The Deferred Action for Childhood Arrivals (DACA) program was created to protect eligible young adults who were brought to the U.S. as children from deportation and to provide them with work authorization for temporary, renewable periods. As of December 31, 2022, there were roughly 580,000 active DACA recipients from close to 200 different countries of birth residing all over the U.S.

While individuals with DACA status can be authorized to work, they remain ineligible for many federal programs, including health coverage through Medicaid, the Children’s Health Insurance Program (CHIP), and the Affordable Care Act (ACA) health insurance Marketplaces. These restrictions result in higher uninsured rates among DACA recipients, contributing to barriers accessing health care.

Denver, Colo.– Connect for Health Colorado, the state’s official health insurance marketplace, is celebrating a record-breaking open enrollment period, with 256,051 Coloradans enrolled in health coverage that begins Jan. 1.

To date, the number of Coloradans who enrolled in health insurance plans for plan year 2025 is more than the total number of people (237,107) who enrolled through Connect for Health Colorado last year.

The official total I was sent is 256,051 Qualified Health Plan (QHP) selections to date, which is 21% more than C4HCO had at the same point last year and 8% higher than last year's final Open Enrollment Period tally.

December 16, 2024—Massachusetts residents have just one week left before the deadline to get health insurance for the new year, but still have the opportunity to make sure they can go into 2025 with coverage that affordably takes care of their health and wellness needs.

Open Enrollment started Nov. 1 and runs through Jan. 23. However, most people who need health insurance—including people who have recently moved to Massachusetts, who are participants in the state’s growing gig and creative economies, or who simply haven’t had health coverage in many months or years—want coverage to start the new year. The deadline for a plan starting Jan. 1 is Monday, Dec. 23.

I don't really write a whole lot about the Small Group Market, which consists of employer-sponsored healthcare coverage for companies with fewer than either 50 employees (in a few states the small group market serves companies with up to 100 employees).

The bulk of my small group market analysis is limited to my annual Rate Change project, where I break out & analyze annual premium rate changes for carriers in both the individual and small group markets. However, even then, while I try to run the numbers for the small group market in each state, I usually don't have much to say about it, and a lot of states don't provide actual carrier-level enrollment data publicly anyway, which means I can usually only run an unweighted average rate change at best.

Small-group plans effective since January 2014 are required to fully comply with Affordable Care Act (ACA) rules that apply to individual and small-group health plans.

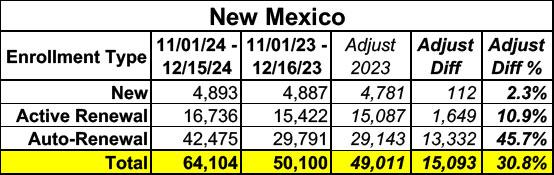

Not only is New Mexico's exchange enrollment up a whopping 31% vs. the same point last year, it's actually already 13.5% higher than the 2024 OEP's final total of 56,472!

On December 13, 2024, the State was informed by its vendor, Deloitte, that there was a major security threat to RIBridges, the system that manages many of the state’s social services programs. Additionally, Deloitte confirmed that there is a high probability that a cybercriminal has obtained files with personally identifiable information.

This is the State of Rhode Island’s dedicated webpage for all the latest information on the breach. We understand this is an alarming situation, and we appreciate your patience as we investigate this matter. We will continue to navigate this challenge together.

Update 12/16/24: 5 Steps to Protect Your Personal Information Today

Governor McKee issued a public service announcement to encourage potentially impacted Rhode Islanders to take 5 steps to protect their personal information today. (see video above)

