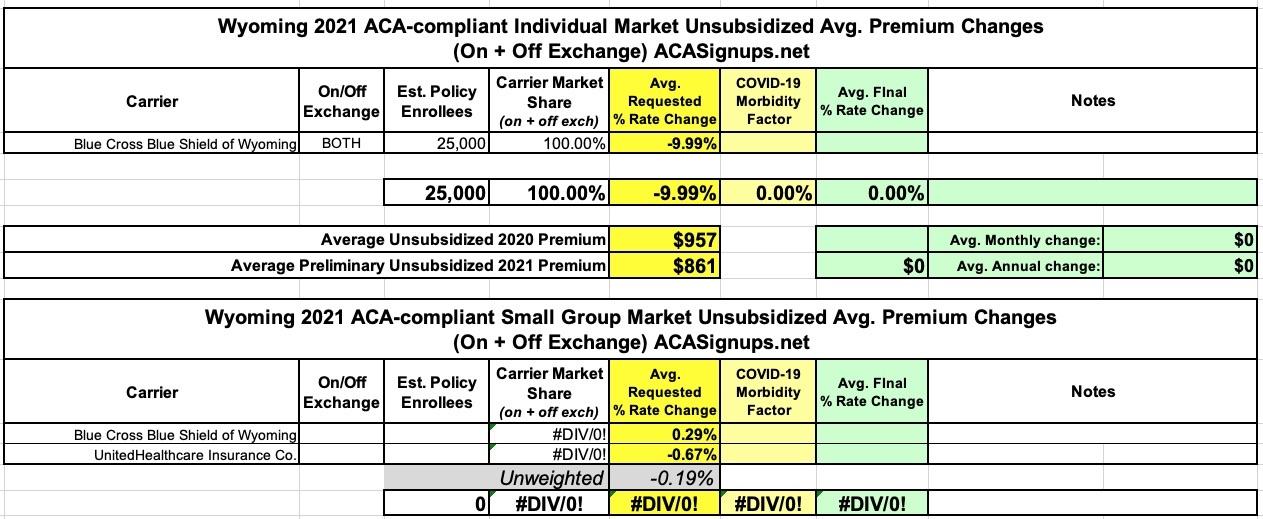

Not much to this one: Wyoming has just a single carrier selling ACA-compliant individual market policies to their 577,000 residents, Blue Cross Blue Shield...which, after raising rates 1.6% for 2020 is now reducing them by a solid 10% on average for 2021. The ~25,000 enrollment figure is an estimate.

For the small group market there are two carriers: BCBSWY and UnitedHealthcare, asking for an unweighted average rate reduction of 0.2% (I don't have a clue how many enrollees either one has).

First, CA's Small Group Market premiums are increasing by just 1.5% in 2021 (the lowest average increase since the ACA passed)

Second, CA's Individual Market premiums are increasing by just 0.6% on average in 2021 (identical to the preliminary rate requests)

Third, that Open Enrollment technically already started back on October 1st...sort of.

The official launch of Open Enrollment in every state isn't until November 1st, but for the past couple of years California has allowed current enrollees already in their system to actively renew/re-enroll for the upcoming year starting on October 15th. This year, it turns out they quietly moved that date back even earlier--current enrollees have been able to re-enroll starting as early as October 1st! I don't recall them ever making a big public announcement about this; I sort of stumbled upon it by accident.

Any music fan eager to bulk up their collection in the ’90s knew where to go to grab a ton of music on the cheap: Columbia House. Started in 1955 as a way for the record label Columbia to sell vinyl records via mail order, the club had continually adapted to and changed with the times, as new formats such as 8-tracks, cassettes, and CDs emerged and influenced how consumers listened to music. Through it all, the company’s hook remained enticing: Get a sizable stack of albums for just a penny, with no money owed up front, and then just buy a few more at regular price over time to fulfill the membership agreement. Special offers along the way, like snagging discounted bonus albums after buying one at full price, made the premise even sweeter.

The data below comes from the GitHub data repositories of Johns Hopkins University, except for Rhode Island, Utah and Wyoming, which come from the GitHub data of the New York Times due to the JHU data being incomplete for these three states. Some data comes directly from state health department websites.

