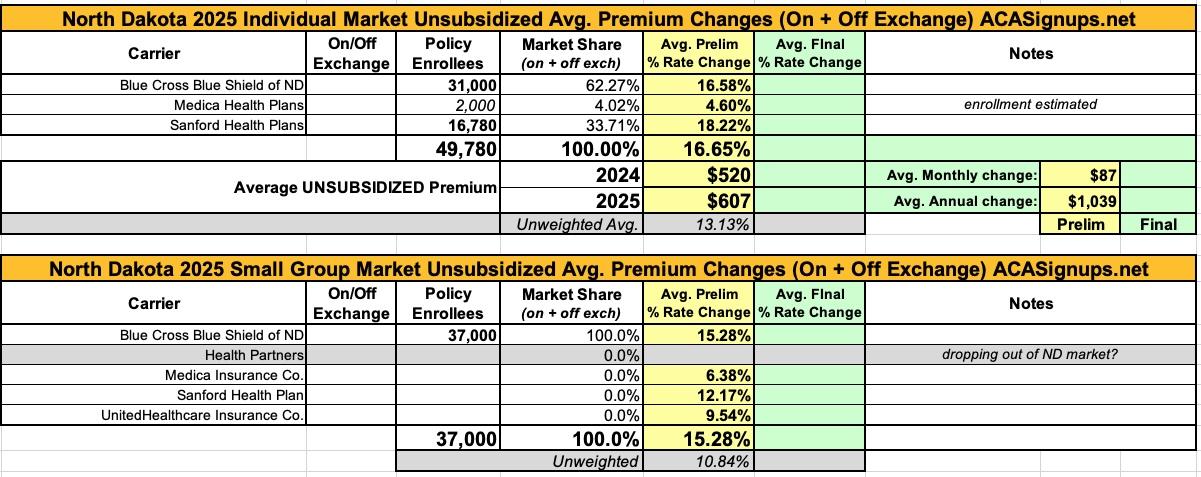

North Dakota only has 3 carriers participating in their individual health insurance market and four in their small group market, since it appears that Health Partners will be pulling out of the latter next year.

For the indy market, the weighted average premium increase being requested is a painful 16.7%, although this may be off slightly due to Medica's enrollment number being a rough estimate (last year's total ND market was only 45,000 people; I'm assuming Medica only has around 2,000 enrollees this year).

For the small group market, I only have the unweighted average rate hikes, which come in at 10.8%.

New Jersey individual & small group market carriers are asking for unweighted average rate increases of 7.3% and 4.5% respectively for 2025. However, the unweighted averages don't tell the whole story--the carriers are asking for rate hikes ranging from as low as 3.8% to as high as 16.2% on the individual market, and from as low as an 18.8% reduction to a 12.3% increase for small group plans.

As is the case with far too many states these days, most of the rate filing memorandums are heavily redacted in New Jersey, making it nearly impossible to get ahold of the actual enrollment numbers, which means I have no way of running a weighted average on either market.

I should note that the 433,000 estimate for New Jersey's total individual market is based on the assumption that 90% of it is via the ACA exchange, with only 10% being enrolled off-exchange.