Update 12/15/24: RIBridges Data Breach Hotline Now Available

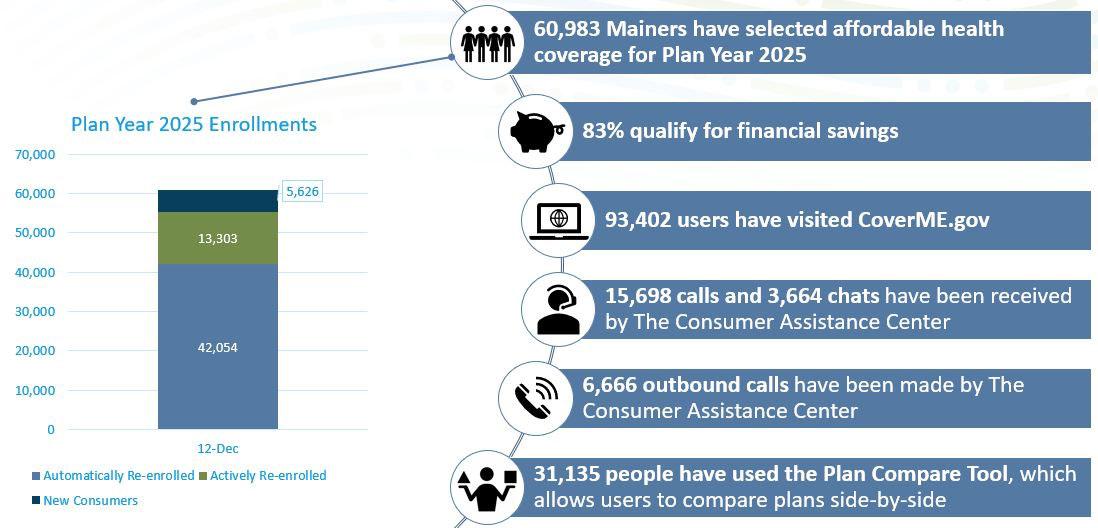

The Maine Department of Health and Human Services (DHHS) Office of the Health Insurance Marketplace (OHIM) will release biweekly updates on plan selections through CoverME.gov, Maine’s Health Insurance Marketplace.

Plan selections provide a snapshot of activity by new and returning consumers who have selected a plan for 2025. “Plan selections” become “enrollments” once consumers have paid their first monthly premium to begin insurance. These numbers are subject to change as consumers may modify or cancel plans after their initial selection.

The deadline to select a plan for coverage beginning January 1, 2025 is December 15, 2024. Consumers who select a plan between December 16, 2024 and January 15, 2025 will have coverage beginning February 1, 2025.

GOP Reportedly Rejects APTC Offer; Wyden Signals He’s Open To Compromise

Senate Finance Chair Ron Wyden (D-OR) Tuesday suggested he may be open to changes to the enhanced Affordable Care Act premium tax credits in order to get Republicans on board an extension of the policy that has been in effect since 2021 and will expire at the end of 2025 without congressional action.

Democrats had proposed one way of giving a hand to families that have fallen through the cracks when it comes to health care, Wyden said of the APTC extension. “If Republicans don’t care for that approach, they oughtta come back and say, ‘here’s what we’d like to do instead,” or else we'll just make the assumption they’re not interested,” he said.

After an eventful month and a half, I’m impressed with Connect for Health Colorado’s growth. We’re seeing about 20 percent more health insurance enrollments over this time last year, an increase made even more impressive considering the enrollment record we achieved last year. I’m thankful to see that enrollments are outpacing previous years, as we announced last week on Get Covered Day, Dec. 5th.

My greatest thanks goes to you, our valued stakeholders, who diligently work to increase access, affordability, and choice for health care coverage in Colorado. As we face a new year of discussions about it all, real Coloradans are still able to afford to cover themselves and their families thanks to your hard work.

December 15 Deadline Approaches for Enrollment in Health Coverage Beginning January 1, 2025 Through NY State of Health

New Cost Savings and Expanded Eligibility in the Essential Plan and Qualified Health Plans Make Insurance More Affordable for More New Yorkers

ALBANY, N.Y. (December 13, 2024) — The State Department of Health’s NY State of Health, the State’s official health plan Marketplace, reminds New Yorkers that December 15 is the last day to enroll in health coverage beginning January 1, 2025. This year brings unprecedented cost savings in the Essential Plan and Qualified Health Plans, which offer dramatically reduced out-of-pocket costs.