Note that a few weeks ago I finally went through and separated out swing districts. I'm defining these as any county which where the difference between Donald Trump and Hillary Clinton was less than 6 percentage points either way in 2016. There's a total of 198 Swing Counties using this criteria (out of over 3,200 total), containing around 38.5 million Americans out of over 330 million nationally, or roughly 11.6% of the U.S. population.

With these updates in mind, here's the top 100 counties ranked by per capita COVID-19 cases as of Saturday, October 10th (click image for high-res version). Blue = Hillary Clinton won by more than 6 points; Orange = Donald Trump won by more than 6 points; Yellow = Swing District

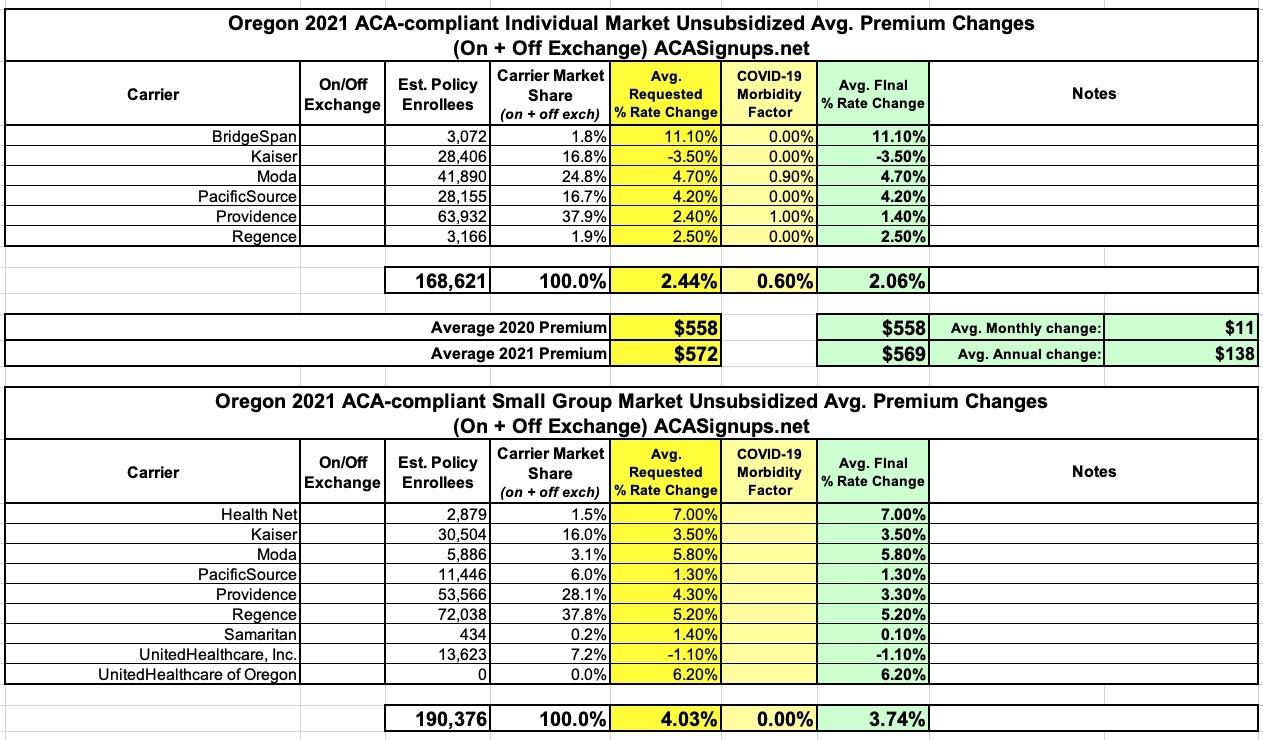

Way back in May (a lifetime ago!), the Oregon Insurance Dept. was one of the first states to release their preliminary 2021 ACA premium rate filings for the individual and small group markets.

At the time, the carriers were asking for a weighted average 2.4% increase on the indy market (OR DOI put it at 2.2%) and a 4% increase for small group policies.

They issued some slightly revised rates later on in the summer, and sometime in August I believe they issued the final approved rates...which are just slightly lower on a few carriers.

In the end, 2021 Oregon enrollees are looking at weighted average premium hikes of 2.1% for indy plans and 3.7% for small group policies:

Back in early August, Covered California issued an extensive analysis of their upcoming 2021 individual market offerings, including the preliminary weighted average premium rate changes of just a 0.6% increase. Officially, this was just the average of the preliminary requests; the approved rates were presumably forthcoming at a later date.

Well, the 2021 Open Enrollment Period has technically already started in California...while new enrollees still have to wait until November 1st, current CoveredCA enrollees have apparently been able to re-enroll for 2021 since October 1st! (In previous years, CoveredCA opened up the renewal period starting on Oct. 15th)

Oklahoma Consumers to Have More Health Options for 2021 ACA Plans

OKLAHOMA CITY – Insurance Commissioner Glen Mulready announced today the 2021 preliminary rate filings for health insurance plans under the Affordable Care Act (ACA). Insurers that currently offer coverage through the Oklahoma Marketplace filed plans requesting average statewide increases of 2.7 percent.

In August, the Nevada Insurance Dept. issued their preliminary 2021 rate filings for the individual and small group markets. Unfortunately, while the filing summaries were easy to find, the actual enrollment numbers weren't. As a result, I only had the department's press release to go on for the weighted overall average on the individual market, and I had to go with an unweighted average for the small group market.

Fortunately, now that the NV Insurance Dept. has issued the approved 2021 rates, they've also added more detailed summaries for both markets, meaning I have effectuated enrollments for every carrier. This allows me to run a proper weighted average rate change across both:

Back in June, Maryland's Insurance Dept. posted the preliminary 2021 rate requests for the individual and small group markets. At the time, carriers were seeking an average 4.8% premium reduction on the individual market and a 5.1% average increase for the small group market.

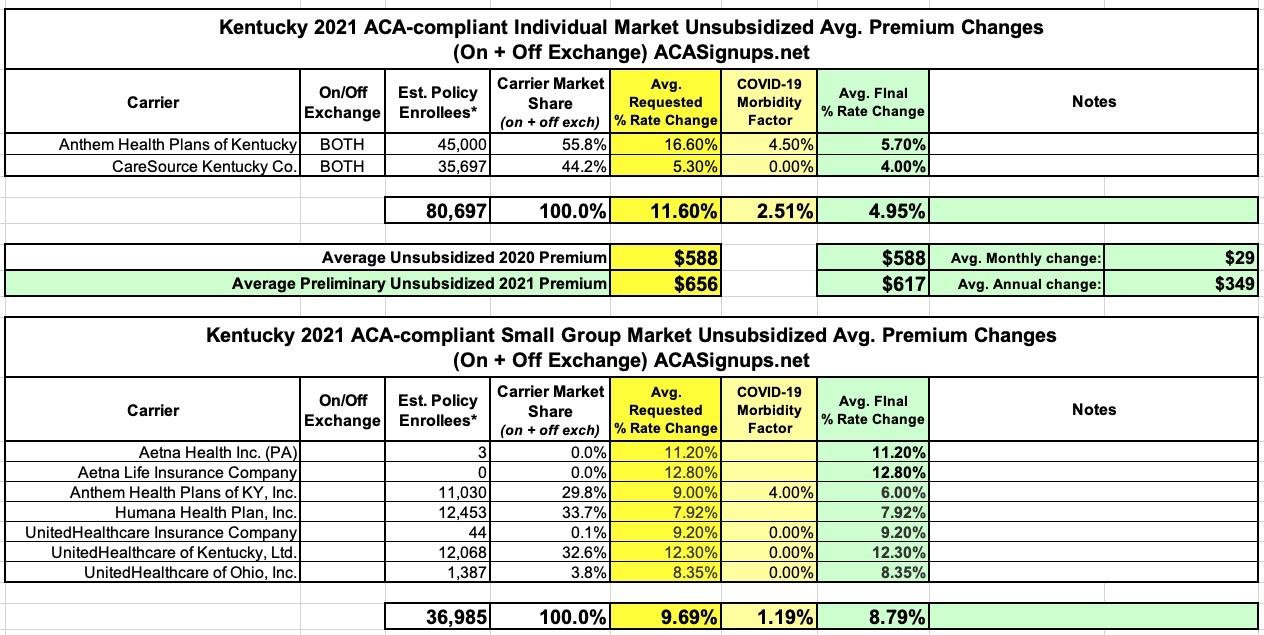

In early August, the Kentucky Insurance Dept. posted preliminary 2021 rate filings for the individual and small group markets. At the time, the carriers were requesting average increases of 11.6% on the individual market (unusually high this year) and 9.7% for the small group market.